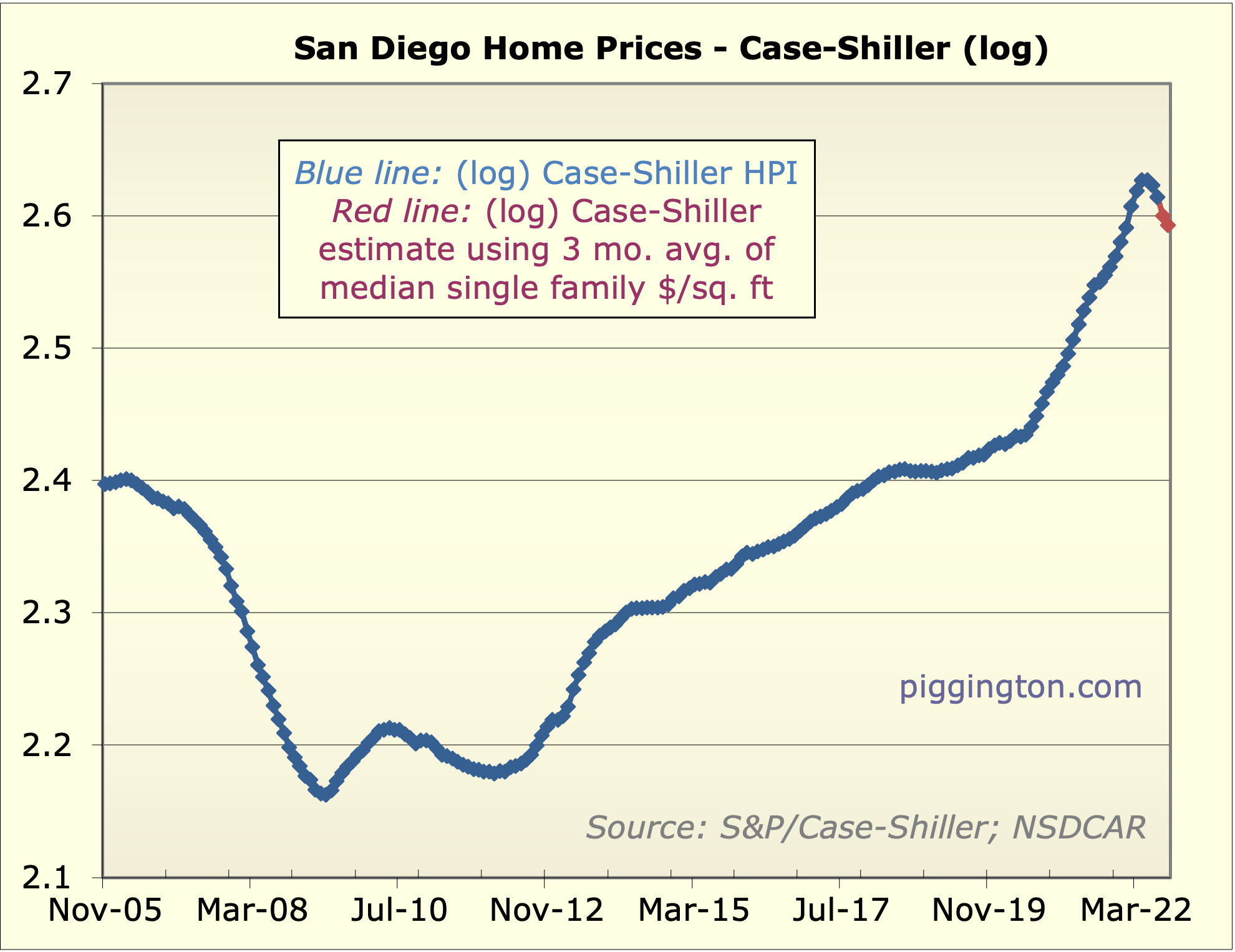

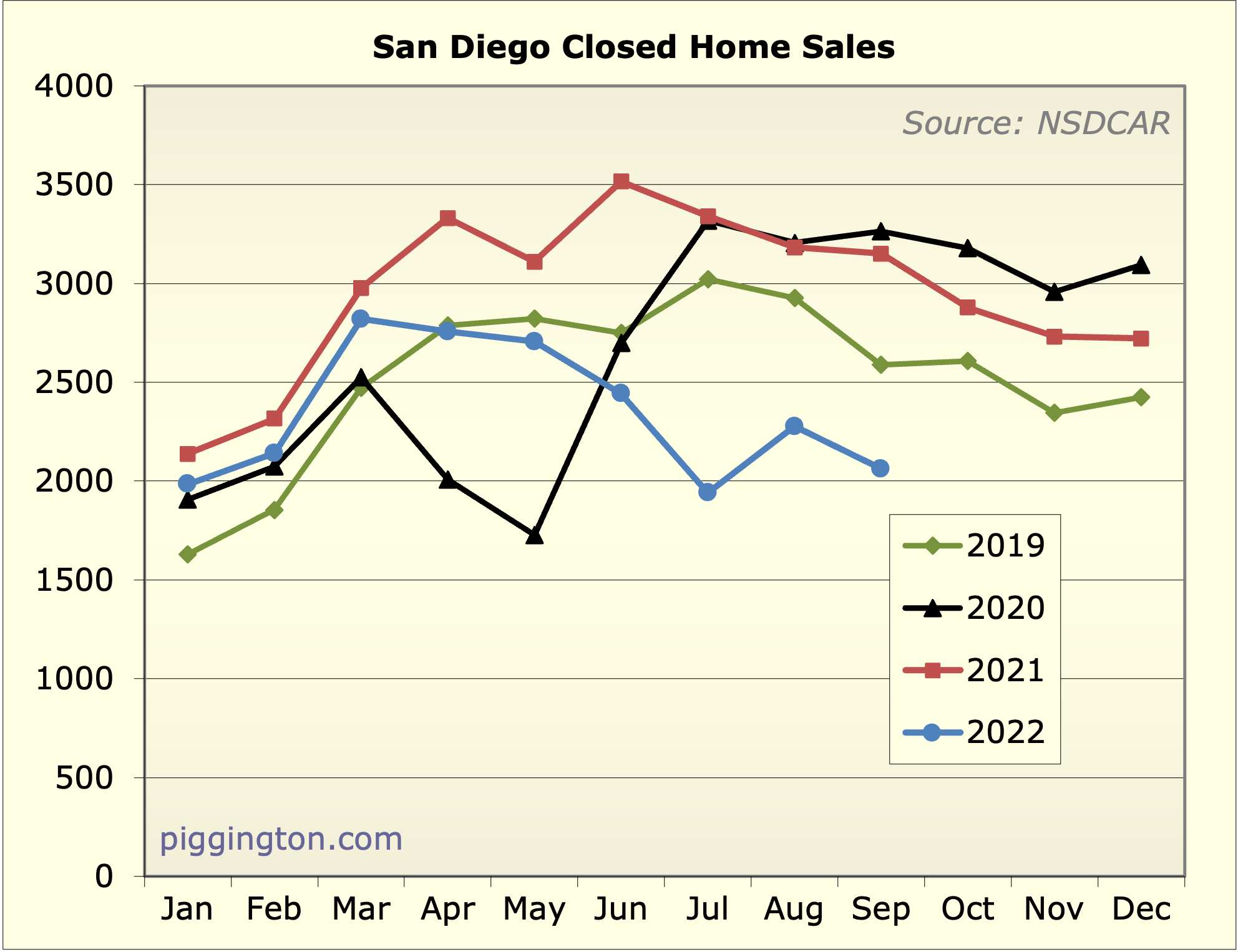

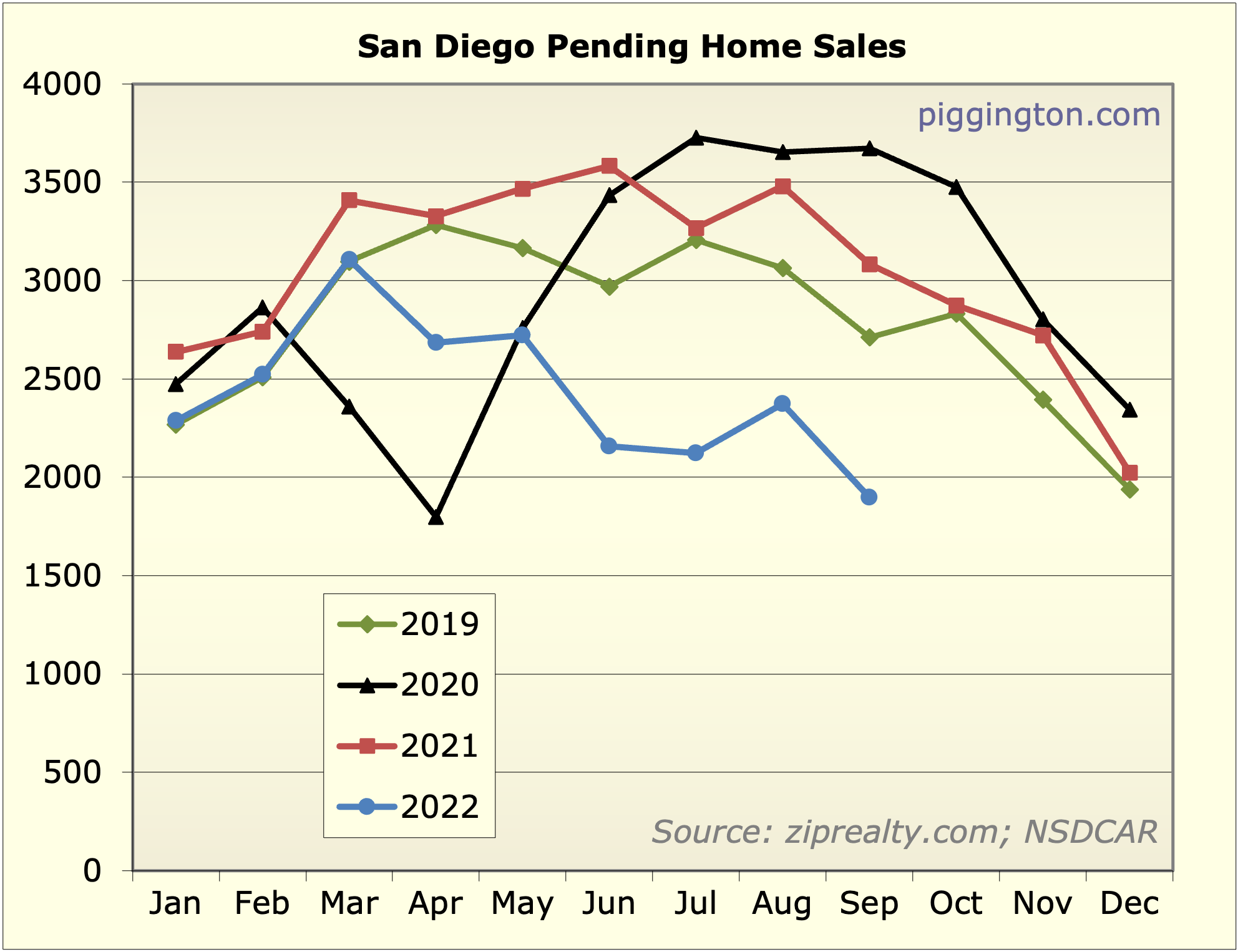

I don’t have much to add to the title, so I will leave it at that.

Oh actually one thing I want to note: the 30-year mortgage (per FRED) averaged 6.1% in September, so that’s what’s reflected in the monthly payment related charts. As of last week, the mortgage rate was up to 6.9%. So that’s going to put further upward pressure on monthly payments, unless rates drop pretty hard at this point.

OK, carry on. Charts below.

Please make sure you post

Please make sure you post something in all CAPS when PRICES HIT BOTTOM and I should buy a rental property. I’m not unreasonable. I’m not looking for you to call the exact day when prices are at a minimum. A one week time period will be sufficient. Meantime, I’ll keep reading your articles with great interest. Seriously, I should have bought when you did!

bibsoconner wrote:Please make

[quote=bibsoconner]Please make sure you post something in all CAPS when PRICES HIT BOTTOM and I should buy a rental property. I’m not unreasonable. I’m not looking for you to call the exact day when prices are at a minimum. A one week time period will be sufficient. Meantime, I’ll keep reading your articles with great interest. Seriously, I should have bought when you did![/quote]

That one was a lucky shot, I’m afraid… I do however remind my wife of it on a regular basis. 🙂

Have been patiently waiting

Have been patiently waiting for this update. It’s like turning a ship…will be very interesting to see how things look in 6-12 months. Thanks for the update, Rich!

evolusd wrote:Have been

[quote=evolusd]Have been patiently waiting for this update. It’s like turning a ship…will be very interesting to see how things look in 6-12 months. Thanks for the update, Rich![/quote]

Nah the ship turned fast its just the data and reporting that take time to turn

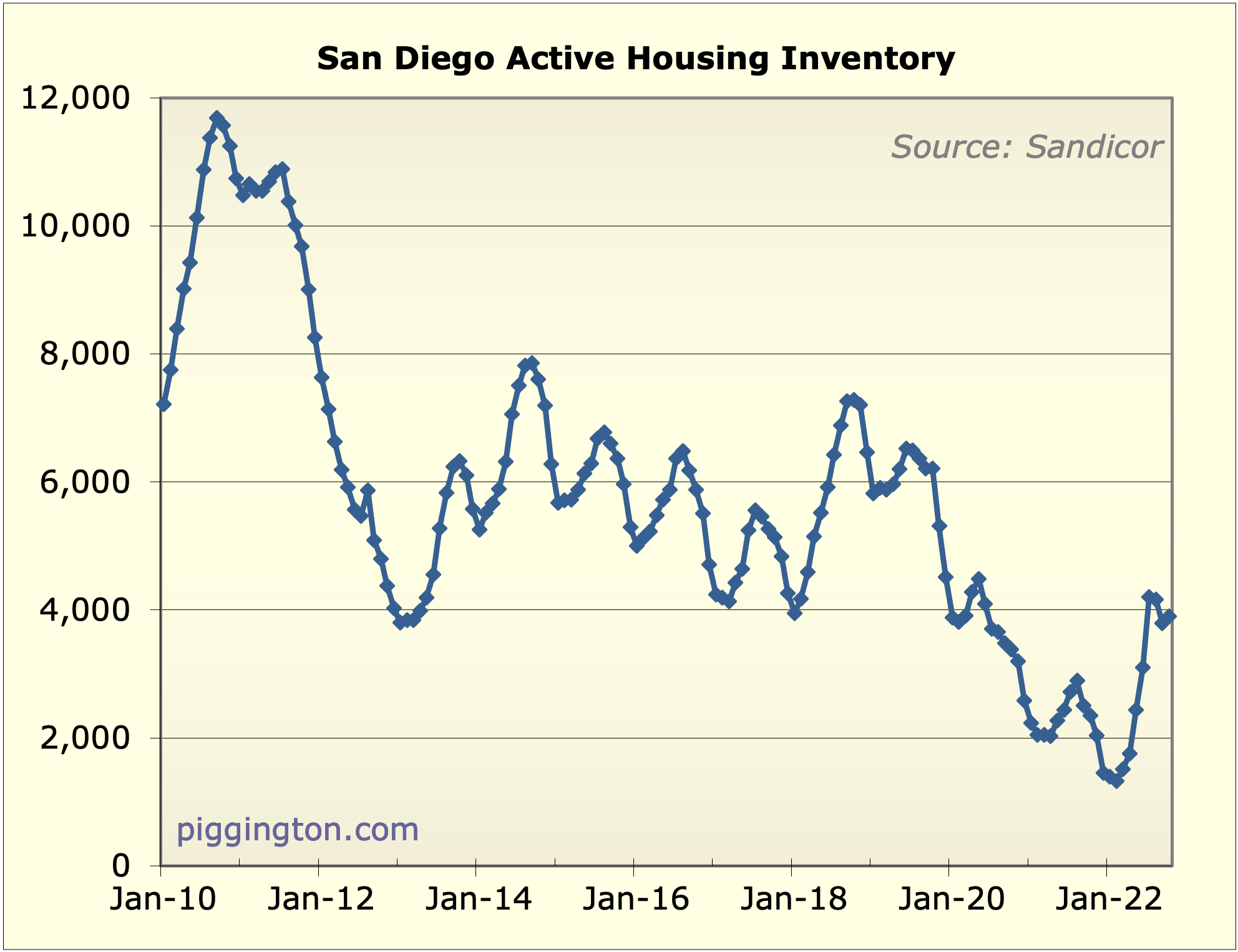

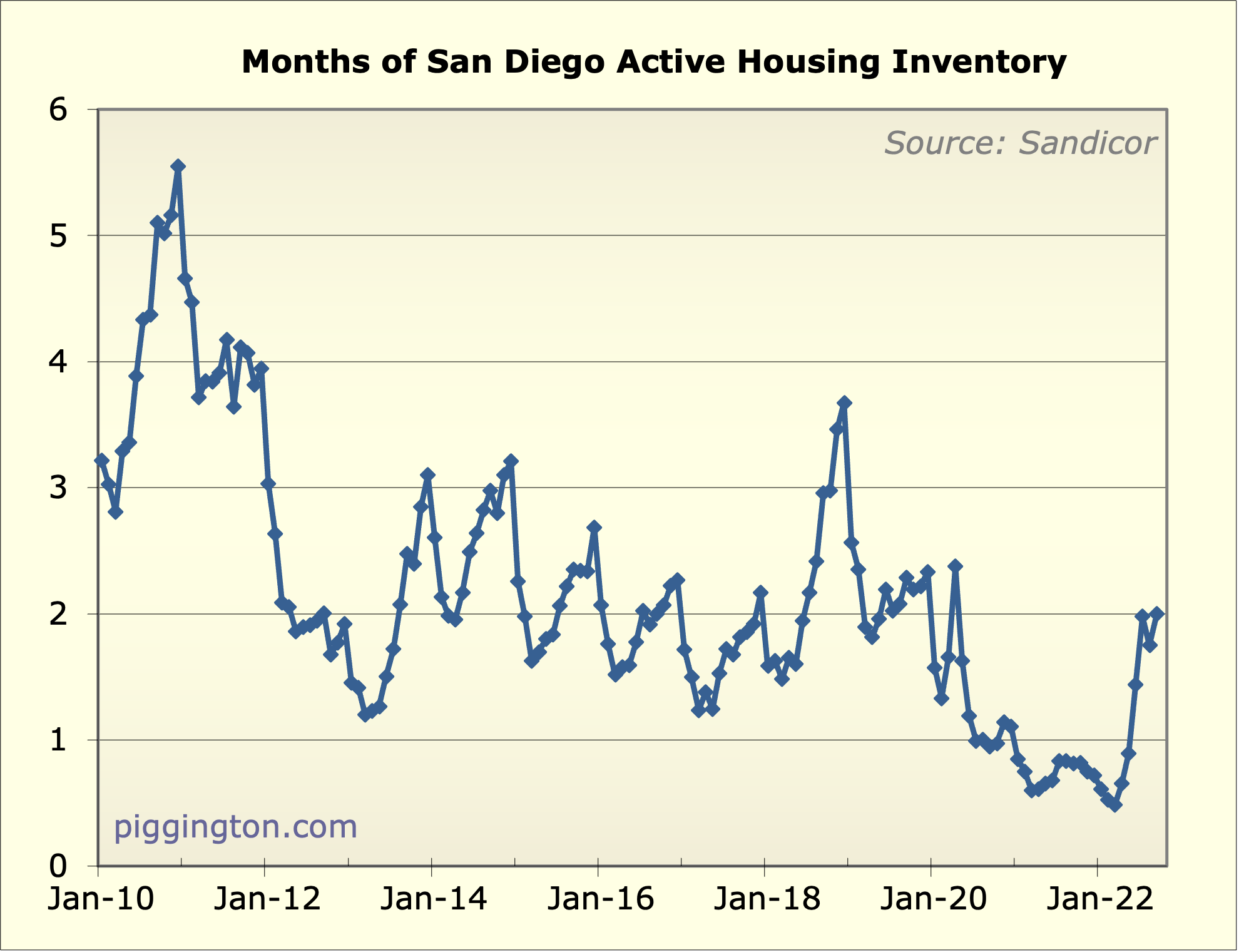

The most interesting chart

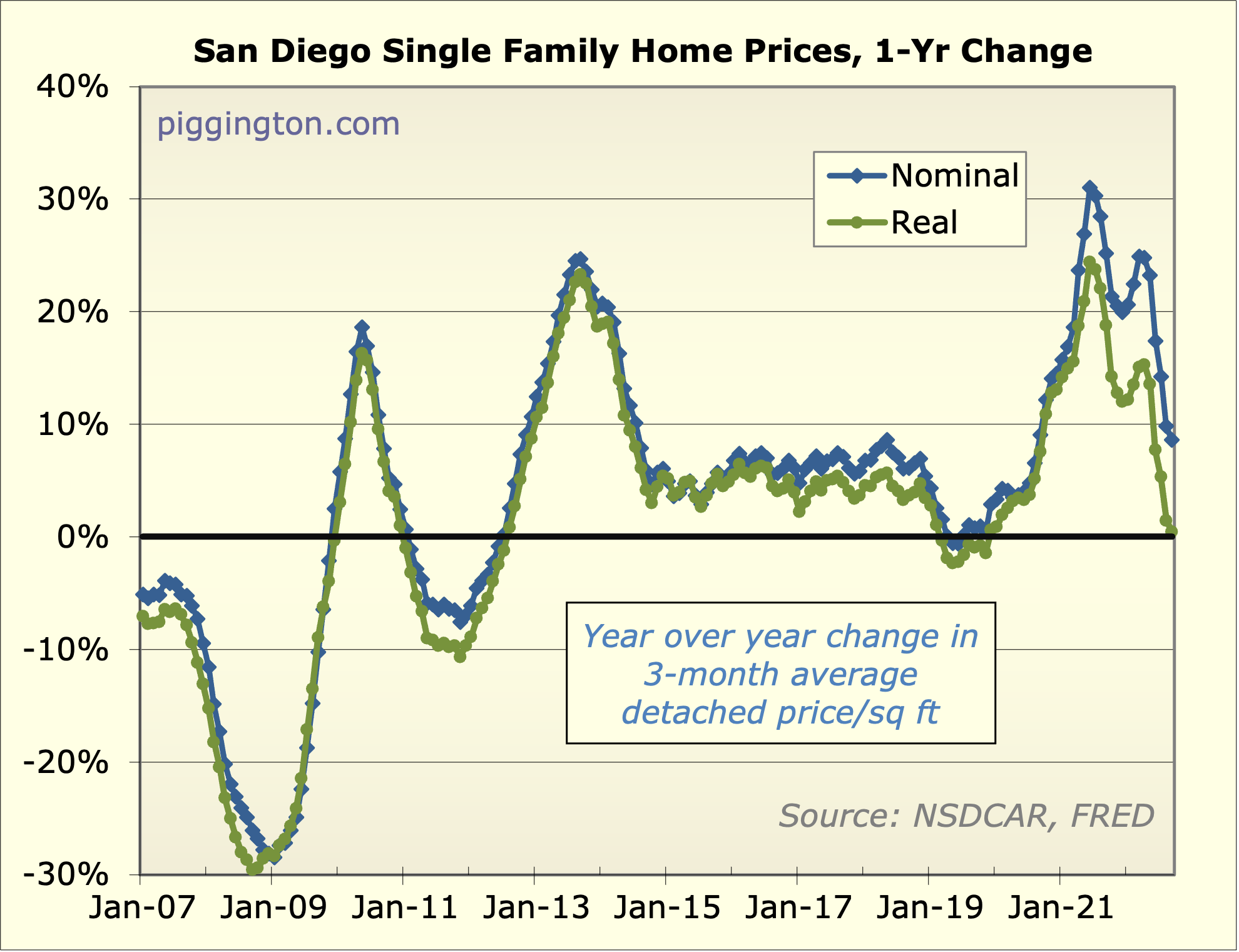

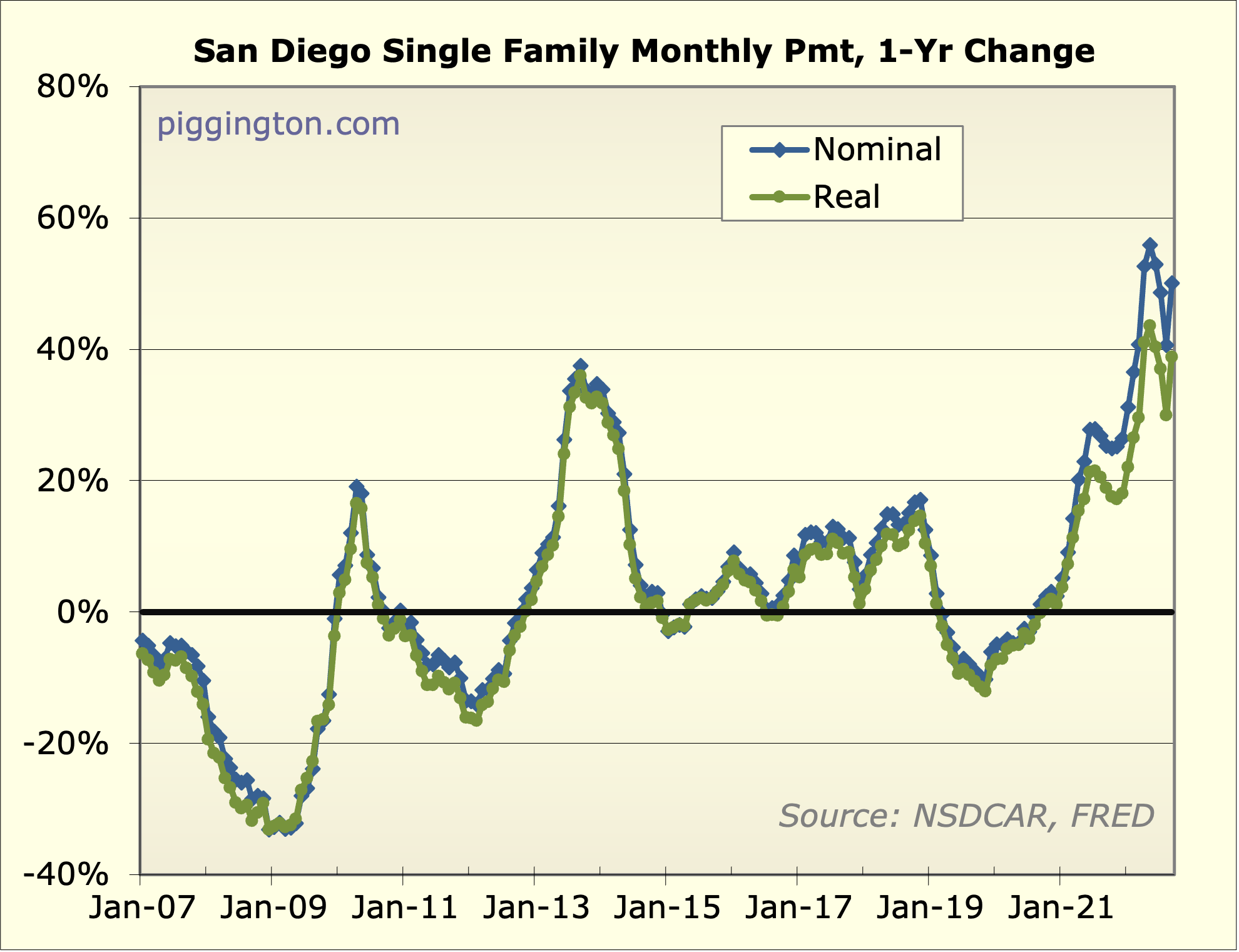

The most interesting chart for me is the monthly payment chart. Given how most home buyers borrow money to buy, that chart is more important IMHO than the price of the home. With rates going bonkers, which drives up monthly payments to a level we haven’t seen since maybe the stagflation era of the late 70s, yet prices haven’t cratered. The biggest question is why? What’s even more interesting is, not only did it not keep on crashing, it actually reversed.

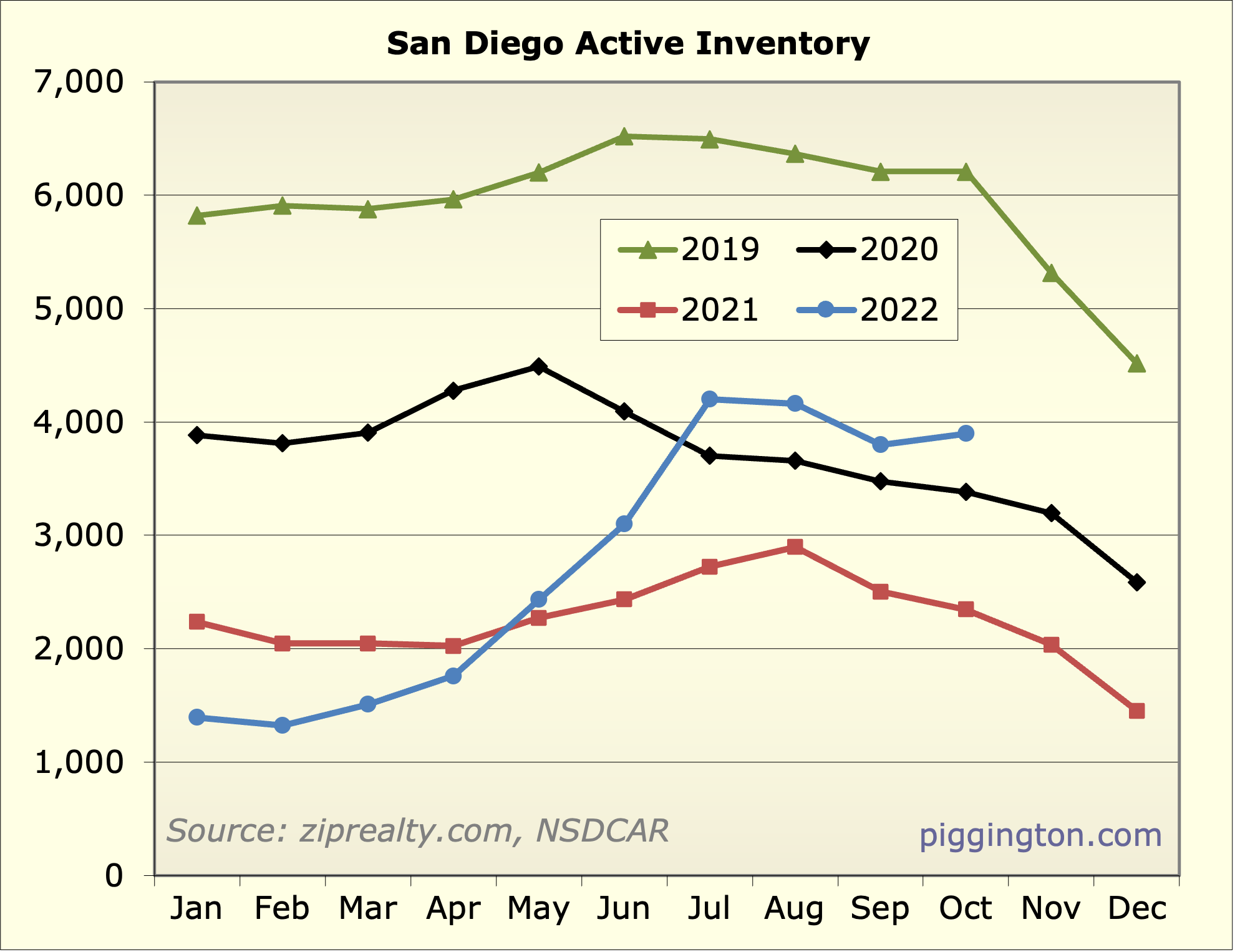

Once supply increases (which

Once supply increases (which I think it will), things are really going to go south fast.

Pbranding wrote:Once supply

[quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Why would anyone sell right now, unless they have to.

an wrote:Pbranding wrote:Once

[quote=an][quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Why would anyone sell right now, unless they have to.[/quote]

Well heading into a recession, increasing number of people will “have to”. Also, not unreasonable to try to capture whatever equity you’ve been able to build especially if you believe things will look worse for several years.

Pbranding wrote:an

[quote=Pbranding][quote=an][quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Why would anyone sell right now, unless they have to.[/quote]

Well heading into a recession, increasing number of people will “have to”. Also, not unreasonable to try to capture whatever equity you’ve been able to build especially if you believe things will look worse for several years.[/quote]

Why would you sell? Where would you live? It is easier to keep a roof over your head by renting out the other rooms and potentially live there for free while you’re unemployed. You’ve locked in extra low rate and housing cost for the next 30 years while rent is going bonkers. Also, if you sell, who will rent it to you if you have no job? Unless you think all these people will sell and be homeless or sell and buy in a much cheaper place for cash? No bank will loan to you if you have no job.

FWIW for anyone that says no

FWIW for anyone that says no one would do that, I had clients that were in late 50’s during last downturn. They lost their jobs and lived in a nice 5BR 4,000 sq ft. They had 2 or 3 tenants renting rooms for a few years to get them through it. Once prices recovered enough they sold and retired. With rates as low as they were the last few years they would have been in a far stronger position to get through it but they made it anyway. People will do what they have to to keep what they have here

Pbranding wrote:Once supply

[quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Nah I think the worst is over. They already went “south fast”. If you were out there actively shopping you’d realize that prices adjusted quickly. Give the data time to catch up. There will be more declines but there is no additional south fast coming around here. Just not seeing that in data

sdrealtor wrote:Pbranding

[quote=sdrealtor][quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Nah I think the worst is over. They already went “south fast”. If you were out there actively shopping you’d realize that prices adjusted quickly. Give the data time to catch up. There will be more declines but there is no additional south fast coming around here. Just not seeing that in data[/quote]

Respectfully disagree. The data is still based on lower interest rates and months behind. Until interest rates start trekking back down I don’t think you can say the worst is behind us. Also the recession hasn’t really impacted employment yet but I think it will.

Pbranding wrote:sdrealtor

[quote=Pbranding][quote=sdrealtor][quote=Pbranding]Once supply increases (which I think it will), things are really going to go south fast.[/quote]

Nah I think the worst is over. They already went “south fast”. If you were out there actively shopping you’d realize that prices adjusted quickly. Give the data time to catch up. There will be more declines but there is no additional south fast coming around here. Just not seeing that in data[/quote]

Respectfully disagree. The data is still based on lower interest rates and months behind. Until interest rates start trekking back down I don’t think you can say the worst is behind us. Also the recession hasn’t really impacted employment yet but I think it will.[/quote]

That’s my point! What’s closing today and even more so happening out there pricewise already reflects a retreat back to the end of last year. Gonna take a while for data to reflect that reality. Throw another 10%ish nominal decline on top of say 20% inflation over what will be the last 3 years and we’ll be back where we should be in real terms. Not Armageddon but back to balance. That’s what matters

FWIW sitting where i do and looking at real time data the way i do gives me a really good feel for these things. I think my track record of predictions shows that pretty clearly

sdrealtor wrote:

FWIW sitting

[quote=sdrealtor]

FWIW sitting where i do and looking at real time data the way i do gives me a really good feel for these things. I think my track record of predictions shows that pretty clearly[/quote]

You’re looking at consumer/retail buyers, but that’s not who will move the market this time around.

The past decade has seen a ton of investment/speculation buyers, including big funds and corps, and they don’t act like consumers.

I’ve been watching for a rush to the exits by this group for years, and now I’m seeing signs of it in the financial press.

drboom wrote:sdrealtor

[quote=drboom][quote=sdrealtor]

FWIW sitting where i do and looking at real time data the way i do gives me a really good feel for these things. I think my track record of predictions shows that pretty clearly[/quote]

You’re looking at consumer/retail buyers, but that’s not who will move the market this time around.

The past decade has seen a ton of investment/speculation buyers, including big funds and corps, and they don’t act like consumers.

I’ve been watching for a rush to the exits by this group for years, and now I’m seeing signs of it in the financial press.[/quote]

Meh. I’m talking about around here and they are not big players here. real estate is local to a large extent

sdrealtor wrote:drboom

[quote=sdrealtor][quote=drboom][quote=sdrealtor]

FWIW sitting where i do and looking at real time data the way i do gives me a really good feel for these things. I think my track record of predictions shows that pretty clearly[/quote]

You’re looking at consumer/retail buyers, but that’s not who will move the market this time around.

The past decade has seen a ton of investment/speculation buyers, including big funds and corps, and they don’t act like consumers.

I’ve been watching for a rush to the exits by this group for years, and now I’m seeing signs of it in the financial press.[/quote]

Meh. I’m talking about around here and they are not big players here. real estate is local to a large extent[/quote]

In God We Trust. Everyone Else Bring Data:

https://www.sandiegouniontribune.com/business/story/2022-10-02/investor-home-purchases

Meh I’m the only one here who

Meh I’m the only one here who brings that level of data. The cash rich investors are mom and pops that hold homes as long term passive income or flippers that get in and out quickly. There are few if any large investor groups with significant portfolios of investment homes here. They just don’t exist to even a moderate level and won’t have an impact on our market. Other things have and will

sdrealtor wrote:Meh I’m the

[quote=sdrealtor]Meh I’m the only one here who brings that level of data.[/quote]

You haven’t done so here. That which can asserted without evidence can be dismissed without evidence.

Now, is there something wrong with either the U-T’s data or analysis? They gave some detail on both.

As for your other post, people can hunker down for only so long. These arguments for the alleged upward stickiness of real estate prices aren’t any more persuasive in 2022 than they were in 2005/6–or the early 90s, for that matter.

Just like the stock market, assets are valued based on the sale of other similar assets. If a small fraction of owners decide to bail at the same time, it will represent a large fraction of price movement and will have ripple effects throughout the economy.

The fact that the sales in question do not represent someone looking for another place to live (because they are investments) means more “retail” inventory is being added to the market and thus further depressing prices.

The coming recession will just add to all of this.

But by all means, present data to the contrary since that’s what this site is all about.

Follow my monitors. Weekly

Follow my monitors. Weekly data

You don’t understand how this works then. People hunkering down doesn’t mean everyone. It means more and in this case as the data is showing a lot more.

Owner of rental properties are seeing rents far above what they ever expected. It seems like a daily occurrence I’m talking to someone whose relative owns 2-5 houses here that’s funding a retirement and when they inherit then they plan on the same. Just regular folks that are long time residents.

Last year we had a huge drop in inventory which at the time i said presaged a market that was a powder key about to explode fueled by low rates

Guess what we’ve got this year? Much lower new inventory than last year! Guess what we don’t have this year? Low rates anymore! So we have anemic new listing counts far below what we’ve seen in past years with even more anemic demand. It’s hard to know what will happen but what wont is a market collapse

sdrealtor wrote:Follow my

[quote=sdrealtor]Follow my monitors. Weekly data

You don’t understand how this works then. People hunkering down doesn’t mean everyone. It means more and in this case as the data is showing a lot more.[/quote]

I called the bubble before this site was started and I nailed the 2009 bottom within weeks so maybe I do know something. I heard the same arguments back then, and you still haven’t presented any evidence.

[quote=sdrealtor]Owner of rental properties are seeing rents far above what they ever expected. It seems like a daily occurrence I’m talking to someone whose relative owns 2-5 houses here that’s funding a retirement and when they inherit then they plan on the same. Just regular folks that are long time residents.[/quote]

Selection bias: why are they talking to you? The plural of anecdote is not data.

They are getting those rents because we’ve had $trillions of liquidity pumped into the economy! My own upper middle class family has gotten north of $20k in cash over the last couple of years, and I know a ton of young people who made more on unemployment than they had ever made in their lives.

Now that party is pretty much over, and the investor class I cited will bolt for the exits once they can’t get the returns needed to service their highly leveraged properties. (The grandmas and grandpas who own & rent a few houses in my circle of acquaintances tend to be cheap as hell about updating their paid-for properties and seem content to collect the resulting lower rents. YMMV)

Another downward pressure locally is the well-documented net population loss we’ve seen in the past few years in SD and California generally. It was down by 45,000 from 2019-2021 in SD according to a couple sources I just saw, which is over 1%.

[quote=sdrealtor]Last year we had a huge drop in inventory which at the time i said presaged a market that was a powder key about to explode fueled by low rates

Guess what we’ve got this year? Much lower new inventory than last year! Guess what we don’t have this year? Low rates anymore! So we have anemic new listing counts far below what we’ve seen in past years with even more anemic demand. It’s hard to know what will happen but what wont is a market collapse[/quote]

With investors, especially the big corporate owners, it doesn’t matter how many sell. What matters is what they sell for because they will have to eventually mark their holdings to market.

With retail buyers, it’s all about the monthly payment. If you think mortgage rates will magically return to the fairytale land of sub-4% rates anytime soon, I’d like to hear your reasoning. The result is that the monthly payment devoted to principal will be smaller. Add in the layoffs that have already either happened or have been announced and you have the arrows all pointing in the same direction.

drboom wrote:

I called the

[quote=drboom]

I called the bubble before this site was started and I nailed the 2009 bottom within weeks so maybe I do know something. I heard the same arguments back then, and you still haven’t presented any evidence.

[/quote]

What are your predictions drboom? I’m all ears. How low and how fast will we bottom?

Pbranding wrote:drboom

[quote=Pbranding][quote=drboom]

I called the bubble before this site was started and I nailed the 2009 bottom within weeks so maybe I do know something. I heard the same arguments back then, and you still haven’t presented any evidence.

[/quote]

What are your predictions drboom? I’m all ears. How low and how fast will we bottom?[/quote]

I would love to know as well.

drboom wrote:

I called the

[quote=drboom]

I called the bubble before this site was started and I nailed the 2009 bottom within weeks so maybe I do know something. I heard the same arguments back then, and you still haven’t presented any evidence.[/quote]

2009 was not the bottom where I live. The bottom was around 2011. I bought December 2008 and a model match down the street sold for about 5% less in 2011-2012.

an wrote:drboom wrote:

I

[quote=an][quote=drboom]

I called the bubble before this site was started and I nailed the 2009 bottom within weeks so maybe I do know something. I heard the same arguments back then, and you still haven’t presented any evidence.[/quote]

2009 was not the bottom where I live. The bottom was around 2011. I bought December 2008 and a model match down the street sold for about 5% less in 2011-2012.[/quote]

There was indeed a dead cat bounce after 2009 that ended with a near-2009 bottom in 2011, but I’m talking about the bottom for SD County as a whole. Individual deals are always possible.

“It’s tough to make predictions, especially about the future.”

–Yogi Berra

Having said that, I do have some things to offer for consideration:

– Sale price to rent ratios always return to historical norms, with some period of “over-correction” below the historical average on the downside.

– Rents will have to come down because the gigantic government handouts are done and we’re headed toward a contracting economy. Those who think nominal prices will remain the same while inflation pushes down real prices should consider the decreasing wage pressures resulting from a weak labor market. This will naturally depress house values.

– A good deal of residential real estate has been bought up by investors over the past 10 years. They are equipped and disposed to dump those properties much more rapidly than regular homeowners, and they will be unsentimental about it.

Some data to consider:

– There are about 1,237,000 housing units in San Diego County (US Census Bureau, July 2021)

– Historically, annual sales volume has been around 42,000 “homes” in the last several years, or about 3.4% of total inventory. (Statista, 2022)

– The owner-occupied rate is about 54% (2016-2020, US Census Bureau)

If only a small fraction of that huge landlord group decides to bail at the same time (which is now getting some attention in the financial press–I have been predicting this for years!), they will swamp the market: instead of 4.5k/month of inventory selling into pent-up demand, it could easily be twice that trying to sell into dwindling demand.

drboom wrote:

There was

[quote=drboom]

There was indeed a dead cat bounce after 2009 that ended with a near-2009 bottom in 2011, but I’m talking about the bottom for SD County as a whole. Individual deals are always possible.[/quote]

County or national bottom is meaningless. We don’t buy the county; we buy houses in a particular zip code. Even more specifically, I am only looking at a particular area of a zip code. So, when the county bottom matters less to me than when the zip code bottom. There was no dead cat bounce between 2009-2011. I was following my area very closely and did not see any dead cat bounce.

drboom][quote=an][quote=drboo

[quote=drboom][quote=an][quote=drboom]

Having said that, I do have some things to offer for consideration:

– Sale price to rent ratios always return to historical norms, with some period of “over-correction” below the historical average on the downside.

– Rents will have to come down because the gigantic government handouts are done and we’re headed toward a contracting economy. Those who think nominal prices will remain the same while inflation pushes down real prices should consider the decreasing wage pressures resulting from a weak labor market. This will naturally depress house values.

– A good deal of residential real estate has been bought up by investors over the past 10 years. They are equipped and disposed to dump those properties much more rapidly than regular homeowners, and they will be unsentimental about it.

[/quote]

I agree with all this. I think there’s more pain to come. But how low and how fast I won’t venture to guess. I originally guessed a 10-20% drop back in June and most disagreed. Now I’m thinking it will even be worse.

So things you say you have

So things you say you have predicted for years haven’t happened? And now you’re basing your forecast on things you’ve been wrong about, or unsure about but hope will happen?

Still waiting on those predictions and I’m willing to wager on them. I have won every single bet I’ve made on this blog and never collected a single one. The losers always seem to vanish once proven wrong

And not that I’m predicting rates but they dropped 1/2% today

And one more thing. The main reason people leave is because it’s too expensive here. What do you think will happen if it gets less expensive here? Any chance that could cause some of them to come back? Others to come here? No that couldn’t happen

drboom wrote:

As for your

[quote=drboom]

As for your other post, people can hunker down for only so long. These arguments for the alleged upward stickiness of real estate prices aren’t any more persuasive in 2022 than they were in 2005/6–or the early 90s, for that matter.[/quote]

Neither 2005 and early 90s saw huge inflation and massive rate increase. Guess when’s the last time we saw huge inflation and massive rates increase. Then, let’s look at what housing prices did during that time.

[quote=drboom]Just like the stock market, assets are valued based on the sale of other similar assets. If a small fraction of owners decide to bail at the same time, it will represent a large fraction of price movement and will have ripple effects throughout the economy.[/quote]

Unlike the stock market, with housing, you must live somewhere, and time stops for no one. So, as people get older, they’ll move out of their parents’ house and must either rent or buy. If you see a collapse in buyers, that means there’s an increase in renters or a pent-up future renter because they’re still living at home. Why would landlord sell when there’s a pent-up demand for rent a rent price keep rising.

Its so easy to get caught up

Its so easy to get caught up in a web of negativity. Yes we are in a declining market but armageddon is not upon us here

an wrote:

Unlike the stock

[quote=an]

Unlike the stock market, with housing, you must live somewhere …[/quote]

That “somewhere” appears to be Arizona, Texas, etc.

The data is pretty easy to find on this topic so I’ll leave it as an exercise for the reader.

drboom wrote:an wrote:

Unlike

[quote=drboom][quote=an]

Unlike the stock market, with housing, you must live somewhere …[/quote]

That “somewhere” appears to be Arizona, Texas, etc.

The data is pretty easy to find on this topic so I’ll leave it as an exercise for the reader.[/quote]So, you’re predict AZ and TX prices will go up because all the CA owners are selling and all the younger people who are moving out of CA to AZ/TX to buy there?

When and how much?

an wrote:drboom wrote:an

[quote=an][quote=drboom][quote=an]

Unlike the stock market, with housing, you must live somewhere …[/quote]

That “somewhere” appears to be Arizona, Texas, etc.

The data is pretty easy to find on this topic so I’ll leave it as an exercise for the reader.[/quote]So, you’re predict AZ and TX prices will go up because all the CA owners are selling and all the younger people who are moving out of CA to AZ/TX to buy there?

When and how much?[/quote]

Presumably they have already seen the price increases. They have been building like crazy, too: Texas had, by my arithmetic, 3.58X as many housing starts per capita compared to California in 2021 (ipropertymanagement.com for starts, Wikipedia for population). Arizona was even higher at 3.78X California.

In absolute terms, Texas had about 15k more starts than net immigration (~185k vs ~170k net immigration), while Arizona lagged (~48k starts vs. ~93k immigration). Texas likely over-built if you assume 2.5 persons per housing unit, while Arizona kept pace and maybe a little more.

California had ~69k starts and *lost* ~367k population in the same year!

drboom wrote:Presumably they

[quote=drboom]Presumably they have already seen the price increases. They have been building like crazy, too: Texas had, by my arithmetic, 3.58X as many housing starts per capita compared to California in 2021 (ipropertymanagement.com for starts, Wikipedia for population). Arizona was even higher at 3.78X California.

In absolute terms, Texas had about 15k more starts than net immigration (~185k vs ~170k net immigration), while Arizona lagged (~48k starts vs. ~93k immigration). Texas likely over-built if you assume 2.5 persons per housing unit, while Arizona kept pace and maybe a little more.

California had ~69k starts and *lost* ~367k population in the same year![/quote]

As they say, there are lies, damn lies, and statistics. As for lost in population statistics, who is moving out? Would these people be in any position to buy a house? If these are renters, why has rent gone up when population went down? Econ 101 would say, if you have decreased demand, price will go down.

an wrote:drboom

[quote=an][quote=drboom]Presumably they have already seen the price increases. They have been building like crazy, too: Texas had, by my arithmetic, 3.58X as many housing starts per capita compared to California in 2021 (ipropertymanagement.com for starts, Wikipedia for population). Arizona was even higher at 3.78X California.

In absolute terms, Texas had about 15k more starts than net immigration (~185k vs ~170k net immigration), while Arizona lagged (~48k starts vs. ~93k immigration). Texas likely over-built if you assume 2.5 persons per housing unit, while Arizona kept pace and maybe a little more.

California had ~69k starts and *lost* ~367k population in the same year![/quote]

As they say, there are lies, damn lies, and statistics. As for lost in population statistics, who is moving out? Would these people be in any position to buy a house? If these are renters, why has rent gone up when population went down? Econ 101 would say, if you have decreased demand, price will go down.[/quote]

“A couple trillion bucks’ worth of windfalls and unemployment benefits the likes of which we have never seen increased the supply of money” is what your Econ 101 professor would comment while he gave you a “D”.

As for your shopping preferences, this isn’t a microsite devoted to a specific 80 acres of San Diego County so most of us are going to be writing in somewhat more general terms.

drboom wrote:”A couple

[quote=drboom]”A couple trillion bucks’ worth of windfalls and unemployment benefits the likes of which we have never seen increased the supply of money” is what your Econ 101 professor would comment while he gave you a “D”.[/quote]Those trillions didn’t disappear in thin air. Also, unemployment benefits stop a long time ago. Why has rent kept on going up after the benefits ended? As for a D, if a professor thinks it’s as simple as a two-variable equation, then that professor suck and the D means nothing.

[quote=drboom]As for your shopping preferences, this isn’t a microsite devoted to a specific 80 acres of San Diego County so most of us are going to be writing in somewhat more general terms.[/quote] Not my shopping preference. The vast majority would not cross shop certain zip codes, much less cross state lines.

drboom wrote:”A couple

[quote=drboom]”A couple trillion bucks’ worth of windfalls and unemployment benefits the likes of which we have never seen increased the supply of money” is what your Econ 101 professor would comment while he gave you a “D”.[/quote]Those trillions didn’t disappear in thin air. Also, unemployment benefits stop a long time ago. Why has rent kept on going up after the benefits ended? As for a D, if a professor thinks it’s as simple as a two-variable equation, then that professor suck and the D means nothing.

[quote=drboom]As for your shopping preferences, this isn’t a microsite devoted to a specific 80 acres of San Diego County so most of us are going to be writing in somewhat more general terms.[/quote] Not my shopping preference. The vast majority would not cross shop certain zip codes, much less cross state lines. Bottom line is, you claim you called bottom and I pointed out that you were wrong. So, now you backed tracked and say, no, it was only in general term.

[quote=drboom]Indeed, Rich, thanks for the analysis and the community.

You, along with some of the great people who post here, helped my wife and I navigate the real estate market as we pursued the purchase of our first house. We’re newly minted homedebtors, and we owe another debt to all of you.

We will naturally sue you (along with Messrs. Case and Schiller) if the value of our house goes down–I mean, the graphs are pointing up, right? :-P[/quote]This was you in December 2009. You sounded a lot less confident than you do now.

an wrote:Bottom line is, you

[quote=an]Bottom line is, you claim you called bottom and I pointed out that you were wrong. So, now you backed tracked and say, no, it was only in general term.[/quote]

I’m not backtracking one bit. Go look at the Case-Schiller-based charts on this site, which aren’t for a three block section of Golden Hill or whatever, and you will clearly see the bottom of the market in nominal and especially real terms.

[quote=an][quote=drboom]Indeed, Rich, thanks for the analysis and the community.

You, along with some of the great people who post here, helped my wife and I navigate the real estate market as we pursued the purchase of our first house. We’re newly minted homedebtors, and we owe another debt to all of you.

We will naturally sue you (along with Messrs. Case and Schiller) if the value of our house goes down–I mean, the graphs are pointing up, right? :-P[/quote]This was you in December 2009. You sounded a lot less confident than you do now.[/quote]

Nice blast from the past!

My confidence was obviously high enough to buy into the market for 20+% down about 5 months earlier, using money saved over years from wages, not windfall money (and it makes a difference).

The joke about prices going further down was … a joke. We could already see the market creeping up in December 2009. I didn’t try to time the bottom, of course, as we’d made an offer on another house in February 2009 and then had a short sale fall through in April. The prices penciled out, so I got in the market. I felt there was some more downside[1], but that didn’t matter as we weren’t speculating on this but rather looking for a place to live and raise our kids without going broke. It’s been great for both. I never lacked any confidence in my market analysis or actual purchase.

If anything, I was a little smug for (a) getting the joint for $10k under the highest offer due to superior negotiating, and (b) getting 50% of our agent’s commission for the same reason. *Then* we got 8 grand back from the gubmint!

I was squawking about a housing bubble in 2003 and more in 04/05 when a delusional RE agent family member was showing us listings for $700k shacks in Encanto with a straight face. The part I got wrong was the timing: I never thought it would go on so long. We rented a cheapish apartment in late ’05 and I recall telling our elderly landlord that we were just hunkering down until the housing market crashed, which I figured would start in a year or two at most. I felt like the voice in the wilderness, but I never wavered. I ran across this site a few years later, right about the time people like Peter Schiff (a one-hit wonder for sure!) and Nouriel “Dr. Doom” Roubini were making the news, and I felt pretty validated.

[1] It’s easy to forget how we were all waiting for the the other shoe to drop when the tidal wave of ARM resets started to adjust! But the inconceivable happened with ZIRP and all the rest, and the Fed decided to screw all the prudent savers in favor of the irresponsibly leveraged asset “owning” class.

drboom wrote:I’m not

[quote=drboom]I’m not backtracking one bit. Go look at the Case-Schiller-based charts on this site, which aren’t for a three block section of Golden Hill or whatever, and you will clearly see the bottom of the market in nominal and especially real terms.[/quote]

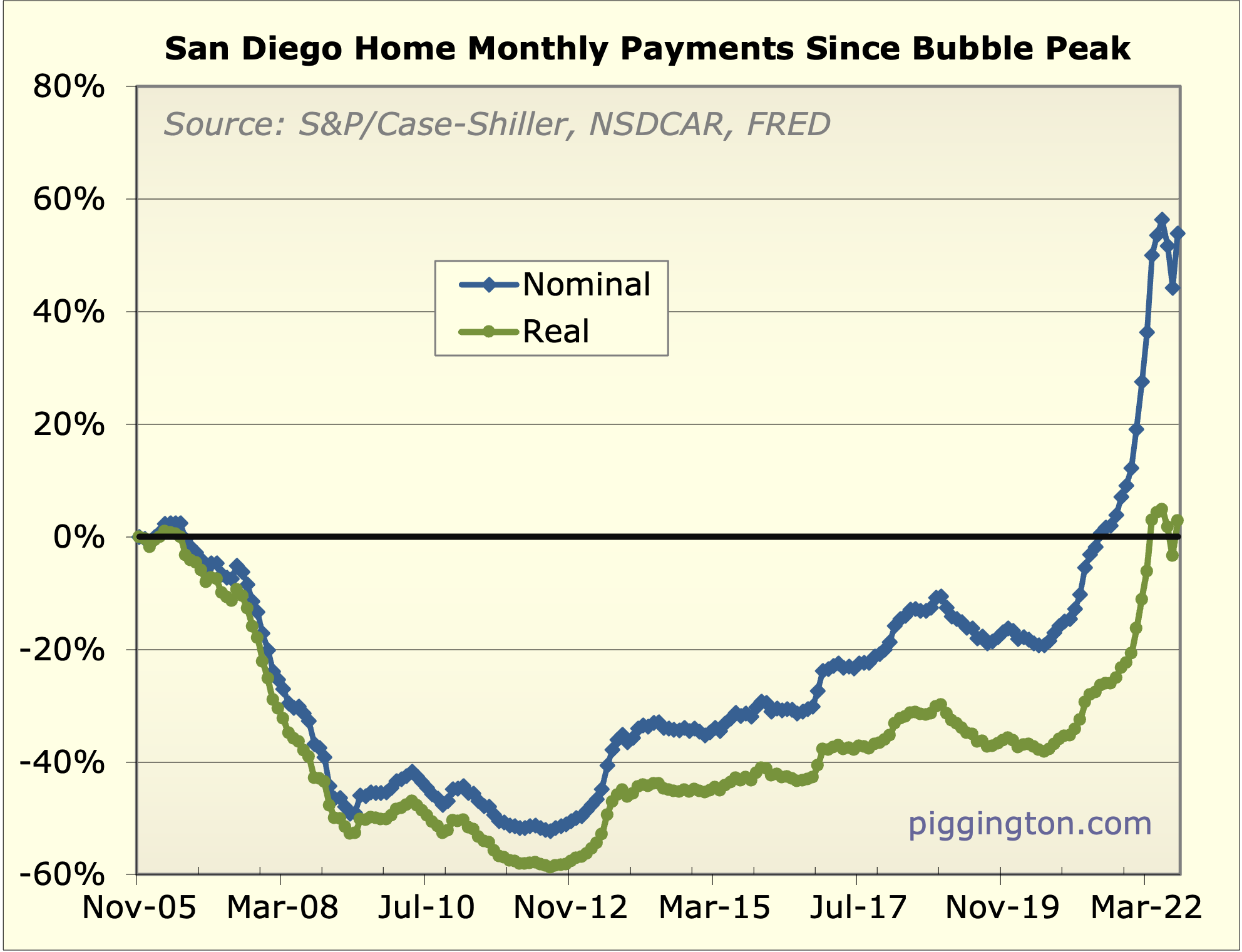

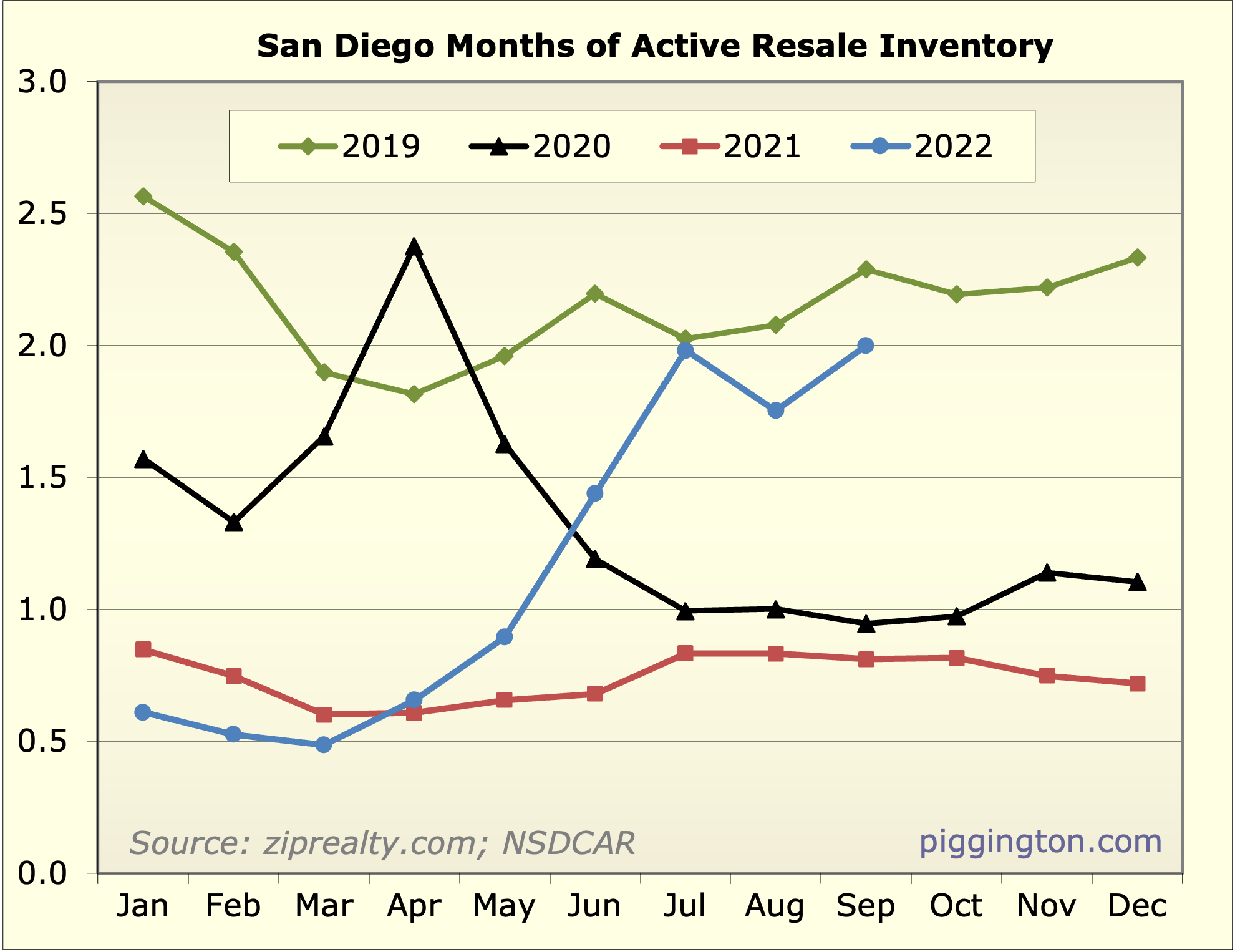

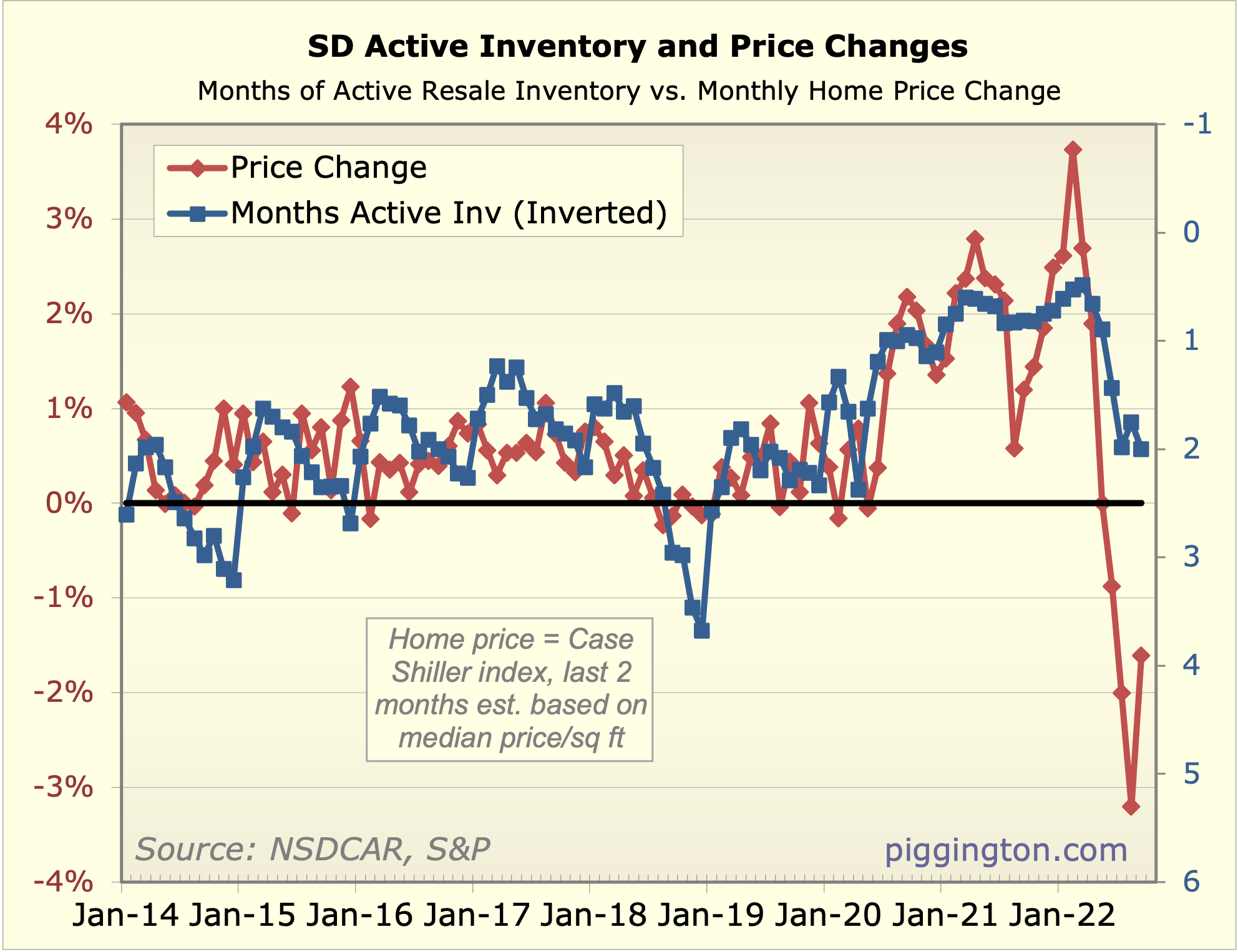

Since you financed your home like the vast majority of the buyers, the bottom was in 2011. Look at Rich’s chart for real payment. 2011 was ~5-10% below 2009. Also, we all know Case-Shiller number is delayed by a few months, as Rich pointed out in the past, so the “bottom” you saw in the Case-Schiller index already come and gone by the time you see it on the index.

As someone who did 150 short

As someone who did 150 short sales and was very active those years the bottom was most definitely 2011. In 2009 the statistics were essentially all short sales mostly of poor quality. In 2011 lenders were finally capitulating. By 2011 there were more traditional sales going on which is why the nominal numbers in the data might look a tad better. Either way anyone who bought between 09 and 12 hit it out of the park whenever and whatever they bought

an wrote:drboom wrote:I’m not

[quote=an][quote=drboom]I’m not backtracking one bit. Go look at the Case-Schiller-based charts on this site, which aren’t for a three block section of Golden Hill or whatever, and you will clearly see the bottom of the market in nominal and especially real terms.[/quote]

Since you financed your home like the vast majority of the buyers, the bottom was in 2011. Look at Rich’s chart for real payment. 2011 was ~5-10% below 2009. Also, we all know Case-Shiller number is delayed by a few months, as Rich pointed out in the past, so the “bottom” you saw in the Case-Schiller index already come and gone by the time you see it on the index.[/quote]

These things aren’t mutually exclusive: like a lot of people, I hit the sales price bottom in mid-2009 and then I re-financed a couple years later. I like big bottoms, I cannot lie.

I’m not claiming the mid-2009 bottom was a once-in-a-lifetime golden opportunity, mind you, and I already said I wasn’t trying to time the market in any case.

But the figures are what they are, and from a how-much-money-did-people-sell-their-houses-for perspective (aka health of the market), the buyer’s payment doesn’t matter.

I already disproved you that

I already disproved you that for the area I was interested in, the bottom for both price and payment was not 2009. Even though I did exactly what you did, I could have saved even more money if I waited until 2011. sdr have data on the ground at the time as well. City statistics only matter to talk about in generality. However, it does not help buyers who try to time the absolute bottom for the area you want to buy in.

Let me unpack this in detail

Let me unpack this in detail so we’re on the same page:

[quote=an]I already disproved you that for the area I was interested in, the bottom for both price and payment was not 2009.[/quote]

You’ve made some assertions about a specific area, sure, and I guess you and a few dozen others have a long-term interest in it. I and most other people live and work in a larger world, however, so I think you’re unduly limiting the discussion.

[quote]Even though I did exactly what you did, I could have saved even more money if I waited until 2011.[/quote]

Maybe you could have, and maybe not. All sales unique. But again: the health of the market as it is commonly understood is NOT driven by buyers’ payments. We don’t get payment appraisals, REITs don’t mark payments to market, etc. … the sales value, estimated or actual, is what matters in this context.

[quote]sdr have data on the ground at the time as well. City statistics only matter to talk about in generality.[/quote]

I don’t really have time to talk about every house, individually, in San Diego County–do you? It’s obvious that there are exceptions to broader trends at the single house or neighborhood level, but you’ll be hard pressed to find anyone else to share your narrow geographic interests with.

[quote]However, it does not help buyers who try to time the absolute bottom for the area you want to buy in.[/quote]

Timing the market requires a crystal ball. You only know if you achieved it in retrospect.

Bottom line: Sales price is KING. All the lower interest (i.e. payment) rates did in the last several years is allow people to more easily put themselves in a position to be underwater with no way out. Interest rates won’t be going back down to where they were anytime soon, and the share of income that can be allocated to housing is fairly inelastic so something has to give.

sdrealtor seems to think people are going to shackle themselves to their houses indefinitely or something, which I find unrealistic.

No one buy a San Diego house.

No one buy a San Diego house. We all buy a specific house. So, while it’s fun to use statistics to talk about things in general, it does not help any buyer. Some zip code could have peaked and bottom earlier/later. You used yourself and your own purchase as to why you made the call perfectly in 2009 as the bottom. Care you share your zip code? You do not live in a San Diego house. You live in your house in a specific zip code. So, no you and most other people do not live in a larger world, we all live in our house that we bought in a specific zip code.

As for the health of the market, payment is key because most people buy with a loan. If mortgage payment is drastically below rent, then you’ll have a flood of buyers jumping in to save money.

BTW, no one today is under water if they bought it 2+ years ago, so I have no idea what you’re talking about. As a matter of fact, if you bought 2+ years ago, you could easily rent out your house for a profit today.

drboom wrote:Maybe you could

[quote=drboom]Maybe you could have, and maybe not. All sales unique. But again: the health of the market as it is commonly understood is NOT driven by buyers’ payments. We don’t get payment appraisals, REITs don’t mark payments to market, etc. … the sales value, estimated or actual, is what matters in this context.[/quote]

Uh, yes, I could have since the house was a few houses down the street on the same side of the street in similar condition.

BTW, show me some data, not statistics. You know what they say about statistics. If you don’t understand what median means, then I can’t help you.

Once again you are completely

Once again you are completely twisting my assertions. I never said every homeowner would shackle themselves to their homes. I said a lot more people would dig and/or hold onto homes longer. So in your larger market theory that doesn’t mean zero inventory it means significantly less inventory. When balanced out against whatever demand is out there less supply naturally keeps prices higher than more supply does. As for the market, bottom, during the downturn, I was doing dozens of short sales all over Southern California, not only did I do them in San Diego, but I did them in various parts of Riverside County, Orange County, San Bernardino, county, LA County and even Ventura county. I had as good a sense of what was going on as anyone, as I was negotiating deals all over every single week. I know when the bottom was, and when lenders were capitulating the most.

sdrealtor wrote:Once again

[quote=sdrealtor]Once again you are completely twisting my assertions. I never said every homeowner would shackle themselves to their homes. I said a lot more people would dig and/or hold onto homes longer.[/quote]

You claim they will do it in such numbers and with enough tenacity that it will put a brake on the market, which I assert would require something like “shackles.”

[quote]So in your larger market theory that doesn’t mean zero inventory it means significantly less inventory. When balanced out against whatever demand is out there less supply naturally keeps prices higher than more supply does.[/quote]

A) What makes you think this layoff tidal wave is going to generate support for anything close to the prices we have now? People don’t actually have to lose their jobs to have an effect on the market: uncertainty breeds caution, and the headlines are full of bad news right now.

B) Because the market is heavily based on comps, all that needs to happen is for some highly leveraged landlords to see rents dropping. They’ll cut their losses and reset the bar downward for everyone else–they’d be fools not to. The market will supply the momentum from there as usual.

The days of financial electroshock therapy are over now that we have a Teahadi House all set to obstruct anything the Cadaver-In-Chief might want to do in the way of bailouts, so the economy is going to have to take its long-delayed medicine.

[quote]As for the market, bottom, during the downturn, I was doing dozens of short sales all over Southern California, not only did I do them in San Diego, but I did them in various parts of Riverside County, Orange County, San Bernardino, county, LA County and even Ventura county. I had as good a sense of what was going on as anyone, as I was negotiating deals all over every single week. I know when the bottom was, and when lenders were capitulating the most.[/quote]

If you know something Messrs. Case and Schiller don’t or didn’t, then OK! I’m just reading their processed data as presented by our host.

They already have and are

They already have and are doing it in such numbers. Follow my monitors and you’ll see the weekly data. A brake slows a car down it doesn’t always stop it

Unemployment is back near all time lows. If it doubles or even triples 90% will still be employed. We are in a low sales volume environment. People dig in and stay put limiting inventory and those that have to move? Well they have to move!

Landlords have enjoyed skyrocketing rents. A pullback won’t hurt them en masse and they surely don’t want to pay massive capital gains taxes. Real estate is leveraged and tax favored which is why they hold it long term. They would have to die en masse to get step up in basis for large scale liquidation and even so most heirs will hold onto them especially here.

I do know something. That data they use is all self reported less than reliably by real estate agents and those dudes don’t get into what is in the mix they just look at macro data. They sit up in ivory towers.

Btw the bigger point here is

Btw the bigger point here is one of my mantras. As a buyer you want to get in when most of the damage is done and catching the exact bottom isn’t that important. That’s because the upside is so big in a recovery around here. The other part is you want to buy on the way down not the way up. As an entry level buyer you want to buy when others don’t want to in order to be able to compete for the good ones. Once the ship turns upward youre road kill against the big money

sdrealtor wrote:Btw the

[quote=sdrealtor]Btw the bigger point here is one of my mantras. As a buyer you want to get in when most of the damage is done and catching the exact bottom isn’t that important. That’s because the upside is so big in a recovery around here. The other part is you want to buy on the way down not the way up. As an entry level buyer you want to buy when others don’t want to in order to be able to compete for the good ones. Once the ship turns upward youre road kill against the big money[/quote]

Not to mention, you’re buying a specific house in a specific area (especially if you want a view lot), so the bottom for the city matters less to you. Especially if you are buying in an older area. Some floorplans seldom come on the market and when it comes one, it might not be at the bottom or when it is the bottom, there’s nothing you want to buy. It all depends on how picky you are and what you’re looking for.

I have been eyeing a handle of houses in my specific area for the last 2 decades and none of them have come on the market :-(.

First 4 reporting weeks of my

First 4 reporting weeks of my NCC monitor for NOV

2020 – 82 new sfr listings

2021 – 47 new sfr listings

2022 – 38 new sfr listings

If that isnt digging in what is?

sdrealtor wrote:First 4

[quote=sdrealtor]First 4 reporting weeks of my NCC monitor for NOV

2020 – 82 new sfr listings

2021 – 47 new sfr listings

2022 – 38 new sfr listings

If that isnt digging in what is?[/quote]

Using your reporting for MM

2021 – 29 new SFR listings

2022 – 15 new SFR listings

Kinda crazy, considering MM has over 74k people and 23k households

Why do I feel like I’m

Why do I feel like I’m arguing with Lawrence Yun? 😛

From a call I was on today.

From a call I was on today. An incredible 89% of everyone with a mortgage in California has a fixed rate of 5% or lower. Unbelievably 71% have a rate of 4% or lower. Nearly a third, 29% have a rate of 3% or lower (Im one of them). As a result of rates at around 7% today, more and more homeowners are opting to not move. They are “hunkering down”

Hey Rich, do you think that

Hey Rich, do you think that it may be time to call the housing market as being frothy? Considering the serious reversals in sales and inventory, coupled with monthly payment on par with the last downturn.

pluto wrote:Hey Rich, do you

[quote=pluto]Hey Rich, do you think that it may be time to call the housing market as being frothy? Considering the serious reversals in sales and inventory, coupled with monthly payment on par with the last downturn.[/quote]

I’m not sure what that question means… are you asking whether I think housing was in a bubble? The answer is no, I do not, and did not think that — I thought housing was very overpriced and very risky, but not a bubble in the “irrational mania” sense. Much more on that topic here: https://pcasd.com/whats-going-on-with-housing/

Basically there was a lot of interest rate risk embedded in house prices; what we are seeing is that risk coming to the fore. That’s different from a bubble in my view.

Rich Toscano wrote:pluto

[quote=Rich Toscano][quote=pluto]Hey Rich, do you think that it may be time to call the housing market as being frothy? Considering the serious reversals in sales and inventory, coupled with monthly payment on par with the last downturn.[/quote]

I’m not sure what that question means… are you asking whether I think housing was in a bubble? The answer is no, I do not, and did not think that — I thought housing was very overpriced and very risky, but not a bubble in the “irrational mania” sense. Much more on that topic here: https://pcasd.com/whats-going-on-with-housing/

Basically there was a lot of interest rate risk embedded in house prices; what we are seeing is that risk coming to the fore. That’s different from a bubble in my view.[/quote]

In the article above, you write “If the inflation-worriers turned out to be right, and rates broke above their pre-pandemic range, perhaps mortgage rates might rise to 6%… To offset the affordability hit from a 6% mortgage rate, home prices would have to drop by 30%.” Now that we’ve passed 6%, and at 7% do you envision a 30%+ price decline?

Pbranding wrote:

In the

[quote=Pbranding]

In the article above, you write “If the inflation-worriers turned out to be right, and rates broke above their pre-pandemic range, perhaps mortgage rates might rise to 6%… To offset the affordability hit from a 6% mortgage rate, home prices would have to drop by 30%.” Now that we’ve passed 6%, and at 7% do you envision a 30%+ price decline?[/quote]

In October 2021, small 3/2 houses in Mira Mesa were in the high 700k. If we see a 30% decrease, those houses should be in the mid to high $500k range. I sincerely hope that Rich is right. Right now, those houses are going for mid to high 800s.

an wrote:If we see a 30%

[quote=an]If we see a 30% decrease, those houses should be in the mid to high $500k range. I sincerely hope that Rich is right.[/quote]

I did not predict a 30% price decline; see my comment above.

Pbranding wrote:

In the

[quote=Pbranding]

In the article above, you write “If the inflation-worriers turned out to be right, and rates broke above their pre-pandemic range, perhaps mortgage rates might rise to 6%… To offset the affordability hit from a 6% mortgage rate, home prices would have to drop by 30%.” Now that we’ve passed 6%, and at 7% do you envision a 30%+ price decline?[/quote]

No, that was not a prediction about prices, it was just meant to illustrate the huge impact that rising rates could have, given how low rates had gotten. There are multiple ways for monthly payments to get more affordable, of which outright price declines are just one. The other two being an increase in fundamentals (rents/incomes), and rates declining. I am guessing it will be a combination of all 3.

PS I’m not ruling it out

PS I’m not ruling it out either; I just think it’s futile to predict nominal price changes if we don’t know the future path of the other two factors (rates, and nominal rents/incomes).

FWIW a 30% price decline would take us back to pricing only 2 years ago, Oct 2020. That just goes to show how crazy the last couple years were.

Losing 2 years’ worth of appreciation (less actually as the peak was a few months ago) doesn’t seem particularly implausible to me, generically speaking. There are a couple good counterpoints this time around.

– First, there was likely a one time step-up in the fair value of home prices, due to the remote work revolution. It’s unclear how much of the rise was due to that.

– Second, inflation has raged during that time, so there’s been unusual growth in incomes/rents.

There’s also a good counter to the counter: two years ago, 30 year rates were 2.8%. Now they’re over 7%.

Anyway these are just idle musings, I guess the point being to illustrate that a 30% decline isn’t actually a crazy forecast. But I’m not making that forecast. Again, there are 3 moving parts here: nominal prices, fundamentals, and rates. You can’t predict one without knowing what the other two will do. (And even if you did know that… it’s still pretty hard).

I fully agree with what you

I fully agree with what you said Rich. I’m 100% happy with price dropping or rent rising to the same rent vs PITI as it was 1-2 years ago. Only time will tell which of the 3 we’ll get. I don’t expect rates to go down in the next year, so, let’s see which will happen over the next year.

For some context, small 3/2 house in MM PITI was about 5-10% above rent last year. So, the same house today has a PITI of ~$5600/month. The rent of a similar house is currently $3800/month. So, rent would have to rise another 32% to get back to the same rent vs PITI ratio as it was a year ago.

So, either rent increase by ~30% or price dropping by ~30%…

So the interesting thing is

So the interesting thing is during the last bubble I thought worst-case scenario around me was 30% decline and that we would get less and we did. That’s because the big percentage gains came at the beginning when prices were lower. This time I pretty much guarantee that 30% declines are in the bank. That’s because the big gains happened at the end when prices were higher. It’s all about math and the later gains being easier to concede

sdr, I’m talking about 30%

sdr, I’m talking about 30% from here, not 30% from peak. If we’re taking about from peak, it would have to be 50% at today’s rate.

Agree 100%

Agree 100%