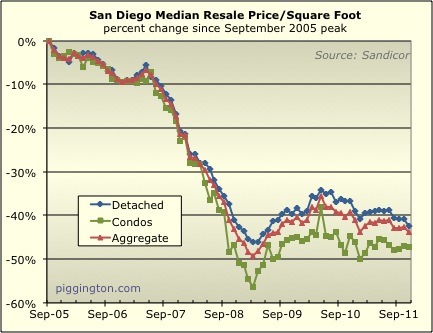

The median price per square foot of San Diego resale homes took a

bit of a hit last month, down 2.5% for single family homes, .3% for

condos, and 1.9% in aggregate. (The single family home price

series is tends to give a more dependable read on the state of

pricing power). On a year-over-year basis, the median price

per square foot was down 8.9% for single family homes, 4.4% for

condos, and 7.5% in aggregate.

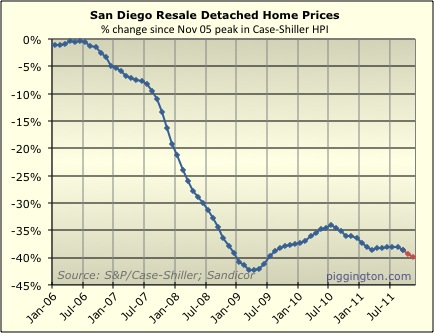

The Case-Shiller proxy, which based on a three-month average of the

detached home median price per square foot, fell by an even

1.0%. That’s down 6.0% from last November. Recall that

the “official” Case-Shiller index hit a new inflation-adjusted

low as of September — it looks like we’ve fallen a couple

percent further since.

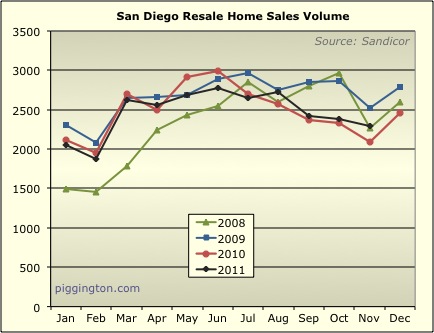

Below are versions of the above graphs gridlined and aligned with

calendar years in order to help elucidate the effects of

seasonality. Clearly, we are in what tends to be the weak

season.

Closed sales dropped by 3.4% for the month, a smaller decline than

we’ve seen in recent Novembers. They were up 10.1% for the

year.

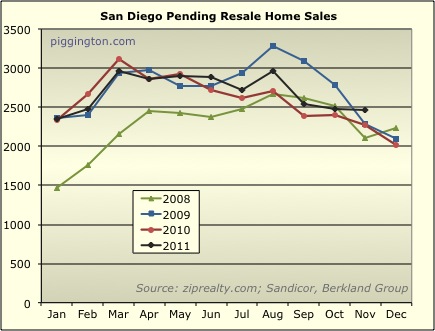

Pending sales fell by a scant .8%, which is also better than the

typical November drop. Pendings were up 8.4% from a year ago.

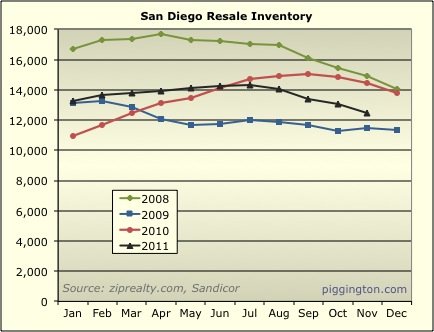

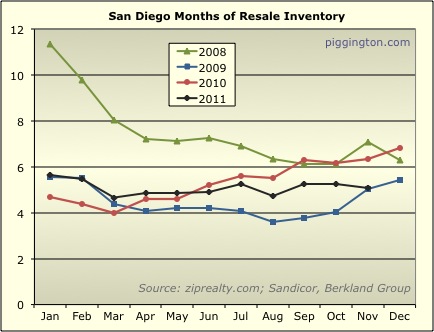

Inventory was down by 4.7% for the month and down 13.6% from a year

ago:

That left 5.1 months of inventory, down 3.9% for the month and 20.3%

from last November.

This is actually a fairly healthy level of inventory, comfortably

below a level at which the market could be considered

“oversupplied.” It’s interesting that prices have been weak in

spite of the reasonable level of supply and the unreasonable lowness

of mortgage rates. We are of course in a time of year in which

prices tend to get pressured lower, all other things being

equal. The market also has a lot of foreclosure inventory and

a fairly anemic economy to contend with.

The negatives have gotten the upper hand lately, but I don’t think a

serious decline is in the works barring a major change in macro

factors such as rates and employment. A slow, unsteady grind

towards lower housing valuation seems to be the more likely outcome

for now.

Could you add a chart that

Could you add a chart that makes housing prices look good?

desmond wrote:Could you add a

[quote=desmond]Could you add a chart that makes housing prices look good?[/quote]

Here you go:

To funny.

To funny.

Take out the 2008 lines and

Take out the 2008 lines and the graphs all look pretty much the same. Looks like 3 years of relative stability to me. Don’t think we are going anywhere anytime soon and are just building another stable base of new owners who had to qualify for their homes properly.

“Looks like 3 years of

“Looks like 3 years of relative stability to me”

Dec 7 2011.

“The sky is clear we can go to lunch”

Dec 7 1941.

desmond wrote:”Looks like 3

[quote=desmond]”Looks like 3 years of relative stability to me”

Dec 7 2011.

“The sky is clear we can go to lunch”

Dec 7 1941.[/quote]

Thats timely and funny but irrlevant. That was a surprise attack and everyone is watching what is happening now. Expect those graphs to look the same for another 3 to 5 years while we add course after course of bricks to our foundation.

“Take out the 2008 lines and

“Take out the 2008 lines and the graphs all look pretty much the same. Looks like 3 years of relative stability to me.”

Why stop there? Take out all the data after 2008 and we can stay in the bubble for ever! 2007 prices will look good again and we can get back to the way things are supposed to be, right?

Guys, sdr’s interpretation is

Guys, sdr’s interpretation is completely legit. The crash phase happened in 08/09, since then the market has just kind of gone nowhere as nominal valuations move sideways, real valuations slowly decline, and the new stock of homeowners is much more financially able to service their debt. What’s so objectionable about what he posted?

Not sure 2.5% decline is

Not sure 2.5% decline is moving sideways. The trend is more down than sideways in my view …and as the above graphs seem to indicate. Home price are still way over-valued in many places, and shouldn’t be confused with affordability based in historically low rates. I do think however, that it is becoming a case of put up or shut up since ‘willingness to pay’ has never been in short supply in Bubblefornia. What is lacking in that innate sense of value for money, which has become an anachronism. You can argue the stability case until you are blue in the face, but for many buyers it remains a deep source of frustration. Arguments that favor ‘what should be’ are still relevant.

Lately the trend is down as

Lately the trend is down as it almost always is seasonally. In Spring it will most likely shift up a bit as it always does and that wont mean the market is improving either.

The arguments that favor what should be absolutely are relevant to what should be. Just not necessarily to what is.

Jazzman wrote:Not sure 2.5%

[quote=Jazzman]Not sure 2.5% decline is moving sideways. The trend is more down than sideways in my view …and as the above graphs seem to indicate. Home price are still way over-valued in many places, and shouldn’t be confused with affordability based in historically low rates. [/quote]

Nominal prices have gone absolutely nowhere for over 2 years. That’s sideways. What happens in a single month in a volatile data series doesn’t impact that conclusion whatsoever.

I don’t know what metric you are using to determine that home prices are overvalued in many places, or what places you are talking about. I do agree that some pockets of SD still seem overvalued. But in aggregate, San Diego homes are actually undervalued based on historical relationships with rents and incomes. (This has nothing to do with interest rates… if you factor in rates, payments are at all time lows compared to rents and incomes).

Rich Toscano wrote:

I don’t

[quote=Rich Toscano]

I don’t know what metric you are using to determine that home prices are overvalued in many places, or what places you are talking about. I do agree that some pockets of SD still seem overvalued. But in aggregate, San Diego homes are actually undervalued based on historical relationships with rents and incomes. (This has nothing to do with interest rates… if you factor in rates, payments are at all time lows compared to rents and incomes).[/quote]

This is why I’m hoping you can update your shambling toward affordability charts *wink* *wink* 😀

AN wrote:

This is why I’m

[quote=AN]

This is why I’m hoping you can update your shambling toward affordability charts *wink* *wink* :-D[/quote]

This weekend, I promise! 😉

For the last year “nominal

For the last year “nominal prices” have been decling and that trend is continuing down, seasonal or non-seasonal. At least that is my interpretation, relevant or not……….

“For the last year “nominal

“For the last year “nominal prices” have been decling and that trend is continuing down, seasonal or non-seasonal.”

I’m seeing the same thing Desmond.

desmond wrote:For the last

[quote=desmond]For the last year “nominal prices” have been decling and that trend is continuing down, seasonal or non-seasonal. At least that is my interpretation, relevant or not……….[/quote]

Jan 09-Jan 10, nominal prices was up. Jan 10-Jan 11, was basically flat. Jan 11-Jan 12, it’s down. So, over the last 3 years, it’s basically flat. Where we’ll be in Jan 13? Who knows. We all can guess, but over the last 3 years, it seems pretty flat to me.

Whatever trend we see out

Whatever trend we see out there is very small. The ec onomic news seems to be getting better including employment. A little good news could bounce things up a couple percent as easily as a little bad news can drop it down a couple percent. Changes this small are just noise in the over all data series. If we go down its not gonna be far. If we go up its not gonna be far either. We are trading in a narrow range and have been for a few years. Some sellers get lucky and get above market prices. Some sellers blow it and get below market prices. Overall we have relative stability. Like it or not.

AN wrote:desmond wrote:For

[quote=AN][quote=desmond]For the last year “nominal prices” have been decling and that trend is continuing down, seasonal or non-seasonal. At least that is my interpretation, relevant or not……….[/quote]

Jan 09-Jan 10, nominal prices was up. Jan 10-Jan 11, was basically flat. Jan 11-Jan 12, it’s down. So, over the last 3 years, it’s basically flat. Where we’ll be in Jan 13? Who knows. We all can guess, but over the last 3 years, it seems pretty flat to me.[/quote]

Am I missing something here. Look at the graph. Whichever line you pick, it went up after the tax credits and went down when they expired. If flat means we are more or less back to where we were. That doesn’t mean RE is flat. It means we are back to where we were. There is a difference. A 1% decline in one month on $1m home is more than most make in a month. If the median went down 2.5% …that is down, not flat. Whichever fancy way you want to tell it, prices are still headed down, which is where they should be headed. Long may it last, since many homes are still over-priced. Period!

Jazzman wrote:Am I missing

[quote=Jazzman]Am I missing something here. Look at the graph. Whichever line you pick, it went up after the tax credits and went down when they expired. If flat means we are more or less back to where we were. That doesn’t mean RE is flat. It means we are back to where we were. There is a difference. A 1% decline in one month on $1m home is more than most make in a month. If the median went down 2.5% …that is down, not flat. Whichever fancy way you want to tell it, prices are still headed down, which is where they should be headed. Long may it last, since many homes are still over-priced. Period![/quote]Why use a $1M house as an example. I can use a $100k condo and say some of us spend more than 1% of that on a TV.

Didn’t I say price have been going down the last year? But I also say price was going up in 2009 and flat in 2010. Didn’t I also say we all can guess where we’re headed to in 2012? But no one knows for sure until it happens. Rich have shown data that many homes are underpriced. Sorry but I trust data over your age. To help you out, here are links to the graphs Rich generated. The chart only goes up to February of this year, which is why I’m hoping Rich will release an update. http://piggington.com/images/dec2010_housing_valuations-7.jpg

http://piggington.com/images/dec2010_housing_valuations-6.jpg

http://piggington.com/images/dec2010_housing_valuations-8.jpg

http://piggington.com/images/dec2010_housing_valuations-5.jpg

desmond wrote:For the last

[quote=desmond]For the last year “nominal prices” have been decling and that trend is continuing down, seasonal or non-seasonal. At least that is my interpretation, relevant or not……….[/quote]

Yes, they were goosed up by the stimulus and since have drifted back down to pre-stimulus levels… this is completely in keeping with my characterization that nominal prices having moved sideways since the crash phase ended in 09.

Rich Toscano wrote:Jazzman

[quote=Rich Toscano][quote=Jazzman]Not sure 2.5% decline is moving sideways. The trend is more down than sideways in my view …and as the above graphs seem to indicate. Home price are still way over-valued in many places, and shouldn’t be confused with affordability based in historically low rates. [/quote]

Nominal prices have gone absolutely nowhere for over 2 years. That’s sideways. What happens in a single month in a volatile data series doesn’t impact that conclusion whatsoever.

I don’t know what metric you are using to determine that home prices are overvalued in many places, or what places you are talking about. I do agree that some pockets of SD still seem overvalued. But in aggregate, San Diego homes are actually undervalued based on historical relationships with rents and incomes. (This has nothing to do with interest rates… if you factor in rates, payments are at all time lows compared to rents and incomes).[/quote]

Absolutely nowhere. I don’t think so. We saw flatness over the selling season and declines thereafter. We are still seeing declines as your graphs very clearly illustrate. A decline is a decline however small it might appear.

Over-valued is an understatement. I don’t need metrics Rich. I have been around long enough to know what is good value and what is not.

Jazzman wrote:Over-valued is

[quote=Jazzman]Over-valued is an understatement. I don’t need metrics Rich. I have been around long enough to know what is good value and what is not.[/quote]

Really? So your age trumps the data?

AN wrote:Jazzman

[quote=AN][quote=Jazzman]Over-valued is an understatement. I don’t need metrics Rich. I have been around long enough to know what is good value and what is not.[/quote]

Really? So your age trumps the data?[/quote]

My age tells me one thing and the date presented in these graphs confirms that. The only bloggers I have a problem with on this issue are usually Realtors. Are you a Realtor?

Jazzman wrote:My age tells me

[quote=Jazzman]My age tells me one thing and the date presented in these graphs confirms that. The only bloggers I have a problem with on this issue are usually Realtors. Are you a Realtor?[/quote]

No I’m not. AFAIK, neither is Rich. So, if I find someone who’s older than you, thinks you’re wrong, and think these charts agree with him/her, then you’re wrong?

Jazzman wrote:AN

[quote=Jazzman][quote=AN][quote=Jazzman]Over-valued is an understatement. I don’t need metrics Rich. I have been around long enough to know what is good value and what is not.[/quote]

Really? So your age trumps the data?[/quote]

My age tells me one thing and the date presented in these graphs confirms that. The only bloggers I have a problem with on this issue are usually Realtors. Are you a Realtor?[/quote]

Let me sum up your entire argument:

1. Data doesn’t matter.

2. Anyone who disagrees with you must be a realtor.

Again, substitute the word “renter” for “realtor” in #2, and you have precisely summarized the thesis that the real estate bulls used at the height of the bubble.

Jazzman wrote:I don’t need

[quote=Jazzman]I don’t need metrics Rich. I have been around long enough to know what is good value and what is not.[/quote]

This exact comment could have been plucked directly from the keyboard of a 2005-era permabull… ignore the data at your own risk.

Rich Toscano wrote:Guys,

[quote=Rich Toscano]Guys, sdr’s interpretation is completely legit. The crash phase happened in 08/09, since then the market has just kind of gone nowhere as nominal valuations move sideways, real valuations slowly decline, and the new stock of homeowners is much more financially able to service their debt. What’s so objectionable about what he posted?[/quote]

Instead of ignoring the crash and saying “looks like 3 years of realative stability” you could also say “despite massive government efforts and record low interest rates the delcine has stalled but shadow inventories remain high and prices show no signs of increasing any time soon.”

There are different ways to frame a situation to change the view, but I guess we all have our biases to confirm.

ShawnHCRW wrote:

Instead of

[quote=ShawnHCRW]

Instead of ignoring the crash and saying “looks like 3 years of realative stability” you could also say “despite massive government efforts and record low interest rates the delcine has stalled but shadow inventories remain high and prices show no signs of increasing any time soon.”

There are different ways to frame a situation to change the view, but I guess we all have our biases to confirm.[/quote]

Yes, and I have said exactly that… it doesn’t make the first interpretation wrong. They are both true and are both an important part of figuring out what’s going on. I just don’t see why describing what’s happened without overlaying a predictive bearish (or bullish for that matter) narrative is so objectionable.

ShawnHCRW wrote:”Take out the

[quote=ShawnHCRW]”Take out the 2008 lines and the graphs all look pretty much the same. Looks like 3 years of relative stability to me.”

Why stop there? Take out all the data after 2008 and we can stay in the bubble for ever! 2007 prices will look good again and we can get back to the way things are supposed to be, right?[/quote]

If you take the first graph, and draw a horizontal line level with the last data point in the aggregate line, the earliest point at which it intercepts aggregate line is about Oct 2008, or 3 years ago.

How is that not 3 years of relative stability ?

sdduuuude wrote:

If you take

[quote=sdduuuude]

If you take the first graph, and draw a horizontal line level with the last data point in the aggregate line, the earliest point at which it intercepts aggregate line is about Oct 2008, or 3 years ago.

How is that not 3 years of relative stability ?[/quote]

REALTOR

Of course, ~3 years of

Of course, ~3 years of relatively flat nominal prices means prices have fallen relative to inflation. Probably something like 4-5%, depending how you like to calculate “real” inflation.

It will be interesting to see if months of inventory moves much in December/January. I know a lot of potential sellers take their homes off the market over the Holidays due to not wanting to show them during December. There could be a big difference in 2012’s market if we see 4 months vs. 6 months of Resale Inventory in January 2012, and either seems feasible right now.

There is alot of effort

There is alot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months.

jazzman and desmond

Both you

jazzman and desmond

Both you seem utterly convinced you know what is coming. I’ve got an open mind and will listen to reasonable argument. So how much do nominal prices have to fall?

desmond wrote:There is alot

[quote=desmond]There is alot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months.[/quote]

I don’t find it a lot of effort to look at a chart and note the fact that prices have gone nowhere for two years. I guess I must be a coffee achiever.

My statement was that the market had gone sideways since the crash phase ended in 09. This is an indisputable fact based on what has actually happened, not a prediction about what may happen in the future. Don’t make more of the statement than what it was.

From the chart on the

From the chart on the previous post by Rich, adjusted for inflation, prices are somewhere near the peak of the last cycle…why doesn’t that make valuations suspect?

Jacarandoso wrote:From the

[quote=Jacarandoso]From the chart on the previous post by Rich, adjusted for inflation, prices are somewhere near the peak of the last cycle…why doesn’t that make valuations suspect?[/quote]

Good question… the answer is that home prices track better to rents and incomes than inflation, and rents/incomes have risen faster than inflation.

Jacarandoso wrote:From the

[quote=Jacarandoso]From the chart on the previous post by Rich, adjusted for inflation, prices are somewhere near the peak of the last cycle…why doesn’t that make valuations suspect?[/quote]

Valuations is not pure nominal price for most buyers. Valuation is price & interest for most buyers. To those who pay cash, yes, valuation is quite high compare to the past. However, majority of the buyers out there do not pay cash for their house. So interest rate plays as big of a role as the nominal price itself. At the peak of the last cycle, IIRC, interest rate was in the low teens. Rich’s charts in “Shambling toward affordability” shows this very clearly. Also as Rich said, you have to compare it against nominal rent & income as well.

AN wrote:Jacarandoso

[quote=AN][quote=Jacarandoso]From the chart on the previous post by Rich, adjusted for inflation, prices are somewhere near the peak of the last cycle…why doesn’t that make valuations suspect?[/quote]

Valuations is not pure nominal price for most buyers. Valuation is price & interest for most buyers. To those who pay cash, yes, valuation is quite high compare to the past. However, majority of the buyers out there do not pay cash for their house. So interest rate plays as big of a role as the nominal price itself. At the peak of the last cycle, IIRC, interest rate was in the low teens. Rich’s charts in “Shambling toward affordability” shows this very clearly. Also as Rich said, you have to compare it against nominal rent & income as well.[/quote]

Price has just become a number against which you calculate your monthly nut. It has been detaching itself from intrinsic value in recent years with remarkable alacrity. Affordability needs to be seen in the context of unintended consequences. Have you really preserved equity gains, or just made homes unaffordable for the next wave of home buyers?

Jazzman wrote:It has been

[quote=Jazzman]It has been detaching itself from intrinsic value in recent years with remarkable alacrity. [/quote]

I just think these kinds of statements are meaningless if you are unwilling to provide data to back them up.

These statistical reports on

These statistical reports on affordability, and even price indices for that matter are useful but more in an academic sense. However, they do play on consumer sentiments and we are seeing a game being played here.

The practicalities of buying a home are quite a different matter. Just read a dozen home inspection reports before you dip your toes. They are designed to inject reality into the home buying process, and they do. Your monthly nut is just the start, and a common mistake is to buy the maximum you can afford later to realize your costs curve is somewhat steeper. I am seeing deferred maintenance on a big scale in this market, as home owners can’t get a loan to rehab, remodel, or even do a few basic maintenance updates. Prices in general are not reflecting these issues enough. So buying what you think you can afford can come with a bag of regrets.

There is no statistical imperative for the practicalities of home ownership. The more secure basis for home ownership is value. It will allow you to refinance, and be a less volatile store of wealth. Prices should therefore be allowed to fall, and declines should be met with encouragement not derision. While home price deflation has been the enemy of the industry due to the downward spiral it creates, I believe we are past that point and now is a great opportunity to let housing come back down to earth.

Jazzman wrote:

There is no

[quote=Jazzman]

There is no statistical imperative for the practicalities of home ownership. The more secure basis for home ownership is value.[/quote]

And how do you determine value without numbers?

Rich Toscano wrote:Jazzman

[quote=Rich Toscano][quote=Jazzman]

There is no statistical imperative for the practicalities of home ownership. The more secure basis for home ownership is value.[/quote]

And how do you determine value without numbers?[/quote]

Rich, it is innate. There weren’t always numbers around to qualify worth. Everyone has their own sense of value, but it is an intuition that is fast being eroded. When you hear someone declare “that is outrageous”, or, “I’m not paying that”, they are expressing their preconceived sense of value. I am not dumbing down stats as they have a very important role, but when they run up against emotional responses such as the above, you need to ask which master do they serve?

Jazzman wrote:Rich, it is

[quote=Jazzman]Rich, it is innate. There weren’t always numbers around to qualify worth. Everyone has their own sense of value, but it is an intuition that is fast being eroded. When you hear someone declare “that is outrageous”, or, “I’m not paying that”, they are expressing their preconceived sense of value. I am not dumbing down stats as they have a very important role, but when they run up against emotional responses such as the above, you need to ask which master do they serve?[/quote]

I could have sworn that was what the permabulls were saying in 2005 when some of us were trying to explain the bubble with data.

BTW, Jazzman, your

BTW, Jazzman, your insinuations about “playing games,” about price declines being met with derision, etc, are quite misplaced.

You are a latecomer to this site, so perhaps you don’t know that I started it in 2004 to document (via data and statistics, which is the proper way to prove a thesis) that homes were stunningly overpriced. For the entire time, I have argued strenuously that overpriced homes are harmful to society, and that the best thing that could happen would be to allow them to become affordable again. I constantly ranted against the bailouts of the banks and real estate industries.

Over this site’s life, I have taken a huge amount of heat — first from permabulls who thought prices could never go down, and then from permabears who thought they would never stop going down. All along, I’ve strived to look dispassionately at the data and to figure out what’s really going on. My analysis may be wrong at times, but it has never been and will never be driven by an agenda.

So please check your ad hominems at the door. My objection to your posts in this thread aren’t based on my having some sort of bias or agenda; they are based on the fact that you have made sweeping statements that are utterly unsupported by the empirical data that I have provided, and that you refuse to provide any data of your own.

Rich

PS – The data I am primarily referring to can be found here (update to come this weekend): http://piggington.com/shambling_towards_affordability_yearend_2010_edition

Jazzman wrote:Price has just

[quote=Jazzman]Price has just become a number against which you calculate your monthly nut. It has been detaching itself from intrinsic value in recent years with remarkable alacrity. Affordability needs to be seen in the context of unintended consequences. Have you really preserved equity gains, or just made homes unaffordable for the next wave of home buyers?[/quote]

Do you have data to back this up? Rich have collected data and generated graphs. Both Rich and I have pointed you to them. DATA have shown that affordability is at an all time high in recent past. Example would be, buyers today pay less per month than buyers just 3 years ago, even when price have been flat. So, where’s your data that show that next wave of home buyers are facing lower affordability level?

AN wrote:Jacarandoso

[quote=AN][quote=Jacarandoso]From the chart on the previous post by Rich, adjusted for inflation, prices are somewhere near the peak of the last cycle…why doesn’t that make valuations suspect?[/quote]

Valuations is not pure nominal price for most buyers. Valuation is price & interest for most buyers. To those who pay cash, yes, valuation is quite high compare to the past. However, majority of the buyers out there do not pay cash for their house. So interest rate plays as big of a role as the nominal price itself. At the peak of the last cycle, IIRC, interest rate was in the low teens. Rich’s charts in “Shambling toward affordability” shows this very clearly. Also as Rich said, you have to compare it against nominal rent & income as well.[/quote]

By your own measure of “monthly nut”, if I understand you, homes are overvalued? Rates should go nowhere but up. If it happens soon, today’s prices will be high in retrospect because the monthly nut for the average buyer will be higher. Yes, I know there is not always a direct correlation, it seems like what you are saying though.

Whether or not other factors weigh against rent/income is hard to discern. I have some thoughts on that but don’t want to go into it right now. But I will ask a question; If houses are extremely affordable and have been for some time now(by any metric), why aren’t prices going up?

Jacarandoso wrote:By your own

[quote=Jacarandoso]By your own measure of “monthly nut”, if I understand you, homes are overvalued? Rates should go nowhere but up. If it happens soon, today’s prices will be high in retrospect because the monthly nut for the average buyer will be higher. Yes, I know there is not always a direct correlation, it seems like what you are saying though.

Whether or not other factors weigh against rent/income is hard to discern. I have some thoughts on that but don’t want to go into it right now. But I will ask a question; If houses are extremely affordable and have been for some time now(by any metric), why aren’t prices going up?[/quote]

Homes are not overvalued. On average, homes in SD are under valued. Here are the data Rich and I point to a few times on this thread: http://piggington.com/shambling_towards_affordability_yearend_2010_edition. If you lock in to a 30 years rate, rising rate doesn’t affect you (in term of rates). As you just said, there’s not always a direct correlation between rising rates and falling price. I would go further and say, I don’t think there is much data showing any correlation, AFAIK. So, decreasing affordability, in my eyes would be brought about by improvement in economic condition.

As to your why aren’t prices going up question, it would be same explanation as to why price keep on going up in 2002-2006 while houses are extremely un-affordable for some time. If affordability drive the market, then we wouldn’t have seen this past bubble. It comes down to simple greed and fear (two faces of the same coin IMHO).

To echo An it all comes down

To echo An it all comes down to pyschology. There are lots of potential buyers out there (including the more bearish posters on this site) that are fully qualified and able to afford a home but are fearful of prices dropping dramatically. The economic news coming out is mostly negative. The supply is constricted and it is difficult to buy a home because of lender involvement (approval for short sale or REO). Those factors overwhelm the affordability issue.

On a related note, I have a family member looking for a starter home. Everything priced under $350K that is decent, in good area and within range of the comps has multiple offers within a week or so. Entry level buyers are fighting to find a decent home while prices and rates are low. Its a bit crazy out there in that segment.

sdrealtor wrote:To echo An it

[quote=sdrealtor]To echo An it all comes down to pyschology. There are lots of potential buyers out there (including the more bearish posters on this site) that are fully qualified and able to afford a home but are fearful of prices dropping dramatically. The economic news coming out is mostly negative. The supply is constricted and it is difficult to buy a home because of lender involvement (approval for short sale or REO). Those factors overwhelm the affordability issue.

On a related note, I have a family member looking for a starter home. Everything priced under $350K that is decent, in good area and within range of the comps has multiple offers within a week or so. Entry level buyers are fighting to find a decent home while prices and rates are low. Its a bit crazy out there in that segment.[/quote]

Could be a lot of psychological/mental factors at play beyond fear. People’s perceptions of what is affordable can change downward, and that can be positive for them. In the real world there is a huge discretionary input into housing expenditures. Maybe optional outlays in other directions become a priority to many. I hope there is a general trend like that. The “negatives”, IMO, should encourage it at least for the time being.

I understand what Rich is saying about needing some statistical derivation of “affordability”, but pragmatically it is something that has to be decided at least a few years forward, looking in the rear view mirror. Under the current situation it would not be that far of a stretch to be hopeful of that outcome being positive, but it can also come across as cheerleading, given the negatives we all know about. Maybe that is what Jazzman is trying to get at?

(Not in the slightest accusing you of “cheerleading”, Rich)

Jacarandoso wrote:sdrealtor

[quote=Jacarandoso][quote=sdrealtor]To echo An it all comes down to pyschology. There are lots of potential buyers out there (including the more bearish posters on this site) that are fully qualified and able to afford a home but are fearful of prices dropping dramatically. The economic news coming out is mostly negative. The supply is constricted and it is difficult to buy a home because of lender involvement (approval for short sale or REO). Those factors overwhelm the affordability issue.

On a related note, I have a family member looking for a starter home. Everything priced under $350K that is decent, in good area and within range of the comps has multiple offers within a week or so. Entry level buyers are fighting to find a decent home while prices and rates are low. Its a bit crazy out there in that segment.[/quote]

Could be a lot of psychological/mental factors at play beyond fear. People’s perceptions of what is affordable can change downward, and that can be positive for them. In the real world there is a huge discretionary input into housing expenditures. Maybe optional outlays in other directions become a priority to many. I hope there is a general trend like that. The “negatives”, IMO, should encourage it at least for the time being.

I understand what Rich is saying about needing some statistical derivation of “affordability”, but pragmatically it is something that has to be decided at least a few years forward, looking in the rear view mirror. Under the current situation it would not be that far of a stretch to be hopeful of that outcome being positive, but it can also come across as cheerleading, given the negatives we all know about. Maybe that is what Jazzman is trying to get at?

(Not in the slightest accusing you of “cheerleading”, Rich)[/quote]

Age probably has something to do with it. Putting things into historical context makes you view things differently. Look at any home that sold +15 years ago, and it will focus the mind wonderfully. For some of us that is not a long time ago, but for others it is as distant, as it is unfamiliar. What I find puzzling is that even recent history is screaming at us, yet we are too eager to forget. Just look at the peak on those graphs. Had the government and federal reserve not applied the brakes when they did, home prices would have continued on their then trajectory. Is the simplest of terms, home prices didn’t correct fully. The fact that rates which are being held down makes them “affordable” is bit like apologizing to an amputee for cutting off his good leg, while praising the merits of prosthetic limbs.

sdrealtor wrote:On a related

[quote=sdrealtor]On a related note, I have a family member looking for a starter home. Everything priced under $350K that is decent, in good area and within range of the comps has multiple offers within a week or so. Entry level buyers are fighting to find a decent home while prices and rates are low. Its a bit crazy out there in that segment.[/quote]

I have noticed just as a hobbyist that top properties continue to be snapped up same-day, especially coastal. There have been a couple recent gems in Encinitas and Solana Beach that have gone above asking price w/i 48 hours.

It’s funny because when I bought my first house in 1998 it was entry-level and the price was $150k… now entry-level is $350k. I remember seeing $450k houses at the time and thinking “Who the hell has $450k?!?!?!?”

Now we’re building a house (SLOWLY… two kids does that) and the total bill will come to $900k or so… but for the neighborhood that’s a “steal”.

Kinda mind-blowing, and I suspect that’s what people like Jazzman get hung up on. But compounding numbers do funny things vs. the human brain. I always compare the linear to logarithmic graphs of the S&P 500 index to reset my brain… one screams bubble and the other screams boring as hell.

desmond wrote:There is alot

[quote=desmond]There is alot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months.[/quote]

Realtors say flat, buyers say down. We know the efforts are aimed at arresting home price deflation. At least the government has been honest enough to admit it.

At least with a few posters

At least with a few posters that have different opinions the post count got over 40 compared to the last 10 or so topic lovefests that probably average a mean nominal chart breaking total real value of 5.

So to play the what if game.

So to play the what if game. Schiff is saying higher interest rates are a comin and I think Roubini is saying the same thing.

The San Diego housing market

The San Diego housing market trend is both sideways over 2 years and down on an annualized basis.

I personally wouldn’t use “sideways over 2 years” to describe the market, as the first six months or so of those 2 years contained massive intervention. Yes, the intervention continues. However, when much of the intervention expired the overall market changed course for the worse.

My opinion is that describing the market as down on an annualized basis is currently the most accurate way to describe the market as a whole. I’d love to see post-massive-intervention annualized price gains. But I’m not holding my breath.