It’s time for the monthly housing data roundup…

Prices

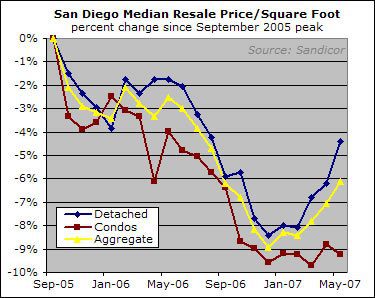

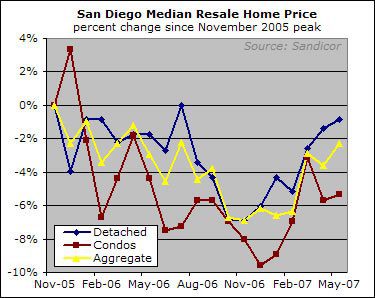

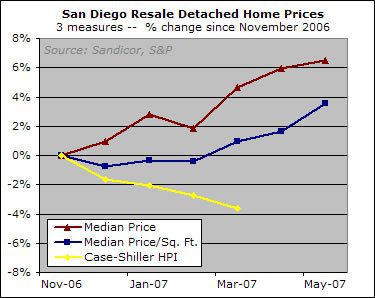

To hear the median-based price indicators tell it, condo prices have stabilized and single-family prices are on a tear:

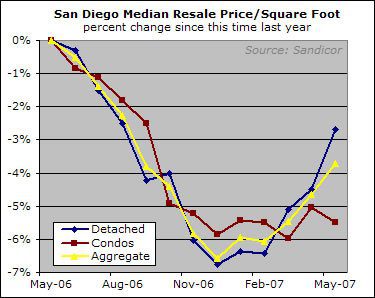

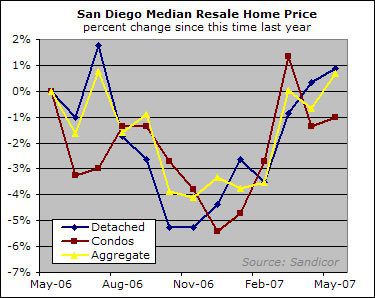

The above charts start from the respective data series’ peaks… here’s a look at the year-over-year change:

The problem is these indicators seem to have become nigh-useless in the wake of the subprime tightening that started at the end of 2006. The decline in low-end activity, as I’ve beaten to death in recent weeks, has caused the median transaction price to rise even as the market price of a given home has fallen (those who are just joining us can find a longer explanation here). These same factors have confused things further by causing a bifurcation of price strength, wherein high-end housing is apparently doing pretty well while lower-end properties are getting more whacked.

Anyway, witness the divergence between the more-accurate Case-Shiller HPI (which is based on same-home sales) and the median-based indicators since the subprime debacle began late last year:

Unfortunately, there is a long delay before the HPI is made available. It could well be that the price strength apparent in the median indicators is at least partially real, and that the HPI will end up ticking up during April and May. Price strength is after all to be expected at this time of year. However, the November-March divergence between the median indicators and the HPI renders the former highly suspect unless and until they can get back into line with the HPI again at some point.

So why bother with them? For one thing, since the rest of the world focuses so much attention on the median price, it’s instructive to see what they are seeing. Also, the median-based indicators are lame but they are the only post-March info available. But possibly the biggest reason is that I already had the charts done, so what the hell.

Anyway, will the strength in the median price cause yet another bout of bottom-calling? Probably. The bullishness has been subdued lately because even the strong median price movements in the resale market have been offset by big median declines in the market for new homes. Nonetheless, I imagine that a few pundits will take the opportunity to declare a new bull market yet again. (On a related note, the highly entertaining "Bubble Markets Inventory Tracking" blog recently profiled one of San Diego’s many serial bottom-callers).

It’s unfortunate that the only remaining utility of the formerly useful size-adjusted median and the formerly less-useful-but-still-not-entirely-useless plain vanilla median is to serve as objects for bullish spinmeistering. Fortunately, many RE professionals and "civilians" in the Econo-Almanac forums are constantly providing interesting anecdotal data that we can enjoy while we wait for the next HPI print.

Supply and Demand

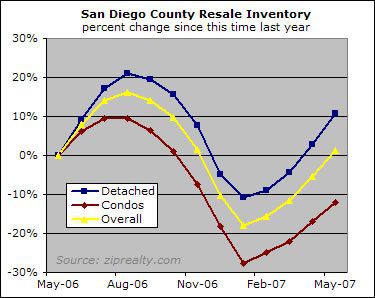

As of mid-May, inventory was about even with its year-ago levels:

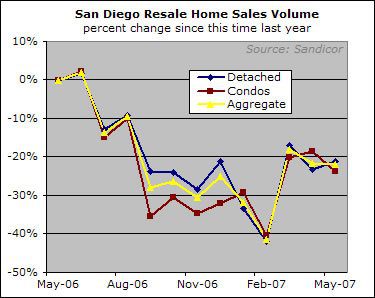

But sales are down over 20% from their already-dismal 2006 levels:

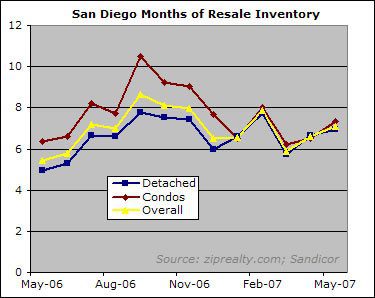

Resulting in a months-of-inventory figure of about 7, which is noticably worse than this time last year:

In 2003-2004, a speculative, short-term run on for-sale inventory was interpreted by almost all local real estate pundits (and non-pundits) as being indicative of a structural crisis-level shortage in San Diego housing supply. Yet now that 7 months of resale inventory is languishing on the market, for-sale inventory is no longer the go-to measure for overall housing supply. Isn’t that interesting?

The overall rise in months inventory sure isn’t going to help prices, but I think it is actually less important than the fact that more of the inventory is of the must-sell variety. As of April, the number of monthly defaults and foreclosure sales (rough proxies for the amount of must-sell inventory) were both greatly increased from their year-ago levels:

Conclusion

Let’s wait and see if that spring bounce is for real. Of course, even if it is, that doesn’t change the fact that we are obviously mired in a long-term housing downturn. The rate of suicide loan resets hasn’t even peaked, and people who are resetting face tighter standards and higher yields (both adjustable and fixed-rate–note the bond market spankage of late). The resulting must-sell inventory overhang is greeted by continually weakening demand as financing options dry up and more and more people punch in to the fact that San Diego housing is vastly overpriced and, for now, anyway, a terrible investment.

The fantasy of paying for a home using only your future equity gains has come to an end. While it’s going to take a long time, home prices and their fundamentals will eventually meet once again.

Chicago mercantile exchange

Chicago mercantile exchange futures for San Diego May 08

last traded at 222.8 – http://www.cme.com –

I don’t have the March 07 figure to hand but it’s 230 something.

So if anybody really believes in the bottom they can put their money where their mouth is trading an index which seems to understate the “price recovery.”

Keep up the good work, Rick!

R.

Very nice update,

Very nice update, Rich.

Funny, how the change in mix (less low-end, relatively more high-end) affects even the size-adjusted calculations; I would not have guessed that that would be the case. When I squint, I see a good correlation between the raw median and size-adjusted median graphs.

I know that ‘median price for resale homes’ is flawed. But, for me, it alone is sufficient when it is caveated with the statement, ‘Remember that there is a change in mix, and that such will resolve itself in the data series in coming months.’

Keep up the good work, sir.

Now, back to politics and religion…

I agree that this is a

I agree that this is a fantastic update. We are privleged to have access to it.

“Funny, how the change in mix (less low-end, relatively more high-end) affects even the size-adjusted calculations;”

My take is that these more qualified “high end buyers” are buying more expensive land(location,views ect.) and higher quality construction and finishings or some hybrid of all three.If this is true it explains the price per square foot almost tracing the basic median trend.