I have bought a house in San Diego. I’m also going to start

putting up guest posts by Ted McGinley.

This (the house buying part) shouldn’t be a huge shock for people

who’ve been reading the site of late, because I’ve talked a lot

about how it makes sense to buy in certain situations. That

said, I will briefly outline my thought process here.

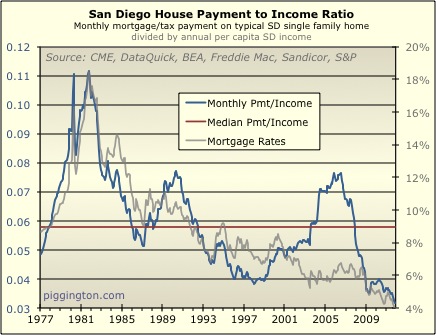

After the recent leg down in interest rates, monthly payments are

the lowest compared to incomes and rents than they’ve been in the

history of the data, and are quite dramatically below their median

historical levels:

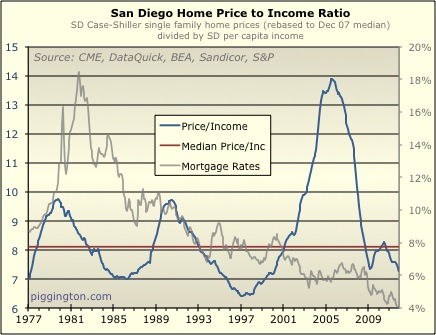

I frequently point out that when it comes to determining whether homes are

overvalued or undervalued, the price-based ratios are far more

important than payment-based ratios. However, as I discussed

in this

article, an individual buyer should be more interested in the

expensiveness of the monthly payment, rather than the purchase

price, if he or she is financing most of the purchase and intends to

(or is at least able to) keep the home indefinitely.

A buyer in these circumstances is not only locking in rock-bottom

monthly payments, but, crucially, is

doing so ahead of what I believe will be a period of unusually

high inflation.

Now, I don’t want to turn this into a big discussion on the

something-flation debate, because that topic been thoroughly beaten

to death elsewhere on this site as well as on my “day job” site, and

it is beside the central point of this article. Suffice it to

say that I consider it a high-confidence forecast that the dollar is

going to lose a lot of purchasing power in the years ahead, because

nominal incomes — and thus prices, including those of rents and

maybe even houses, a little — must

be made to rise (in excess of any plausible level of

economic growth, i.e., via inflation) if the country is to be able

to continue servicing its tremendous and growing debt.

If this outlook is correct, as I believe it is, then today’s

ultra-low rates make this an ideal time to take out a chunky 30-year

fixed mortgage, and to sit back and let inflation hew away at the

real value of the mortgage and the monthly payments over the years

to come.

So, the missus and I went out looking for homes. We only found

one in our price range, a single family house in Bay Park, that we

thought was awesome enough to be a long-term home. So we made

an offer, got a loan with as low a down payment as we could get away

with, and have now re-joined the ranks of the titular Landed Poor.

And now I will attempt to anticipate some questions:

Q:

Does this mean you think this is the bottom for home

prices?

A. Not really. I

don’t know when the bottom will be, but it really doesn’t matter all

that much as I’ve financed most of the property and I’m more

interested in minimizing monthly payments than the purchase

price. For what it’s worth, my (not very high-confidence)

prediction on home prices is that valuations

will continue to slowly decline for a while, but nominal prices will kind of bounce

along and not do anything too dramatic in either direction any time

soon (barring an interest rate spike… see 3 questions down).

Q:

OK, does this mean

you think this is the bottom for monthly payments?

A. I suspect that it’s

awfully close, at least in terms of level (I have less of an opinion

on duration). But my investing philosophy is that you

shouldn’t get too caught up on catching the exact top or bottom,

because it’s impossible to do so with any reliability. If

something is a great deal, you can be greedy and wait for it to

become a super-great deal — but there’s a good chance that’s not

going to happen, leaving the possibility that the train will leave

the station without you. I believe that long-term investing

success (and far lower stress levels) will come from being

disciplined about buying things that are cheap and selling things

that are expensive, not by getting overly worked up about whether

you caught the exact peak or trough.

I sat out an inflation-adjusted home price decline of almost 50%,

and now I’m buying at a time when prices are cheaper than normal and

monthly payments at 45% below their historical median. That’s

close enough for me.

Q:

Monthly payments

may be cheap, but homes are still overpriced.

A. Not so. Not in

the aggregate, anyway:

As of November, San Diego homes were 10% undervalued based on the

historical ratio of home prices to San Diego incomes. Of

course, individual markets may vary from this aggregate figure, and

there are always issues with even the best price indicators, so

buyers should (and we did) verify that their target homes are

reasonably priced compared to area rents. On the whole,

however, the argument that San Diego homes are overpriced is not

supported by the data.

Q:

Won’t interest

rates go up a lot, and won’t that push down home prices?

A. Yes, it’s certainly

possible that rates could rise a lot, possibly to a shocking

degree. And this could indeed put downward pressure on home

prices. There’s actually very little correlation between

interest rates and home valuations, and if anything, homes have

tended to get more expensive in rising rate environments (due to

rising rates typically being accompanied by rising wages, as well as

other external factors). However, I think that a sufficiently

steep and abrupt rate rise could really hurt home prices.

But recall that I am more concerned with minimizing monthly payments

than the purchase price. If rates rose enough to really impact

prices, it’s likely that those higher rates would have affected

monthly payments even more. So for a long-term, heavily

leveraged purchase, the threat of rising rates is a reason to act

sooner rather than later.

Q:

Ted McGinley was

president of the Alpha Betas. Don’t you think you’re more

Tri-Lamb material? Consider the following:

A. That’s just mean.

I appreciate you coming out

I appreciate you coming out of your mortgaged closets about the purchase. Congratulations. I bought in June 2011 for the same exact reasons and I will probably refinance soon in order to get the current lower rates. It’s comforting to know that whatever happens to rent prices or the value of the dollar, my mortgage will never increase.

And Bay Park is a great neighborhood, I wish I could have afforded a house there.

A big congratulations to you

A big congratulations to you both! 🙂

How do you like being homeowners? Is it better than expected after all these years (like scaredy’s purchase)?

Nobody can ever say that you didn’t do your homework regarding your purchase, and you were smart to mortgage as much as possible, whether we get inflation or deflation — locking in payments if we get inflation, and having money on the side if we get deflation.

Your analysis is spot-on WRT payments…not to mention the fact that the govt/Fed can prop up prices long enough to diminish the “savings” from buying at a lower price because of rent paid while “bubble-sitting.”

I can’t believe you actually did it!

Nerds rule!!!!!! 🙂

Congrats on the purchase.

Congrats on the purchase. While you probably felt you had to include a personal justification for you choice you owe no one an explanation. Your blog has helped countless people avoid economic calamity and that makes you a bit of a hero in my eyes. You did what you feel is right for yourselves. That’s good enough me, should be good enough for others and if not, that’s their problem not yours. Nicely done sir!

(No subject)

Traitor !

Just kidding, you

Traitor !

Just kidding, you can hang with the Alpha Betas if you want.

On the house thing, though, nice work. Got views ?

You ended up in my old ‘hood. I miss it, want to move back to Bay Park at retirement in 10 (one can hope, right?) or 20 years.

I guess the only downside is that now when you use the term “Landed Poor” it might be taken slightly differently and you also may have lost your last shred of credibility with the perma-bears (I guess that’s not a bad thing).

Good Luck !

Congrats on your recent

Congrats on your recent purchase, Rich! Agree with dimmer that Bay Park is a great area for many reasons and you will not regret owning and living there!!

It’s safe to buy a house,

[img_assist|nid=15782|title=It’s safe to buy a house, now!?|desc=|link=node|align=left|width=300|height=312]

NEERRRRDSS!!!!!

[img_assist|nid=15781|title= NEERRRRDSS!!!!!|desc=|link=node|align=left|width=300|height=265]

Thanks everyone.

CAR –

Thanks everyone.

CAR – Thank you… yes, it’s really be nice to be “in control” once again, and able to completely dial the place in. That’s appealing for someone whose main goal is to never leave the house. 😉

SDR – Thanks for the sentiment… I agree, but I’ve given the decision a lot of thought and I hoped it might be helpful to some people if I explained my rationale.

FSD – Yes, we have a very nice view of Mission Bay.

afx and speaker — With the inclusion of both nuke the fridge and Ogre references, this thread is now complete!

Thanks everyone.

CAR –

Thanks everyone.

CAR – Thank you… yes, it’s really be nice to be “in control” once again, and able to completely dial the place in. That’s appealing for someone whose main goal is to never leave the house. 😉

SDR – Thanks for the sentiment… I agree, but I’ve given the decision a lot of thought and I hoped it might be helpful to some people if I explained my rationale.

FSD – Yes, we have a very nice view of Mission Bay.

afx and speaker — With the inclusion of both nuke the fridge and Ogre references, this thread is now complete!

Toscano Jumps the Shark!

[img_assist|nid=15784|title=Toscano Jumps the Shark!|desc=|link=node|align=left|width=300|height=225]

FormerSanDiegan wrote:Toscano

[quote=FormerSanDiegan][img_assist|nid=15784|title=Toscano Jumps the Shark!|desc=|link=node|align=left|width=300|height=225][/quote]

The animatronic corpse of Harold Akers will come get you there.

He will show up in your living room standing behind you while you are watching tv and ask in a wheezy midwestern accent “Rich, clean up your room”.

Great job Rich!

I think we

Great job Rich!

I think we would be extremely hard pressed to find any PIGGs out there who have not yet purchased a home.

Now what are we gonna talk about?

I bought a persimmon tree an

I bought a persimmon tree an apricot tree and an Asian pear tree this weekend.

And also a lot of cacti.

I would not have bought those things had I not bought a house.

I suppose we could talk about landscaping.

I appreciate your q and a above.

Sounds reasonable.

Rich,

Firstly, congrats to

Rich,

Firstly, congrats to you both.

Secondly, thanks for the website that helped me and my wife avoid the bubble, and take advantage of successfully timing the market.

In the 2003/2004 time frame I began thinking along the same lines that you were and began looking for info on real estate, because I had no understanding of it aside from buying a place in LA during the early nineties and losing about 19 % of its value. Once bitten, twice shy, and then some.

Holding off for as long as we did was a constant battle with the missus. But now, even she has come around to my way of thinking – waiting was worth it.

Best to you both and big, big thanks for creating a forum for folks like us to benefit from!

Congrats Rich.

@ SD

Congrats Rich.

@ SD Realtor: You’d be surprised. Some of us are still lying in the weeds, waiting to pounce.

woodrow there is nothing

woodrow there is nothing wrong with waiting in the weeds. As long as you know what you are waiting for then you are fine. Personally I think that for those who are heavy with cash waiting for interest rates to run up very high is a good idea. That may take quite awhile but there is nothing wrong with that strategy.

I’m wondering how long it

I’m wondering how long it takes the main stream media or a clever real estate marketing firm to capatalize on this development. Diana Olick should write an article with the title “pioneer housing bubble blogger buys home.” Since I’m sure she reads this blog and has a secret crush on me, I’ll consider it a wink my way if that is the title of the article.

But seriously, how many NAR types have you mowed down over the years, at the very least Chamberlain will mention this on the radio as evidence that it’s now time to buy. Only this time, the data will be on their side.

Congrats on the purchase! It’s been a long road, thanks for letting us ride along.

p.s., I emailed Diana a link to this thread, I couldn’t help it.

This is such big news,

This is such big news, someone told me in the hall before I read it here ! I didn’t even know this person was a reader.

I have been shopping for move-up properties in Carmel Valley lately. Still likely 6 to 24 months away for me, but I’m seeing plenty of things I could both live in and afford.

There is something to be said for the addage that “The right time to buy a house is when you are ready.” so whether or not you timed it perfectly is not significant. It’s close enough and, it seems, you are ready.

I love Bay Park. Most people in Clairemont wish they lived in either Bay Park or UC.

By the way, “Revenge of the Nerds” was filmed on campus at the University of Arizona.

you should let all the piggs

you should let all the piggs take you for a drink to celebrate at the HighDive (tho i’ve never actually been in there)! congrats man

CafeMoto wrote:you should let

[quote=CafeMoto]you should let all the piggs take you for a drink to celebrate at the HighDive (tho i’ve never actually been in there)! congrats man[/quote]

I’m taking Rich to Donovan’s for dinner next December. The best part is I wont be picking up the tab. Another Pigg will have that honor on the losing end of a bet made about 5 years ago. Sometimes the realtors win too 🙂

sdrealtor wrote:CafeMoto

[quote=sdrealtor][quote=CafeMoto]you should let all the piggs take you for a drink to celebrate at the HighDive (tho i’ve never actually been in there)! congrats man[/quote]

I’m taking Rich to Donovan’s for dinner next December. The best part is I wont be picking up the tab. Another Pigg will have that honor on the losing end of a bet made about 5 years ago. Sometimes the realtors win too :)[/quote]

LOL! We’ll see about that. It’s not over, yet!

I think all the bears have now jumped off the fence. Where will all the buyers come from? 😉

It would be my pleasure to pick up Rich’s tab, no matter who wins. He’s been the source of sanity over the years, and we are forever grateful to him for all the effort he’s put into gathering and analyzing the data and maintaining this blog.

CAR – Thank you for the kind

CAR – Thank you for the kind words! And Donovan’s is my favorite… 😉

Thanks to everyone else on the thread, too, for the good wishes… much appreciated.

Rich, in your situation that

Rich, in your situation that was a great buy. Here’s a tip, before you call somebody to do some work on your house, ask yourself if you a smarter than the guy you are calling. btw, I asked McGinley what he thought of your purchase:

http://www.youtube.com/watch?v=Sm02Rbd7vVM

Rich, this is awesome news!!!

Rich, this is awesome news!!! This Piggington Indicator is probably the best buy signal than anything else out there. Especially the neighborhood as well. A view home in an established coastal neighborhood is much harder to find at a good price too. This is exactly how Piggs have acted over the last few years. Piggs in temecula started buying first, then gradually selected new but hard hit areas within the county, now penetrating into established highly sought after neighborhoods. I can almost envision a map of gradual movement of Pigg purchases from the inland/suburb moving toward the coast/center.

Now it is time to get to know your local home depot really really well. 🙂 btw, does this also mean home improvement stores are now a “buy”?

And lastly… The Nerds do eventually triumph!!!

Can I come park my RV in

Can I come park my RV in front of your house? Just kidding. Guess you’ll be going to Costco ,Home improvement stores a lot. Do you have a pickup yet? Congratulations Rich! A house 2 doors down from me just went into escrow the other day. Makes one wonder with rents above mortgages in some places if silent seconds might be coming into fashion.

Congrats Rich! I lived in Bay

Congrats Rich! I lived in Bay Park for years and loved it, hope you do too!

My Bay Park favorites:

Same

My Bay Park favorites:

Same Old Grind (Coffee)

Mountain Mike’s Pizza

Siesel’s Meats

Summer Nights @ 9:50 pm

… and that Italian place that used to be at Burgener & Clairemont Drive (next to 99 cent store), but I think it closed down a few years ago.

Thanks FSD… definitely

Thanks FSD… definitely going to check these out (with Seisel’s on the short list 🙂

I’m not sure what qualifies

I’m not sure what qualifies one to be a Pigg, but I certainly haven’t bought a home yet. However, I have no reason to malign anyone who has. I guess it’s all about taking advantage of the unusual circumstances, rather than about principles. Being able to buy a home with very little down payment, with very cheap credit was what everyone railed against during the bubble. Now it’s OK because we have a better handle on it? I can’t help but keep asking myself how it’s all been made possible.

Good luck Rich. I also owe a debt of gratitude.

Jazzman, the issue in the

Jazzman, the issue in the bubble was that people were taking out debt that they couldn’t actually afford to service (via teaser rate loans, exacerbated because so many people were lying about their incomes). This is a completely different situation from taking out a fixed rate loan that one can afford to service.

(Another difference is that they were taking out these loans to buy grossly overpriced assets).

ctr70, I loathe traffic noise too. That was on my very short list of instant disqualifications. There are places in Bay Park without it, you just have to go higher up the hill.

Rich Toscano wrote:Jazzman,

[quote=Rich Toscano]Jazzman, the issue in the bubble was that people were taking out debt that they couldn’t actually afford to service (via teaser rate loans, exacerbated because so many people were lying about their incomes). This is a completely different situation from taking out a fixed rate loan that one can afford to service.

(Another difference is that they were taking out these loans to buy grossly overpriced assets).

ctr70, I loathe traffic noise too. That was on my very short list of instant disqualifications. There are places in Bay Park without it, you just have to go higher up the hill.[/quote]

Yes, I am aware of that, but I’m not going to be the party pooper here. Congrats are in order and I wish you the best.

I checked out Bay Park a lot

I checked out Bay Park a lot myself looking, the one thing that bothers me about that area is you hear the freeway from everywhere. I’d look at these houses with great views, but then you would step out on the deck and hear that wonderful roar of highway 5. Same thing with a lot of Mission Hills down by the 5. I just have a major pet peeve that I can’t stand sitting in my house trying to relax or read and hearing the freeway, major road noise, or being in the airport jet path. Bugs the crap out of me. Other that that I think Bay Park is a great spot.

ctr70 wrote:I checked out Bay

[quote=ctr70]I checked out Bay Park a lot myself looking, the one thing that bothers me about that area is you hear the freeway from everywhere. I’d look at these houses with great views, but then you would step out on the deck and hear that wonderful roar of highway 5. Same thing with a lot of Mission Hills down by the 5. I just have a major pet peeve that I can’t stand sitting in my house trying to relax or read and hearing the freeway, major road noise, or being in the airport jet path. Bugs the crap out of me. Other that that I think Bay Park is a great spot.[/quote]

Bonsall

ctr70 wrote:I checked out Bay

[quote=ctr70]I checked out Bay Park a lot myself looking, the one thing that bothers me about that area is you hear the freeway from everywhere. I’d look at these houses with great views, but then you would step out on the deck and hear that wonderful roar of highway 5. Same thing with a lot of Mission Hills down by the 5. I just have a major pet peeve that I can’t stand sitting in my house trying to relax or read and hearing the freeway, major road noise, or being in the airport jet path. Bugs the crap out of me. Other that that I think Bay Park is a great spot.[/quote]

I’d trade in the crows in Clairemont for some freeway noise any day. Anyone else find there are more crows in their area than seems reasonable?

sdduuuude wrote:ctr70 wrote:I

[quote=sdduuuude][quote=ctr70]I checked out Bay Park a lot myself looking, the one thing that bothers me about that area is you hear the freeway from everywhere. I’d look at these houses with great views, but then you would step out on the deck and hear that wonderful roar of highway 5. Same thing with a lot of Mission Hills down by the 5. I just have a major pet peeve that I can’t stand sitting in my house trying to relax or read and hearing the freeway, major road noise, or being in the airport jet path. Bugs the crap out of me. Other that that I think Bay Park is a great spot.[/quote]

I’d trade in the crows in Clairemont for some freeway noise any day. Anyone else find there are more crows in their area than seems reasonable?[/quote]

Yes. Around this time last year, they started squaking outside my bedroom window at around 5 AM. They’re just starting to do it again this year. This link might interest you, though I can’t say I’ve taken advantage of it yet:

http://www.dfg.ca.gov/hunting/

ctrl-f crows

I should throw in the obligatory congrats to Rich, as this home purchase is big news for sure. Like so many others, this site helped to save me from myself.

There was a nice fish market

There was a nice fish market down in the flats off Morena? Is it still there??

And don’t forget Tio Leo’s 🙂

Congratulations Rich.

The

Congratulations Rich.

The fish market that BG mentioned might be Catalina seafood – make sure you wear close toed shoes or you can’t go in the back and pick your fish.

But it’s great… It’s behind Pacific Sales/Sear outlet – back by the train tracks. The freshest fish in town – and reasonable.

http://www.catalinaop.com/

And seconding the rep for the High Dive. Never been – but it’s been cool for at least 2 decades.

Haven’t checked that one out

Haven’t checked that one out but Bay Park Fish Company is top notch.

Love the blog, Rich, and congrats on the purchase.

bearishgurl wrote:There was a

[quote=bearishgurl]There was a nice fish market down in the flats off Morena? Is it still there??

And don’t forget Tio Leo’s :)[/quote]

Went to that Tio Leo’s twice last year. I’ll never go back. Nearly everyone was unhappy with their food. It was just – blah.

My wife lived in a condo just off the 15 for many years. You get used to the freeway noise because it fades into the background … unlike crows.

Congratulations, Rich!!!

I am

Congratulations, Rich!!!

I am so, so close to making the pounce. Scanning my neighborhood, there are some nice condos in my range now, and a duplex or two that is so, so close to my price-reach…

I want to hold out for something with a yard so that I can garden, so I guess now it is a race between my ability to save up that down payment, and the end of the bottom (if this is indeed the bottom for monthly payments, as you suspect.)

Will you still be doing this blog?

I live across the street from

I live across the street from a high school, and they’re currently re-doing the football field. Monster tractors came and tilled it up about 3 feet deep, and that day we had probably 100-200 crows picking off the scurrying vermin. It was a sight to see.

Be careful fucking with crows. They have been known to memorize faces and mess with people who mess with them. They don’t call a group of them a MURDER for nothing.

What you need is a pet hawk. They’ll keep the population in check. We have a lot of those as well, living near canyons. It’s always a good show seeing a hawk vs crow battle. It’s like Maverick vs the Migs up there.

CricketOnTheHearth

[quote=CricketOnTheHearth]

Will you still be doing this blog?[/quote]

Most definitely…

How low of a down payment %

How low of a down payment % can you get away with these days? Did you have to get PMI?

I do not see where you

I do not see where you figured in the total cost to own the home. If mortgage rates are 4% and annual depreciation of the house is 6%, then cost to carry the home is 10%, and renting looks a lot cheaper.

Why buy a home just because mortgage payments are cheaper than rent, if you eventually have to pay the piper and lose your downpayment and principal reductions on the mortgage?

It seems to me you did a monthly cash flow analysis and just ignored the balloon payment at the end. Isn’t that the same group-think that created the housing bubble?

creative_cpa wrote:I do not

[quote=creative_cpa]I do not see where you figured in the total cost to own the home. If mortgage rates are 4% and annual depreciation of the house is 6%, then cost to carry the home is 10%, and renting looks a lot cheaper.

Why buy a home just because mortgage payments are cheaper than rent, if you eventually have to pay the piper and lose your downpayment and principal reductions on the mortgage?

It seems to me you did a monthly cash flow analysis and just ignored the balloon payment at the end. Isn’t that the same group-think that created the housing bubble?[/quote]

A long-term 6% annual depreciation of home prices is, imho, an absurd assumption. (ref: price valuation chart + Ben Bernanke and his printing press).

In any event, it’s irrelevant because, as I explained in the post, I intend to hang onto the home indefinitely.’

BTW: I think you need to look up what “group-think” means.

creative_cpa wrote:I do not

[quote=creative_cpa]I do not see where you figured in the total cost to own the home. If mortgage rates are 4% and annual depreciation of the house is 6%, then cost to carry the home is 10%, and renting looks a lot cheaper.

Why buy a home just because mortgage payments are cheaper than rent, if you eventually have to pay the piper and lose your downpayment and principal reductions on the mortgage?

It seems to me you did a monthly cash flow analysis and just ignored the balloon payment at the end. Isn’t that the same group-think that created the housing bubble?[/quote]

Even if you use current values for a ~2000 square foot house in Bay Park and compare rent to buy, and assume 6% depreciation, it might still make sense to buy.

See the rent versus buy comparison below. If someone were to hold for 21 years it would make sense to buy, even with the ridiculous assumption of 6% depreciation over 30 years.

The below is a rent/buy comparison based on 6% annual depreciation and 3% annual rent inflation. I plugged in the list price for a remodeled 5BR ~2200 sf house for sale in the upper part of Bay Park that had Bay and Canyon views, and the advertised rent for a 3BR house in the same part of Bay Park (with only a canyon view). So I skewed these in favor of rent.

Assumption was a 4% interest rate. Note that this also includes 0.5% per year in maintenance costs PLUS 0.5% per year in upgrade costs (~$6000 in the first year, indexed for inflation thereafter)..

[img_assist|nid=15799|title=D’Oh!|desc=|link=node|align=left|width=300|height=400]

Well, it’s hard to make your

Well, it’s hard to make your chart large enough for me to read, but a 21-year time frame for breakeven on a rent vs. buy analysis is far beyond the time horizon of most mere mortals. The average first time buyer stays in his home about 5 years before moving on. The second time buyer stays longer, in the range of 11-12 years.

If you say the breakeven is 21 years, the only logical conclusion is to rent.

p.s. The annualized depreciation rate of the San Diego MSA housing stock since the bubble burst in the Fall of 2005 has been 6.5% per year.

creative_cpa wrote:

p.s. The

[quote=creative_cpa]

p.s. The annualized depreciation rate of the San Diego MSA housing stock since the bubble burst in the Fall of 2005 has been 6.5% per year.[/quote]

I guess that means prices will fall 6.5% per year forever (just like the permabulls thought prices would rise 15% annually forever, just because they had been rising 15% annually for a few years leading up to the bubble peak).

Rich Toscano

[quote=Rich Toscano][quote=creative_cpa]

p.s. The annualized depreciation rate of the San Diego MSA housing stock since the bubble burst in the Fall of 2005 has been 6.5% per year.[/quote]

I guess that means prices will fall 6.5% per year forever (just like the permabulls thought prices would rise 15% annually forever, just because they had been rising 15% annually for a few years leading up to the bubble peak).[/quote]

At 6.5% depreciation a year, I can buy a $1M home today at ~$510k in 10 years. If I wait 15 years instead, I can buy that house for $365k. I can’t wait to buy something like this: http://www.sdlookup.com/MLS-110054255-966_Santa_Florencia_Solana_Beach_CA_92075 in 15 years for $365k.

creative_cpa wrote:Well, it’s

[quote=creative_cpa]Well, it’s hard to make your chart large enough for me to read, but a 21-year time frame for breakeven on a rent vs. buy analysis is far beyond the time horizon of most mere mortals. The average first time buyer stays in his home about 5 years before moving on. The second time buyer stays longer, in the range of 11-12 years.

If you say the breakeven is 21 years, the only logical conclusion is to rent.

p.s. The annualized depreciation rate of the San Diego MSA housing stock since the bubble burst in the Fall of 2005 has been 6.5% per year.[/quote]

The fact that the average homeowner moves after 5 years (first time) and 12 years (second time) does not significantly change the outcome in this scenario.

Consider the following:

Person 1 rents for the next 30 years

Person 2

A. buys house #1 and moves after 5 years

B. Buys house #2 and moves afetr an additional 12 years

C. Buys house #3 and is still living there in year 30.

Who is ahead in that scenario, using the same assumptions above ?

creative_cpa wrote:Well, it’s

[quote=creative_cpa]Well, it’s hard to make your chart large enough for me to read, but a 21-year time frame for breakeven on a rent vs. buy analysis is far beyond the time horizon of most mere mortals. The average first time buyer stays in his home about 5 years before moving on. The second time buyer stays longer, in the range of 11-12 years.

If you say the breakeven is 21 years, the only logical conclusion is to rent.

p.s. The annualized depreciation rate of the San Diego MSA housing stock since the bubble burst in the Fall of 2005 has been 6.5% per year.[/quote]

I sense the troll is strong with this one…