I’m still trying to put together a post with some big picture

thoughts on the SD housing market. The market’s confusing in several

ways, and my thoughts are more jumbled than usual.

While I flail away at that, here are some updated valuation charts:

For the uninitiated, these measure the price of San Diego housing as

compared to local incomes and rents. (We could separately chart

prices vs. incomes and prices vs. rents, but tell a very similar

story to each other so I’ve taken to collapsing them into a single

measure).

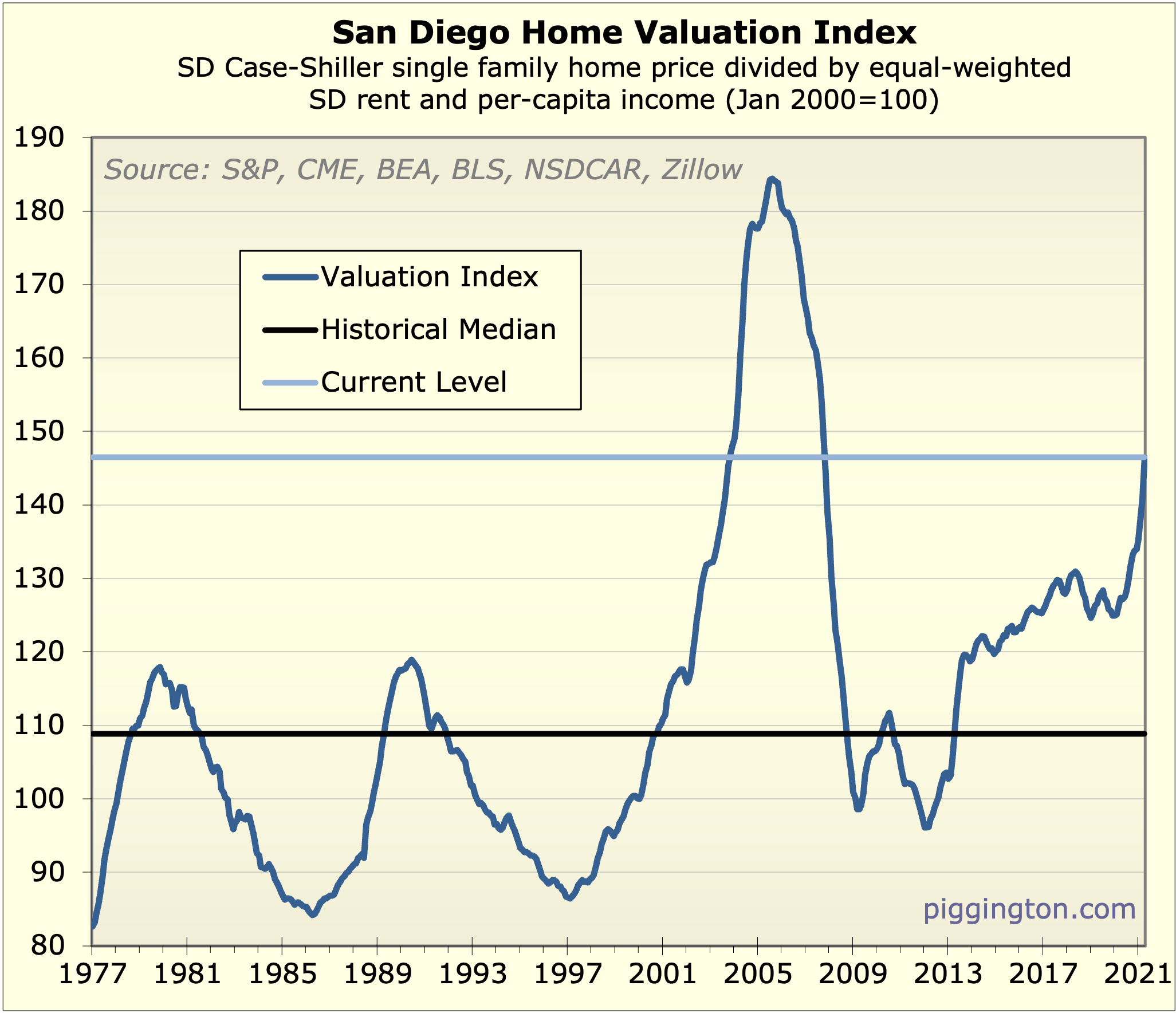

The first graph shows that valuations — prices compared to rents

and local incomes — are very high compared to their history, having

only been higher during the bubble.

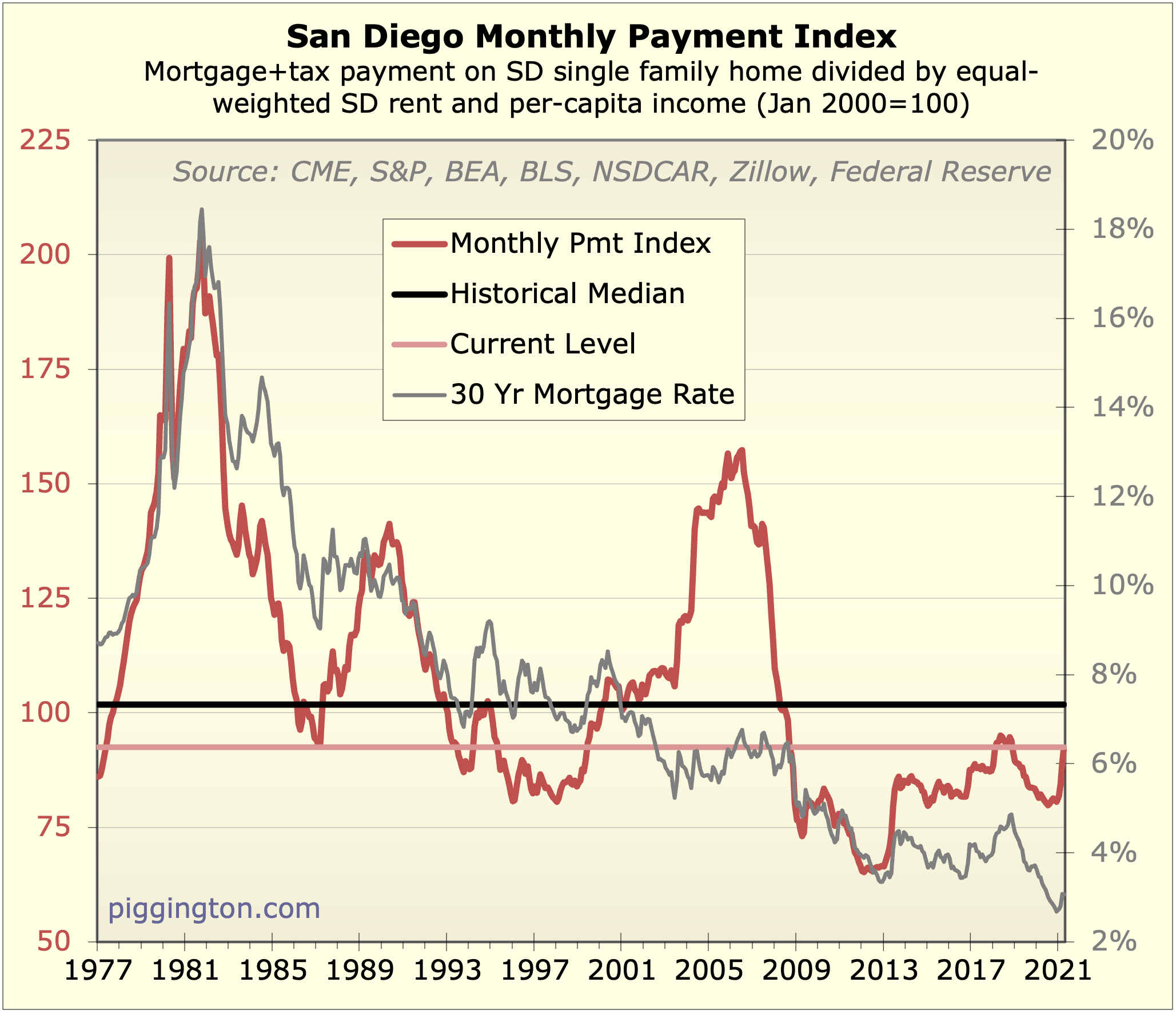

The second graph is one of the confounding factors I mentioned.

Instead of measuring home prices, it measures monthly payments, thus

incorporating mortgage rates into the picture. And this shows that

even though (per the first graph) home prices are quite high,

monthly payments are pretty reasonable compared to their history.

The interest rate situation renders the current situation very different from the mid-2000s bubble. If

someone can lock in financing at these rates, the monthly nut is not

actually that bad, and it may make sense to buy. As opposed to the

prior bubble, when the only reason to buy was the belief that

valuations would keep rising for the rest of time. This is one of

the major reasons I don’t consider this a bubble, despite the very

lofty valuations.

However, to the extent that low rates are what’s allowing prices to

stay so high, that puts home prices at risk should rates increase

significantly.

More to come at some point soon, I hope…

PS – Data note: up til now I’ve used the rent component of San

Diego CPI to determine rents. However, they have been distorted by

eviction moratoriums, resulting in a gap between how much

landlords are actually getting (CPI) vs. what they are asking for

from new renters. I believe the latter is the more appropriate

comparison here. So, I’ve sub’d in rental stats from Zillow, which

appear to more accurately reflect asking rents. For more on this

disparity see this

chart from this

article by inflation analyst Mike Ashton.

{kind=link}

More great info Rich. The

More great info Rich. The first thing that jumped out at me was when you put a line to market bottoms the valuation trend is clearly up over the last 50 years. Would it be reasonable to say the way we assign value to home ownership or the premium placed on home ownership has increased as a whole?

I definitely agree that the

I definitely agree that the trend has been upward. I don’t know about the premium though because how much of it is just rates? The second graph shows that people are paying a lower monthly payment (vs. rents/incomes) than historical… so that would argue against the idea of people assigning a higher value to it. With that said – yes I definitely suspect it’s a combination of increasing scarcity over time and demographic shift, in addition to lower rates.

FWIW I put that median line on there just for perspective, not to imply that the median is the equilibrium/sustainable/”correct” value. I thought about doing a trend line but that opens up some cans of worms. It’s thrown off by the bubble, for one. For another, it implies that the trend will continue forever, which could lead to some dangerously off-base assumptions.

Understood. When I look at

Understood. When I look at graphs like that I try not to over analyze and look for something that should be obvious and is staring me in the face. That slow gentle climb in the trend line was one of those things and made me wonder what it means.

Rich do you have individual

Rich do you have individual charts for median rent and income? It would be interesting to see those plotted individually next to average mortgage payment.

So now we have new problem to

So now we have new problem to deal with none of us have even considered. Stopped by a home for sale and spoke to agent. 30 year old has been living in nice family neighborhood tract home by himself the last 2 years. Gonna make 50% profit.

Asked him where he’s going. He’s staying in town and buying a new custom home down by the beach areas for almost $4M cash. When he saw the confusion on my face he simply smiled and said two words. Crypto Baby!

Crypto is negative sum

Crypto is negative sum gambling because of “mining” costs, programming costs, security costs, and other transaction costs.

The winners are happy to announce they won, losers are much more shy.

It is especially negative to the USA because the winners are frequently scammers in China and the former USSR.

sdrealtor wrote:

Asked him

[quote=sdrealtor]

Asked him where he’s going. He’s staying in town and buying a new custom home down by the beach areas for almost $4M cash. When he saw the confusion on my face he simply smiled and said two words. Crypto Baby![/quote]

So do you suppose he will report that income and pay the 1-2Mil in taxes due? Do Crypto wallet companies send their clients 1099s?

I have no idea. I own none

I have no idea. I own none and never have. I dont understand it and the potential profits are not something I need to reach even my most aggressive goals.

Spoke to my son and he made a good point. Put a little money in each month I dont care about as a hedge. I may start just to learn something. I dont know? Really is outside my alivezone. Crazy though to see even one transaction from this. I really never even thought of it as a potential market force but clearly something that needs to be considered.

sdrealtor wrote:I have no

[quote=sdrealtor]I have no idea. I own none and never have. I dont understand it and the potential profits are not something I need to reach even my most aggressive goals.

Spoke to my son and he made a good point. Put a little money in each month I dont care about as a hedge. I may start just to learn something. I dont know? Really is outside my alivezone. Crazy though to see even one transaction from this. I really never even thought of it as a potential market force but clearly something that needs to be considered.[/quote]

I created a coinbase account earlier this year but haven’t had the balls to purchase any actual crypto outside of some shares of the bitcoin trust ETF. Clearly the rise of crypto makes sense as a response to the reckless gov spending and fed money printing. However, the extreme volatility shows every indication of a speculative bubble. I’ve been into precious metals for years and it is frustrating to see their mediocre performance even during this inflation environment where they should be going up big. But overall, this current speculative environment just reminds me so much of 1999.

Just bought a little. What

Just bought a little. What the heck crypto baby! To balance it out I bought more wine. I dont need either

I’ve been into precious

Long term charts of PM show long periods of stability punctuated by short periods of huge gains.

Silver’s average yearly price was $15.71 in 2018, $16.21 in 2019, and $20.55 in 2020. Now it is about $28. That’s not mediocre to me.

And if you happened to buy ASEs specifically, you saw an additional gain since before 2020 they sold at a spot premium of about $2, and now it is more like $10. In other words they went from about $18 in 2018 to about $38 now, more than doubling.

gzz wrote:

I’ve been into

[quote=gzz]

Long term charts of PM show long periods of stability punctuated by short periods of huge gains.

Silver’s average yearly price was $15.71 in 2018, $16.21 in 2019, and $20.55 in 2020. Now it is about $28. That’s not mediocre to me.

And if you happened to buy ASEs specifically, you saw an additional gain since before 2020 they sold at a spot premium of about $2, and now it is more like $10. In other words they went from about $18 in 2018 to about $38 now, more than doubling.[/quote]

Assuming perfect timing is an awful big if. Assuming awful timing someone who bought prime RE at prior peak and held on still made out like a bandit. You can have your PM. If I’m gonna invest in a commodity it will be wine where I know how to produce significantly higher gains and can drink the profits

I’m skeptical of wine as a

I’m skeptical of wine as a source of “significantly higher gains.” It would seem to require a lot of time, as well as storage space, plus lots of transaction costs.

Now if you like the process of buying, storing, and selling wine, then those aren’t costs and you can do well. But it’s a hobby then, not an investment.

It is well under 1% of my portfolio. For me it is a hybrid hobby and investment. I have a few boring old bars I will dump when there’s another speculative frenzy for silver, which happens every 10-15 years.

Then, probably like with you and wine, I enjoy the process of buying and selling European gold and silver coins, in particular Western Europe from the late 18th to early 20th century.

Last week bought 3 bottles

Last week bought 3 bottles for $X each. Turned around and sold 2 for 1.5X each the next day. Buyer in NJ sent me pre paid FedEx label to overnight to him. That’s about 50% profit in one day with zero transaction costs. Could have sold the third bottle and it will only increase in value but as of now it’s basically free to me and I’d love to drink it someday. I know what to buy, where to buy it, how to sell it and what I’m doing. You can’t do anything close to that with PM. You are right that it’s a hobby but if I wanted to I could easily turn it into a very profitable business

gzz wrote:

I’ve been into

[quote=gzz]

Long term charts of PM show long periods of stability punctuated by short periods of huge gains.

Silver’s average yearly price was $15.71 in 2018, $16.21 in 2019, and $20.55 in 2020. Now it is about $28. That’s not mediocre to me.

And if you happened to buy ASEs specifically, you saw an additional gain since before 2020 they sold at a spot premium of about $2, and now it is more like $10. In other words they went from about $18 in 2018 to about $38 now, more than doubling.[/quote]

If you look at Gold for instance, over the last 10 years or so, yes it has gone up. But it has seriously underperformed stocks, crypto, and RE over that period. And it doesn’t provide any income (unless you own a jewelry store). So yeah it is nice to own but not exciting. I would have expected both Gold and Silver to be way higher today given the runaway inflation that is going on in all other asset classes.

DZ, there has not been any

DZ, there has not been any runaway inflation. Assets prices are high because that’s what happens when interest rates fall. The present value of those future flows go up. Houses and stocks are just like bonds in this way.

The goldbugs have two unsupported conspiracy theories. First, there’s inflation that the BLS and other government entities and economists are covering up.

Second, the banks and government are sinisterly holding down the price of gold and silver.

Both of these are implausible for a ton of reasons.

To start with, the US gov profits from inflation. It makes seigniorage on the new currency; it gets to tax large nominal capital gains; tax brackets go up; the real value of its trillions in fixed rate debt go down.

Second, the US gov is the largest owner of gold in the world, by far.

Third, the US gov actively promotes retail PM ownership by minting beautiful low-premium coins in all sorts of sizes and designs.

gzz wrote:DZ, there has not

[quote=gzz]DZ, there has not been any runaway inflation. Assets prices are high because that’s what happens when interest rates fall. .[/quote]

10y treasury rate has more than doubled in the last year. Meanwhile, asset prices continued to go up during that same period. You are clueless if you don’t see inflation.

The reason is this: https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

The crypto currency gains are

The crypto currency gains are just another example of the obscene amount of wealth created by the Federal Reserve. And as I’ve mentioned before, following Sports Collectibles, every week I read about new record setting auctions. Gretzky rookie card just sold for 3.75 mil breaking all records for hockey cards. Asset prices are going nuts everywhere. Too much money in the system.

So the crypto thing is kinda

So the crypto thing is kinda freaking me out. What I consider kids have been buying it all over the country and world for several years. I know a bunch I drink wine with around the US who do. Cash in a few million dollars and you can live anywhere? The beach communities in SD sure look like a pretty good spot to hang out for the next few decades. Hard to think of many better places for someone like that

sdrealtor wrote:So now we

[quote=sdrealtor]So now we have new problem to deal with none of us have even considered. Stopped by a home for sale and spoke to agent. 30 year old has been living in nice family neighborhood tract home by himself the last 2 years. Gonna make 50% profit.

Asked him where he’s going. He’s staying in town and buying a new custom home down by the beach areas for almost $4M cash. When he saw the confusion on my face he simply smiled and said two words. Crypto Baby![/quote]

Back in the housing bubble, a hater emailed me to tell me what an idiot I was, and ended saying something like, “I’ve made more money on my house than I ever could at my job.”

I thought that parting shot was pretty funny, because it seemed like a pretty good indicator of a housing bubble!

Anyway the Crypto Baby story brought that back to mind. 30 year olds buying beach houses with cash. Very late-stage-speculative-mania stuff.

I’m on team gzz here if that’s not clear. Bubbles by (my) definition must involve 2 things: egregious overvaluation, and euphoric behavior.

– Valuation: crypto is impossible to value. It’s not giving you a stream of cash flows like a stock or bond — it’s just worth whatever the next person is willing to pay. So who can say for sure on the value question. But stories like sdr’s sure do suggest massive overvaluation. And that very inability to value it means that, if it is a bubble, the crash could be absolutely epic.

– Behavior: I’ve literally never seen more bubbly, euphoric, cult-like behavior than in crypto. The behavior category alone is enough for me to believe that this is likely a giant speculative mania.

I think there are major bubbles going on in crypto and in parts of the stock market. I don’t think housing is a bubble, but I DO think a lot of bubble money is flowing into housing. If I am right, those inflows will go into reverse at some point.

I don’t get crypto. I don’t

I don’t get crypto. I don’t have to. I don’t need it or anything like the gains people are chasing to meet my goals. I don’t think it’s a major force in the housing market but truthfully don’t know. However there is some of it going on and it’s one more small log on a very big raging fire. What struck me most is there are always things going on we aren’t aware of, don’t anticipate or factor in. This is simply one more.

With that said, I always know I could be wrong. I constantly ask myself as part of my decision making , what if I’m dead wrong? For that reason alone I’ll buy a little with money I can afford to never see again and if it goes up I’m pull out my original investment when it makes sense to me and let the rest ride. Many of the smartest business and wall street minds are doing the same

Rich Toscano wrote:

I think

[quote=Rich Toscano]

I think there are major bubbles going on in crypto and in parts of the stock market. I don’t think housing is a bubble, but I DO think a lot of bubble money is flowing into housing. If I am right, those inflows will go into reverse at some point.[/quote]

Exactly, even if you deny there is a housing bubble, you can’t deny that bubble money is contributing greatly to the housing prices.

But I still have a hard time believing housing is not a bubble. There is clearly significant amount of investment money going into the market. SDR is talking about tract homes in NCC approaching 2mil. Nobody with a rational mind would pay that much for a tract home. That kind of irrationality is indicative of a speculative bubble.

deadzone wrote:Rich Toscano

[quote=deadzone][quote=Rich Toscano]

I think there are major bubbles going on in crypto and in parts of the stock market. I don’t think housing is a bubble, but I DO think a lot of bubble money is flowing into housing. If I am right, those inflows will go into reverse at some point.[/quote]

Exactly, even if you deny there is a housing bubble, you can’t deny that bubble money is contributing greatly to the housing prices.

But I still have a hard time believing housing is not a bubble. There is clearly significant amount of investment money going into the market. SDR is talking about tract homes in NCC approaching 2mil. Nobody with a rational mind would pay that much for a tract home. That kind of irrationality is indicative of a speculative bubble.[/quote]

By the same measure no one with a rational mind would pay more than a few bucks for fermented grape juice yet tons of people far smarter and successful than us do so everyday. You are focused on the house when the vast majority of what they are buying is the land.You’re trapped in your own way of thinking. Crypto baby!

sdrealtor wrote:deadzone

[quote=sdrealtor][quote=deadzone][quote=Rich Toscano]

I think there are major bubbles going on in crypto and in parts of the stock market. I don’t think housing is a bubble, but I DO think a lot of bubble money is flowing into housing. If I am right, those inflows will go into reverse at some point.[/quote]

Exactly, even if you deny there is a housing bubble, you can’t deny that bubble money is contributing greatly to the housing prices.

But I still have a hard time believing housing is not a bubble. There is clearly significant amount of investment money going into the market. SDR is talking about tract homes in NCC approaching 2mil. Nobody with a rational mind would pay that much for a tract home. That kind of irrationality is indicative of a speculative bubble.[/quote]

By the same measure no one with a rational mind would pay more than a few bucks for fermented grape juice yet tons of people far smarter and successful than us do so everyday. You are focused on the house when the vast majority of what they are buying is the land.You’re trapped in your own way of thinking. Crypto baby![/quote]

I’m sure fine wine sales are nuts right now too, just like crypto, baseball cards, comic books and everything else. Given there is so little activity in home sales now, if I were you I would pursue that business for a while, take advantage of the current craziness.

deadzone wrote:sdrealtor

[quote=deadzone][quote=sdrealtor][quote=deadzone][quote=Rich Toscano]

I think there are major bubbles going on in crypto and in parts of the stock market. I don’t think housing is a bubble, but I DO think a lot of bubble money is flowing into housing. If I am right, those inflows will go into reverse at some point.[/quote]

Exactly, even if you deny there is a housing bubble, you can’t deny that bubble money is contributing greatly to the housing prices.

But I still have a hard time believing housing is not a bubble. There is clearly significant amount of investment money going into the market. SDR is talking about tract homes in NCC approaching 2mil. Nobody with a rational mind would pay that much for a tract home. That kind of irrationality is indicative of a speculative bubble.[/quote]

By the same measure no one with a rational mind would pay more than a few bucks for fermented grape juice yet tons of people far smarter and successful than us do so everyday. You are focused on the house when the vast majority of what they are buying is the land.You’re trapped in your own way of thinking. Crypto baby![/quote]

I’m sure fine wine sales are nuts right now too, just like crypto, baseball cards, comic books and everything else. Given there is so little activity in home sales now, if I were you I would pursue that business for a while, take advantage of the current craziness.[/quote]

why choose? I do a little of pretty much all of those things. So many ways to make money. Always is

Rich Toscano wrote:

–

[quote=Rich Toscano]

– Behavior: I’ve literally never seen more bubbly, euphoric, cult-like behavior than in crypto.

[/quote]

Then apparently you were not around during the late 90s .com bubble. It was nuts. Everyone I knew was throwing money at tech stocks, it was a can’t lose proposition. You were a fool for not getting in on it. All of the 20somethings were getting rich. Now they invented an acronym for it called “FOMO”.

deadzone wrote:Rich Toscano

[quote=deadzone][quote=Rich Toscano]

– Behavior: I’ve literally never seen more bubbly, euphoric, cult-like behavior than in crypto.

[/quote]

Then apparently you were not around during the late 90s .com bubble. It was nuts. Everyone I knew was throwing money at tech stocks, it was a can’t lose proposition. You were a fool for not getting in on it. All of the 20somethings were getting rich. Now they invented an acronym for it called “FOMO”.[/quote]

I was around (though not plugged into the financial world back then). The 90s was certainly bigger in terms of participation, you are right on that. But among those participating, the behavior seems even more egregious in crypto.

There could be some recency bias involved on my part, but I don’t think that would change my conclusion.

Rich Toscano wrote:deadzone

[quote=Rich Toscano][quote=deadzone][quote=Rich Toscano]

– Behavior: I’ve literally never seen more bubbly, euphoric, cult-like behavior than in crypto.

[/quote]

Then apparently you were not around during the late 90s .com bubble. It was nuts. Everyone I knew was throwing money at tech stocks, it was a can’t lose proposition. You were a fool for not getting in on it. All of the 20somethings were getting rich. Now they invented an acronym for it called “FOMO”.[/quote]

I was around (though not plugged into the financial world back then). The 90s was certainly bigger in terms of participation, you are right on that. But among those participating, the behavior seems even more egregious in crypto.

There could be some recency bias involved on my part, but I don’t think that would change my conclusion.[/quote]

The main thing I remember from the 90s was the general feeling that these stocks only go up and you can’t lose. Housing in the 2000s was very similar. So from mental point of view I see today’s scenario as nearly identical. But one big difference today is all the money the government is handing out to the public which they are turning around and trading (gambling) with their Robinhood accounts. Back in the 90s, the folks buying up Tech stock actually had to use their real savings to do it.

deadzone wrote:Rich Toscano

[quote=deadzone][quote=Rich Toscano][quote=deadzone][quote=Rich Toscano]

– Behavior: I’ve literally never seen more bubbly, euphoric, cult-like behavior than in crypto.

[/quote]

Then apparently you were not around during the late 90s .com bubble. It was nuts. Everyone I knew was throwing money at tech stocks, it was a can’t lose proposition. You were a fool for not getting in on it. All of the 20somethings were getting rich. Now they invented an acronym for it called “FOMO”.[/quote]

I was around (though not plugged into the financial world back then). The 90s was certainly bigger in terms of participation, you are right on that. But among those participating, the behavior seems even more egregious in crypto.

There could be some recency bias involved on my part, but I don’t think that would change my conclusion.[/quote]

The main thing I remember from the 90s was the general feeling that these stocks only go up and you can’t lose. Housing in the 2000s was very similar. So from mental point of view I see today’s scenario as nearly identical. But one big difference today is all the money the government is handing out to the public which they are turning around and trading (gambling) with their Robinhood accounts. Back in the 90s, the folks buying up Tech stock actually had to use their real savings to do it.[/quote]

Housing is nothing like stocks. It has real utility and it can’t go to zero. It’s kinda silly IMO to discuss them as similar

Agreed, but as usual you

Agreed, but as usual you didn’t understand my comment. I mentioned 2000s housing market because the public was under the belief at the time that real estate prices would never go down. If people believe prices can only go up, then they will be willing to overpay for assets, whether RE or stocks or anything else.

We are once again at that point. But this time there is even more confidence that RE and stocks can’t go down because everyone knows the Fed is supporting this and are under the belief that the Fed will not stop their support.

I understood your comments

I understood your comments and as usual disagree. Most people seem well aware real estate could go down around here. Surely people cashing out do. They know there is short term risk it could go down and likely will at some point but dont care. That is unless there is a total collpase which no one including you beleives is coming. They value and want a nice place to live. They are ready, able and willing to pay for that.

sdrealtor wrote:I understood

[quote=sdrealtor]I understood your comments and as usual disagree. Most people seem well aware real estate could go down around here. Surely people cashing out do. They know there is short term risk it could go down and likely will at some point but dont care. That is unless there is a total collpase which no one including you beleives is coming. They value and want a nice place to live. They are ready, able and willing to pay for that.[/quote]

Current RE prices are completely dependent on near zero interest rates and Fed money printing. So clearly if the Fed turns off the spigot there very well could be a collapse. The point is RE is just like any other investment, all about confidence. At this point everyone is confident the Fed will never stop supporting. Just like in 2000s everyone was certain RE would never go down because that’s what the NAR kept reminding everyone.

The Fed isnt turning off the

The Fed isnt turning off the spigot, we will be in a relatively low rate emnvironment for a long time to come. You view RE as only an investment which may be your issue. You are missing the point that most view RE as a place to live and buying it as an opportunity to lock in a long term home at a fixed cost. Plenty of people beleived RE would go down in the 2000’s and not only this blog. Plenty beleive that now. They dont care. I beleive it will likely go down in next several years. I dont care either

deadzone wrote:Current RE

[quote=deadzone]Current RE prices are completely dependent on near zero interest rates and Fed money printing. So clearly if the Fed turns off the spigot there very well could be a collapse. The point is RE is just like any other investment, all about confidence. At this point everyone is confident the Fed will never stop supporting. Just like in 2000s everyone was certain RE would never go down because that’s what the NAR kept reminding everyone.[/quote]

Is it that clear? What happened when the Fed raised rates from 5% to 20% in the late 70s? Did RE collapse?

an wrote:deadzone

[quote=an][quote=deadzone]Current RE prices are completely dependent on near zero interest rates and Fed money printing. So clearly if the Fed turns off the spigot there very well could be a collapse. The point is RE is just like any other investment, all about confidence. At this point everyone is confident the Fed will never stop supporting. Just like in 2000s everyone was certain RE would never go down because that’s what the NAR kept reminding everyone.[/quote]

Is it that clear? What happened when the Fed raised rates from 5% to 20% in the late 70s? Did RE collapse?[/quote]

Different time, different circumstance. But yes I agree historically interest rates vs. home prices wasn’t always a direct relationship.

But the problem is now our entire economy is based on the Fed induced wealth effect. This concept of Fed monetizing debt didn’t exist in the 70s. It basically started in 2009 and really went bonkers in the last year. So there is absolutely no historical precedent to the situation we are in right now. It is pretty obvious that if they turn off the spigot now, the whole titanic is going down.

So, it’s different this time,

So, it’s different this time, but it’s clear you know exactly what would happen? Right…

an wrote:So, it’s different

[quote=an]So, it’s different this time, but it’s clear you know exactly what would happen? Right…[/quote]

Yes it is different this time. The Fed monetization, that is creating the current inflation/bubble, has never happened before in the US. What happens at this point is unpredictable since there is no historical precedent.

deadzone wrote:an wrote:So,

[quote=deadzone][quote=an]So, it’s different this time, but it’s clear you know exactly what would happen? Right…[/quote]

Yes it is different this time. The Fed monetization, that is creating the current inflation/bubble, has never happened before in the US. What happens at this point is unpredictable since there is no historical precedent.[/quote]

History repeating itself

deadzone wrote:Yes it is

[quote=deadzone]Yes it is different this time. The Fed monetization, that is creating the current inflation/bubble, has never happened before in the US. What happens at this point is unpredictable since there is no historical precedent.[/quote]

[quote=deadzone]So clearly if the Fed turns off the spigot there very well could be a collapse. [/quote]

So if it’s unprecedented, then how can it be clear that [quote=deadzone]if the Fed turns off the spigot there very well could be a collapse.[/quote]

I’m confused.

an wrote:deadzone wrote:Yes

[quote=an][quote=deadzone]Yes it is different this time. The Fed monetization, that is creating the current inflation/bubble, has never happened before in the US. What happens at this point is unpredictable since there is no historical precedent.[/quote]

[quote=deadzone]So clearly if the Fed turns off the spigot there very well could be a collapse. [/quote]

So if it’s unprecedented, then how can it be clear that [quote=deadzone]if the Fed turns off the spigot there very well could be a collapse.[/quote]

I’m confused.[/quote]

Which part of the Fed buying trillions of dollars of debt, something that has never occurred before in history, don’t you understand? What do you think would happen to asset prices if they stopped doing this?

deadzone wrote:an

[quote=deadzone][quote=an][quote=deadzone]Yes it is different this time. The Fed monetization, that is creating the current inflation/bubble, has never happened before in the US. What happens at this point is unpredictable since there is no historical precedent.[/quote]

[quote=deadzone]So clearly if the Fed turns off the spigot there very well could be a collapse. [/quote]

So if it’s unprecedented, then how can it be clear that [quote=deadzone]if the Fed turns off the spigot there very well could be a collapse.[/quote]

I’m confused.[/quote]

Which part of the Fed buying trillions of dollars of debt, something that has never occurred before in history, don’t you understand? What do you think would happen to asset prices if they stopped doing this?[/quote]I don’t know what would happen. If I did, I’d be filthy rich. I’m happy that it’s clear for you.

What confuses me is not the unprecedented thing but your statement that you clearly know what would happen with the aftermath from something that never happened before.

Since the entire economy is

Since the entire economy is based on Fed support, it stands to reason if Fed pulled back, things would collapse. For that reason there is a belief the Fed won’t/can’t ever stop their current policies. The big question is how long can they keep it up? That’s the part that is unpredictable. Can it go on indefinitely? They even invented a new term to justify this, called modern monetary theory.

Fed will throw common people

Fed will throw common people under the bus, Fed will do NOTHING to contain inflation, as doing so would mean price of assets ought to decline. Such a decline in asset prices would collapse the ponzi pyramid.

Very glad to read your take

Very glad to read your take on this, Rich, as it confirms my thoughts about the crypto craze. Things like this are always tempting, so I can see the allure, and it is interesting.

As others, our Plan A has been working well for a few generations, so no need to change course at this point. Keeping it all in perspective, regardless of the level of wealth we build, from whatever sources, we can’t take any of this with us, but it does make life more comfortable and enjoyable for us and for our loved ones for the short time we are here.

Relative valuation is still

Relative valuation is still low because very low market interest rates imply the value of safe assets with rising yields (even slowly rising) are very high.

I try to think of reasons why SD real estate won’t keep rising quickly to match its true value, and it is pretty hard.

Over time wealthy societies spend large shares of income on health care first and luxury/positional goods second. And a nice home in San Diego is very positional!

Rich, out of curiosity, are

Rich, out of curiosity, are property taxes factored into your monthly payment index? Mortgage + interest maybe low, but property taxes are based on the home price.

Going with sdr’s example, 4M would be 42K in property taxes, almost 4k a month. With PMI@3% at 13,491/mo. Taxes would makes up a substantial part of the monthly.

He paid cash. Most high

He paid cash. Most high dollar sales are all or mostly cash. They are also a very small segment of the market and have little to no impact on the stats

pinkflamingo wrote:Rich, out

[quote=pinkflamingo]Rich, out of curiosity, are property taxes factored into your monthly payment index? Mortgage + interest maybe low, but property taxes are based on the home price.

Going with sdr’s example, 4M would be 42K in property taxes, almost 4k a month. With PMI@3% at 13,491/mo. Taxes would makes up a substantial part of the monthly.[/quote]

Yes, they are.

DZ and SDR are finally in

DZ and SDR are finally in agreement, on crypto.

They are both wrong. Cyptocurrency is wealth destroying, not generating.

The intention of bitcoin’s inventors was to be something useful for transactions. However, bitcoin is not actually used to buy and sell things.

It isn’t “used” at all in any productive way, except for the limited purpose of buying drugs, cybercrime like ransomware, and evading government regulations on money transfers.

You’re not investing, you are gambling in way that has a much larger rake than casinos. People think crypto is the way to wealth because the people who made money in it never shut up about it, but the larger group of people who lose money are embarrassed and don’t go around telling you.

gzz wrote:DZ and SDR are

[quote=gzz]DZ and SDR are finally in agreement, on crypto.

They are both wrong. Cyptocurrency is wealth destroying, not generating.

The intention of bitcoin’s inventors was to be something useful for transactions. However, bitcoin is not actually used to buy and sell things.

It isn’t “used” at all in any productive way, except for the limited purpose of buying drugs, cybercrime like ransomware, and evading government regulations on money transfers.

You’re not investing, you are gambling in way that has a much larger rake than casinos. People think crypto is the way to wealth because the people who made money in it never shut up about it, but the larger group of people who lose money are embarrassed and don’t go around telling you.[/quote]

Well someone converted it into enough cash to buy a beautiful home so there’s that. I’ll never be a big investor in it but I can have some fun with my mad money and learn something along the way. Crypto Baby!

gzz wrote:DZ and SDR are

[quote=gzz]DZ and SDR are finally in agreement, on crypto.

They are both wrong. Cyptocurrency is wealth destroying, not generating.

The intention of bitcoin’s inventors was to be something useful for transactions. However, bitcoin is not actually used to buy and sell things.

It isn’t “used” at all in any productive way, except for the limited purpose of buying drugs, cybercrime like ransomware, and evading government regulations on money transfers.

You’re not investing, you are gambling in way that has a much larger rake than casinos. People think crypto is the way to wealth because the people who made money in it never shut up about it, but the larger group of people who lose money are embarrassed and don’t go around telling you.[/quote]

I can’t debate Bitcoin’s realistic usability as a currency, but up until now it is definitely wealth producing, not destroying, for anyone who purchased it prior to 2021 they are up huge. But yes you are correct, it appears to be a speculative play (aka gambling) which is no different than buying .com stocks in the late 90s or Tesla and others today. So in the long run, these things usually run their course and many will lose their shirts.

But realistically, as long as the Fed keeps printing, I don’t expect cryptos to crash. All of the Fed money needs to go somewhere, whether real estate, stocks or baseball cards. Crypto is trendy and easy to buy. No reason to think it will crash as long as the Fed spigot stays on full blast.

for anyone who purchased it

They think they are “up huge.” If more than 1 in 1000 of them tried to sell their “up huge” beanie babies, they would find they are not “up huge” but a pyramid scheme.

Of course you can’t. Nobody can. There is no justification for buying it other than thinking someone else will buy it later on for even more. The old justification turned out to fail. But now there is not even a pretense to being useful.

People know full well they are facilitating criminal activity and poisoning the air when they buy crypto, but they don’t care because of speculative fever and greed. 99.99% of articles are either about its price going up and down or the crime and environmental destruction it causes.

Nothing at all is positive. It is gambling, but far worse.

gzz wrote:

for anyone who

[quote=gzz]

They think they are “up huge.” If more than 1 in 1000 of them tried to sell their “up huge” beanie babies, they would find they are not “up huge” but a pyramid scheme.

Of course you can’t. Nobody can. There is no justification for buying it other than thinking someone else will buy it later on for even more. The old justification turned out to fail. But now there is not even a pretense to being useful.

People know full well they are facilitating criminal activity and poisoning the air when they buy crypto, but they don’t care because of speculative fever and greed. 99.99% of articles are either about its price going up and down or the crime and environmental destruction it causes.

Nothing at all is positive. It is gambling, but far worse.[/quote]

No different than the “gambling” that goes on in the stock market.

deadzone and gzz can you guys

deadzone and gzz can you guys please stop talking so negatively about crypto.

i hate crypto and dont understand it. but it really pisses me off that really stupid people made decent gains in this and it seems like whenever the stars align and the two of you jointly trash a speculation, it goes to the moon. So please stop sending these ridiculous things to the moon by continuing to jointly trash crypto. in fact if yo hate crypto, then apply murphys law and go buy crypto just so it goes down…while you are at it, can you also buy shares of AMC and GME so you can send those stocks downward too??? those two are also pissing me off. especially after yesterday and this morning where amc is at $34/share for this pos…. im getting really frustrated by these MEME stock pickers and want someone to put a stop to this by adding a lot of negative energy to the buyers group…

Coronita wrote:deadzone and

[quote=Coronita]deadzone and gzz can you guys please stop talking so negatively about crypto.

i hate crypto and dont understand it. but it really pisses me off that really stupid people made decent gains in this and it seems like whenever the stars align and the two of you jointly trash a speculation, it goes to the moon. So please stop sending these ridiculous things to the moon by continuing to jointly trash crypto. in fact if yo hate crypto, then apply murphys law and go buy crypto just so it goes down…while you are at it, can you also buy shares of AMC and GME so you can send those stocks downward too??? those two are also pissing me off. especially after yesterday and this morning where amc is at $34/share for this pos…. im getting really frustrated by these MEME stock pickers and want someone to put a stop to this by adding a lot of negative energy to the buyers group…[/quote]

I just cashed out of my AMC a couple weeks ago at $13, I had about 40% gain so didn’t want to be too greedy. Should’ve held in hindsight. I’m losing money on the bitcoin trust so far.

The home price upsurge is

The home price upsurge is pretty much nationwide, and due largely to today’s artificially low interest rates. Our ultra-low interest rates are propelling the housing market, and this cannot last, since overall price inflation will rise (are rising), and will ultimately force interest rates up, as happened in the late 1970s and early 80’s when Fed Chairman Arthur Burns was replaced by tough-guy Volcker.

Conclusion: buy rental property to the max now and lock in these interest rates. You’ll be sitting pretty when mortgage rates double.

“artificially low interest

“artificially low interest rates”

So the market clearing price of loanable funds is “artificial”?

If so please state the current “natural” interest rate, and show your work. Or surely one of the bazillion RonPaul inflation-permadoomers out there have done so, and can provide a link.

“our ultra-low interest rates”

Ultra low compared to what? They are in line with our closest peers (UK, Australia, Canada), and very high compared to Japan and the rest of Europe.

My view is that interest rates in the USA are artificially high, propped up by a Fed that is run by and captured by a rentier class that wants to hold down wage growth and can’t accept the true risk-free market rate of interest given demographic trends is negative.

Good advice but for the wrong reason. A rental that pays $2500 a month at a cap rate of 1% should be worth about $3 million. The fact you can get them now in SD for $700,000 is what’s artificial.

Artificial in the sense that

Artificial in the sense that if the fed stopped buying treasuries, the rate would be much higher.

Other central banks manipulating interest rates does not make our rates real.

Ultra low interest rates in absolute terms say in the last 200 years.

https://advisor.visualcapitalist.com/us-interest-rates/

pinkflamingo wrote:Artificial

[quote=pinkflamingo]Artificial in the sense that if the fed stopped buying treasuries, the rate would be much higher.

Other central banks manipulating interest rates does not make our rates real.

Ultra low interest rates in absolute terms say in the last 200 years.

https://advisor.visualcapitalist.com/us-interest-rates/%5B/quote%5D

What’s the probability of the fed stop buying treasuries?

If everyone is doing it today, then why would it be artificial? Just because they didn’t do it in the past? What make you think they won’t keep doing it in the future?

You say the rate is ultra low interest rates in absolute terms say in the last 200 years. But what make you think they won’t keep on going lower the next 200 years?

–

–

Higher rates in the US from

Higher rates in the US from 1800-1960 reflected the US had a rapidly growing population and strong technological growth, which in turn caused a large number of highly profitable economic opportunities, which then drove a very strong demand for loanable funds.

Now we have much slower tech growth and no growth in working age population.

The USA of 1900 was comparable to China in 2000.

The USA today is about where Japan was 15 years ago in terms of aging population and very low demand for funds by creditworthy borrowers.