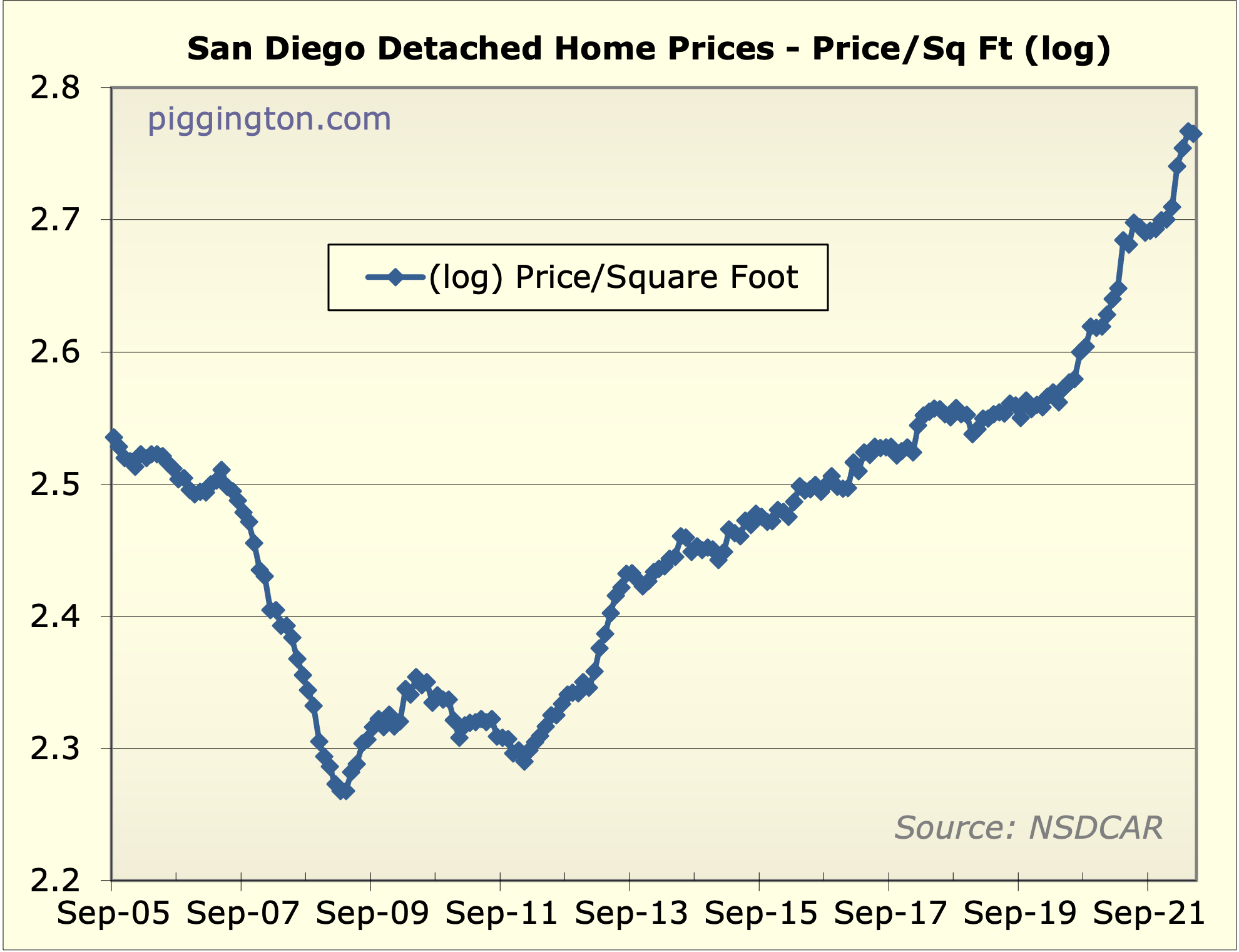

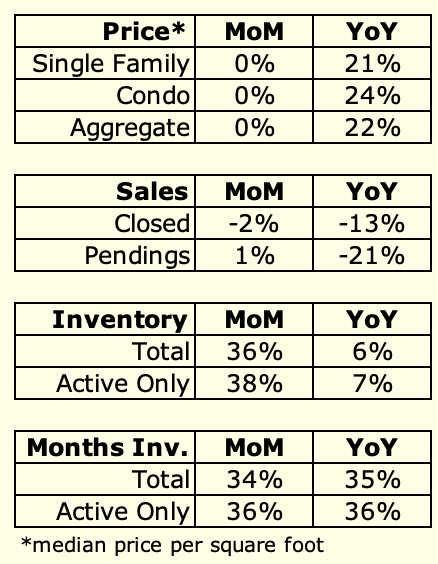

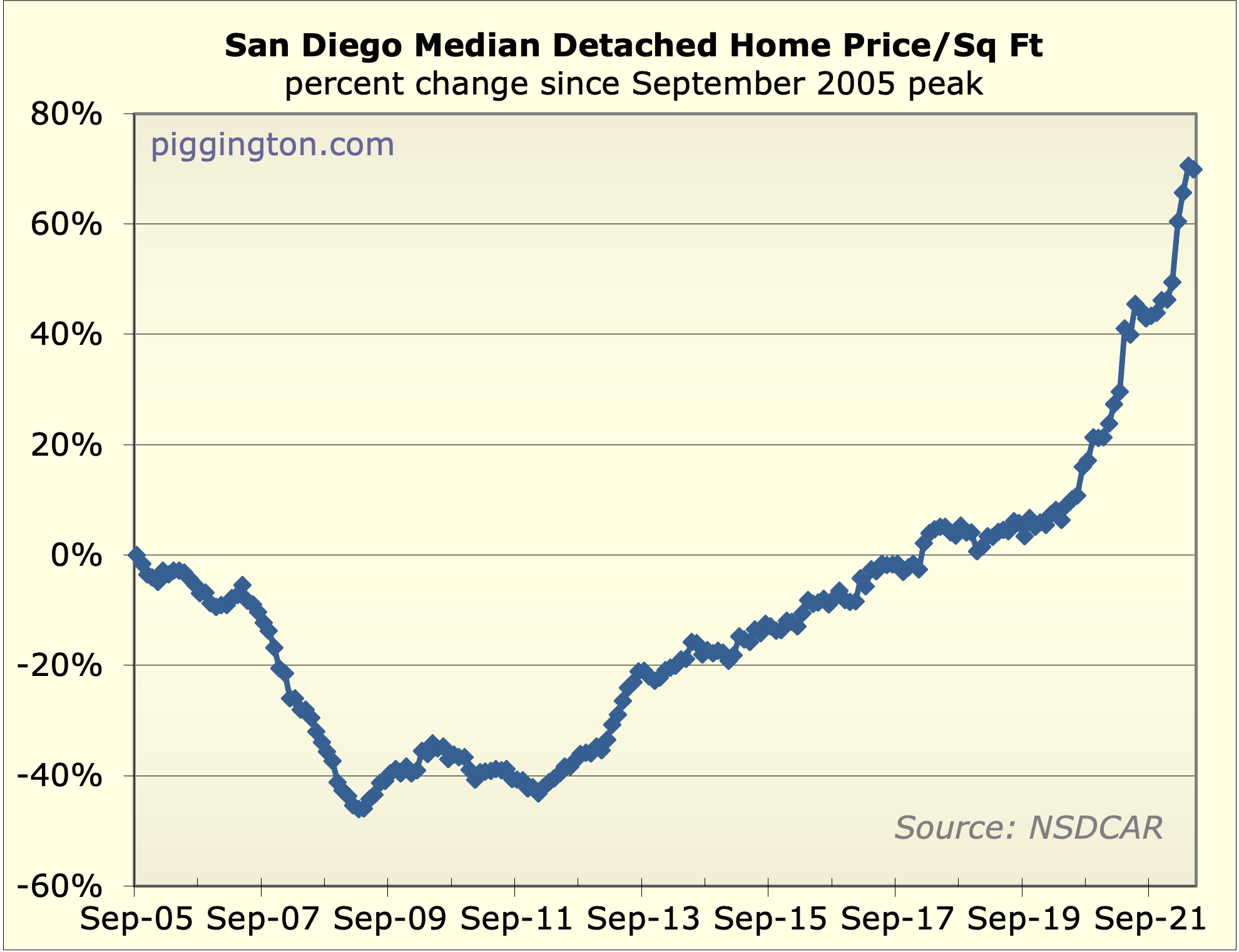

Prices were down a (very) wee bit last month:

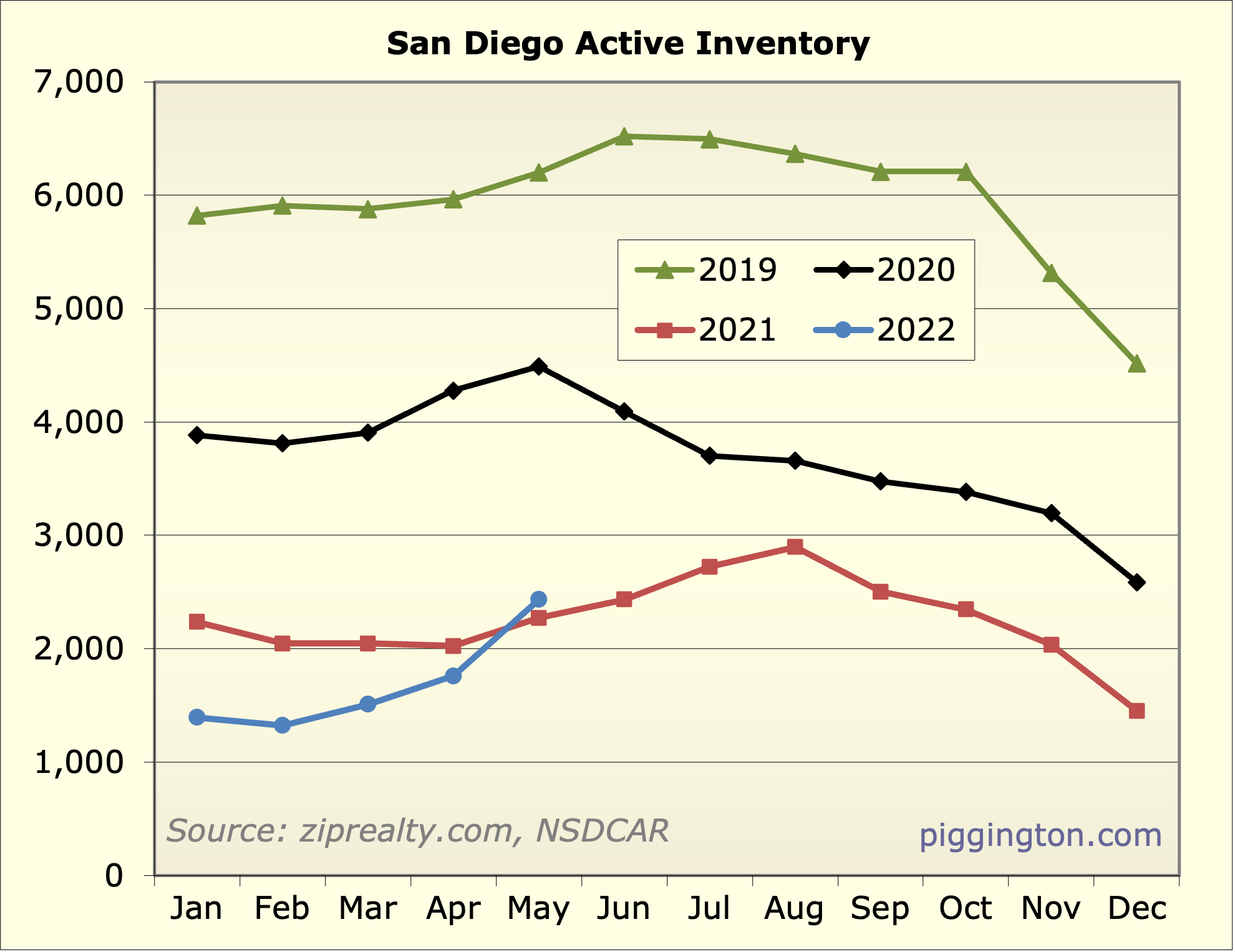

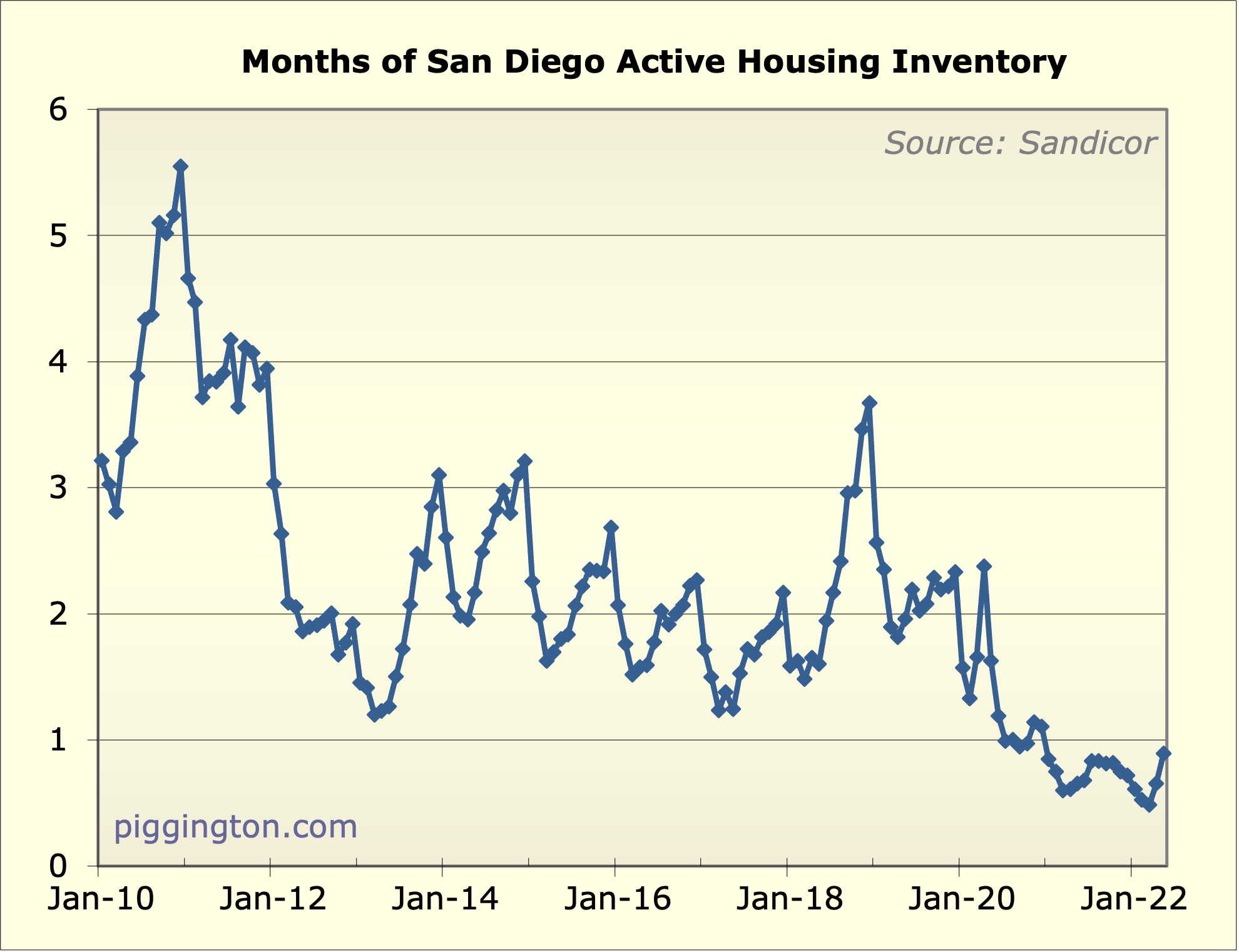

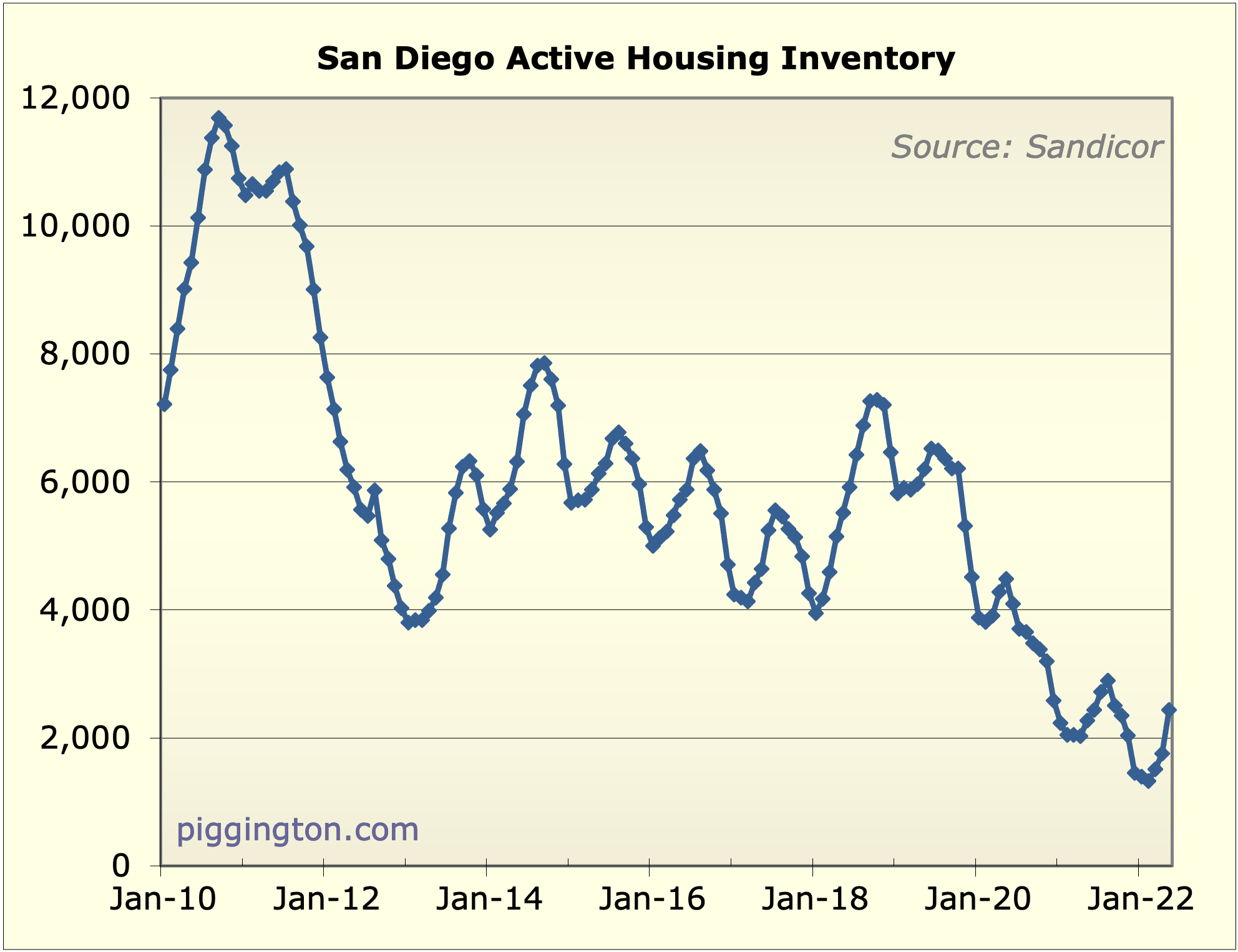

Inventory started to build:

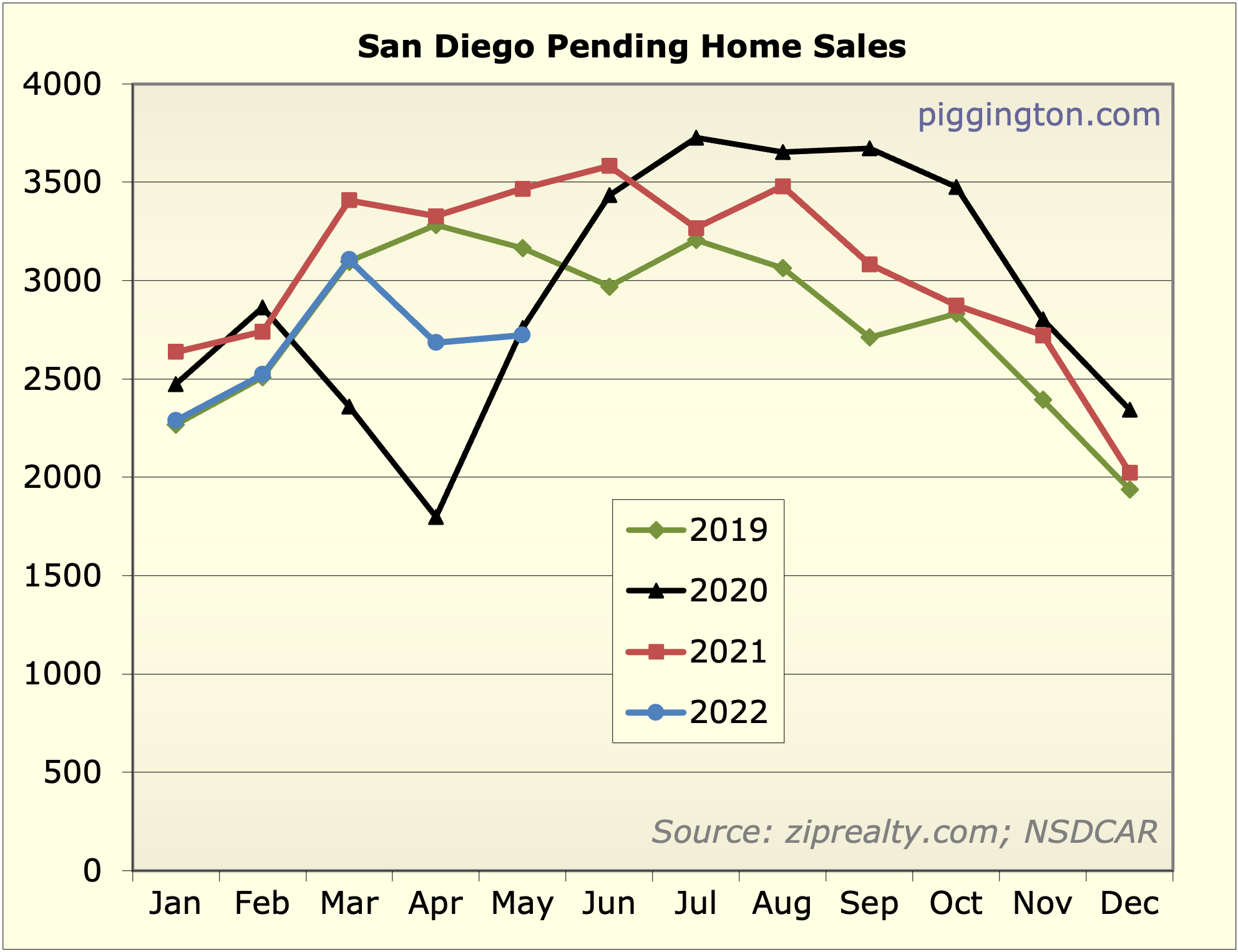

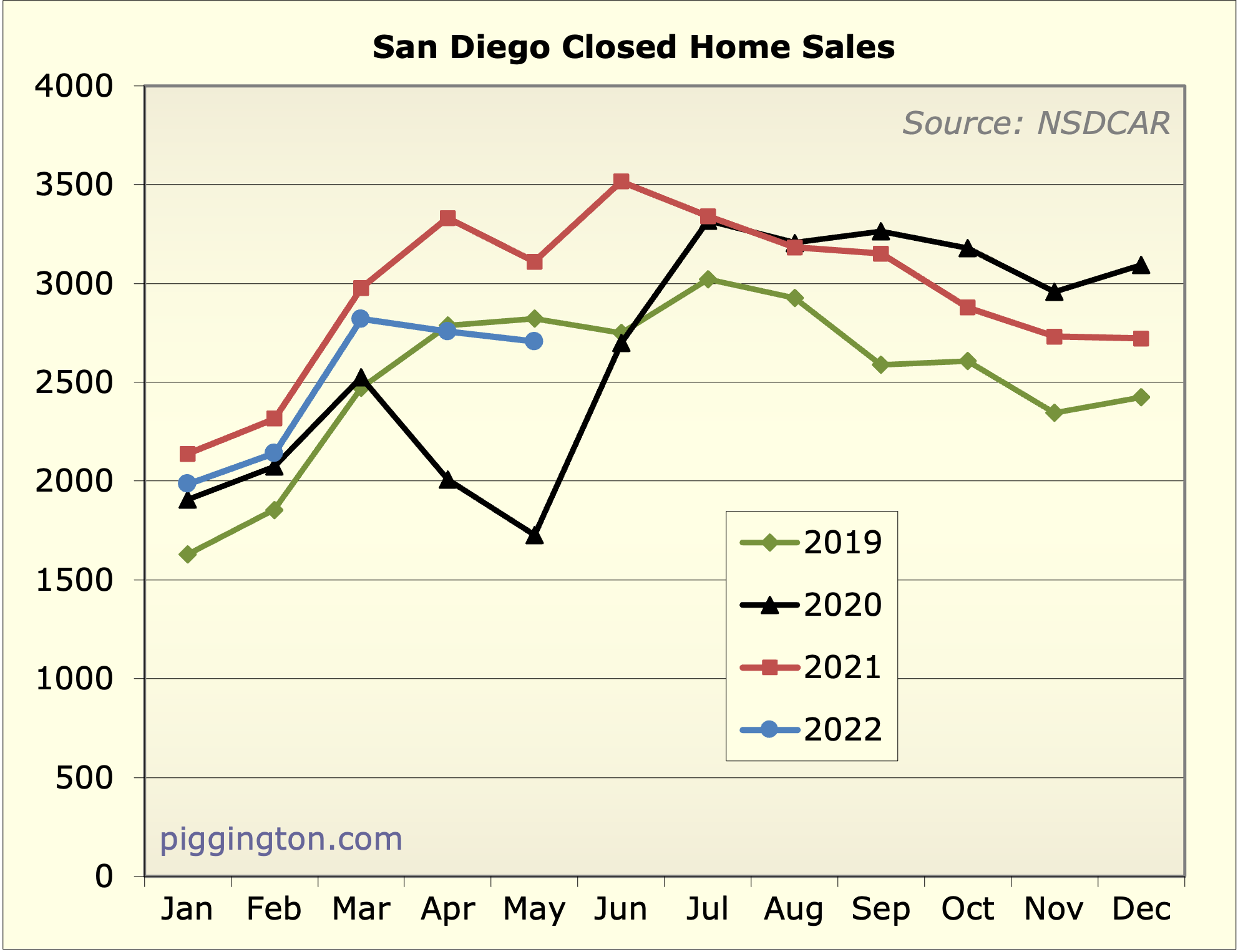

Pending sales hung in there from the prior month, but are still

lower than a couple months ago. It’s probably the case that many

people going pending last month still had lower rates locked in.

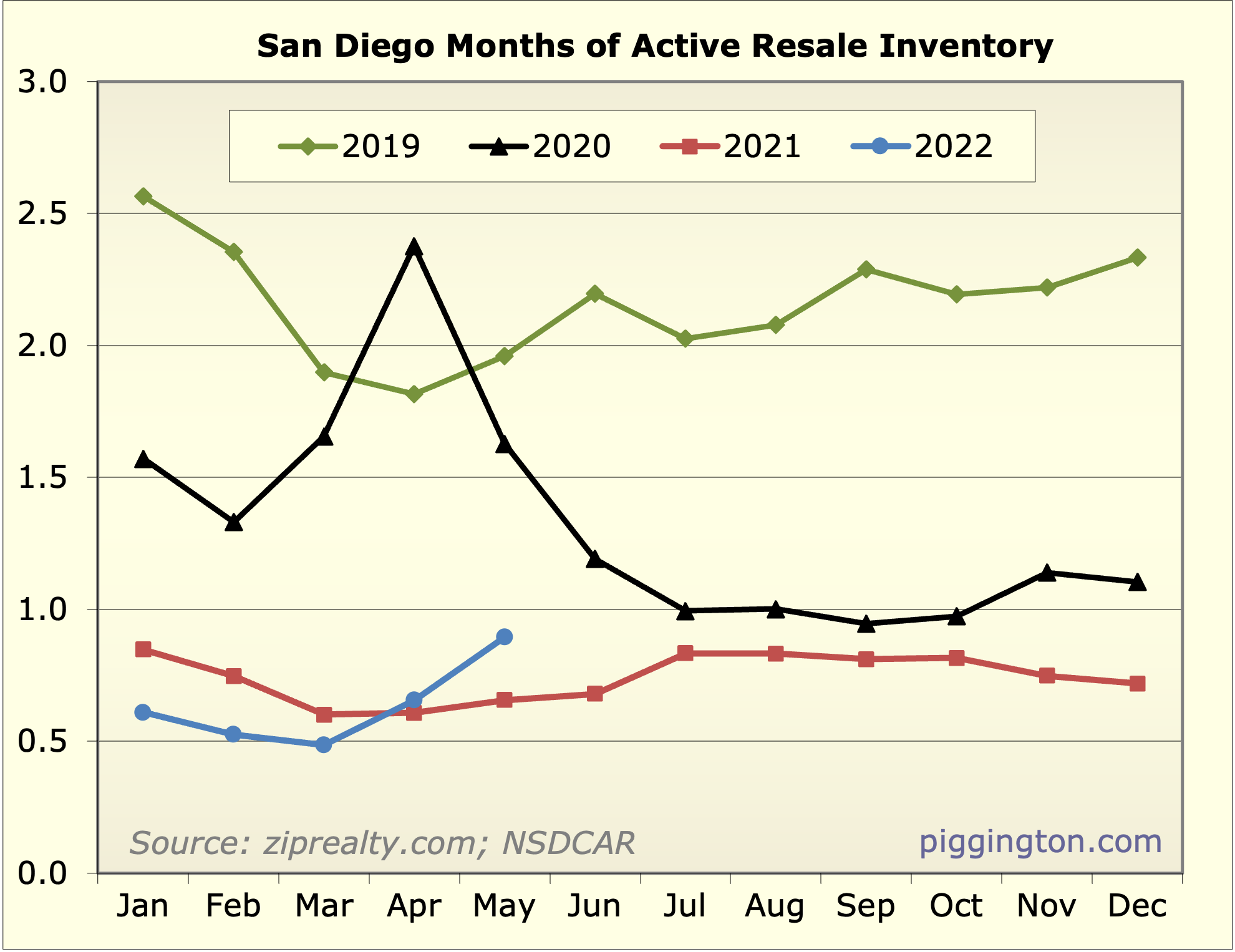

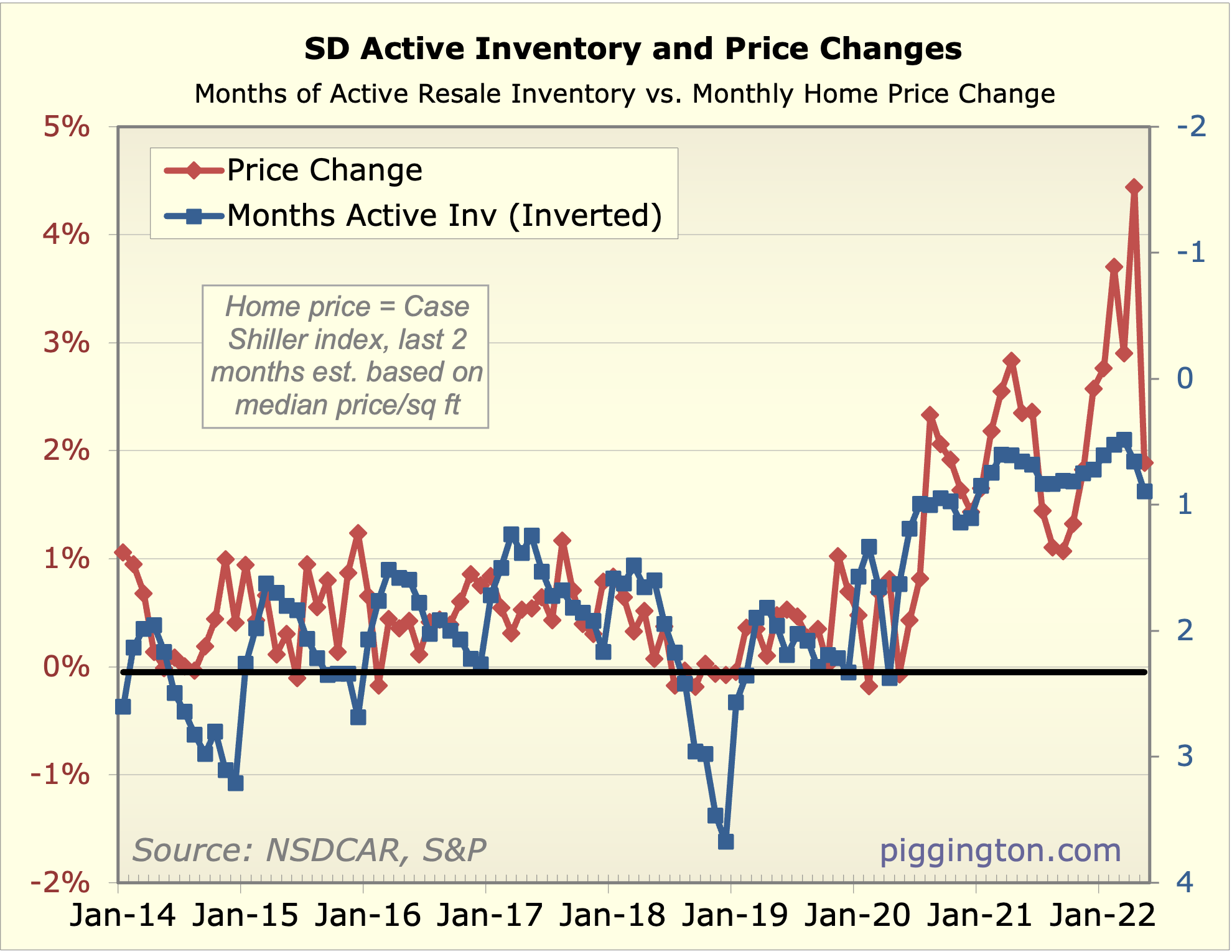

Putting them together, months of inventory rose quite a lot in

percent terms, but that’s coming off a very low base.

This longer-term chart of months of inventory puts the increase in

perspective:

So we’re still at very low inventory levels that have historically

implied higher near-term prices. I continue to question whether that

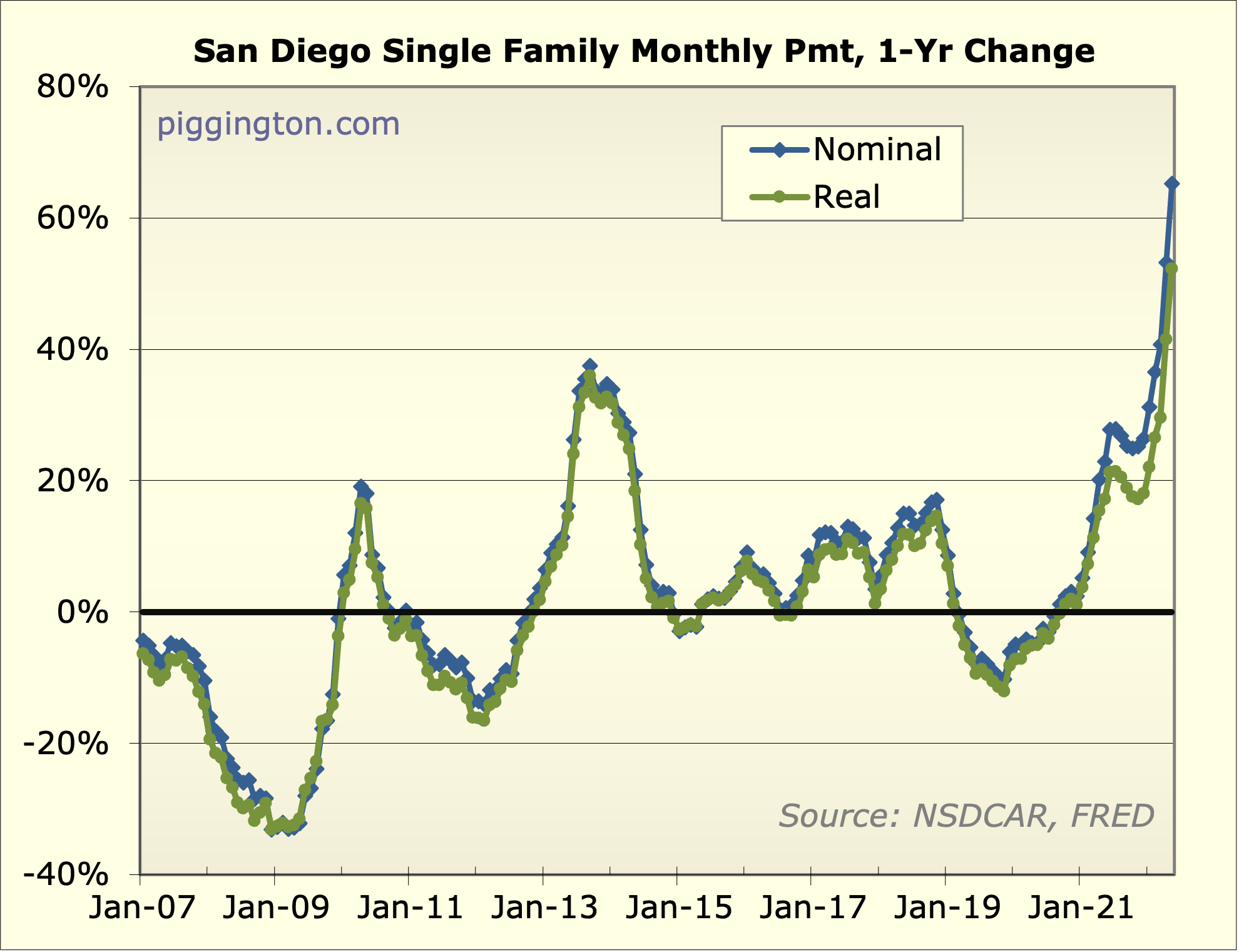

can be sustained. Here is the absolutely nutty rise in monthly

payments over the past year:

Just think about this. A year ago, people were already stretching to

buy houses here. Just 12 months later, for any given house, the

monthly payment required to buy it has gone up 65%! Or 52% in

inflation adjusted terms… assuming the buyer’s income kept up with

inflation (which, on average, is not the case).

These are just astounding numbers and it’s hard to see how this

doesn’t seriously impact demand at this price level, once the higher

rates are fully priced in (rate locks expired etc).

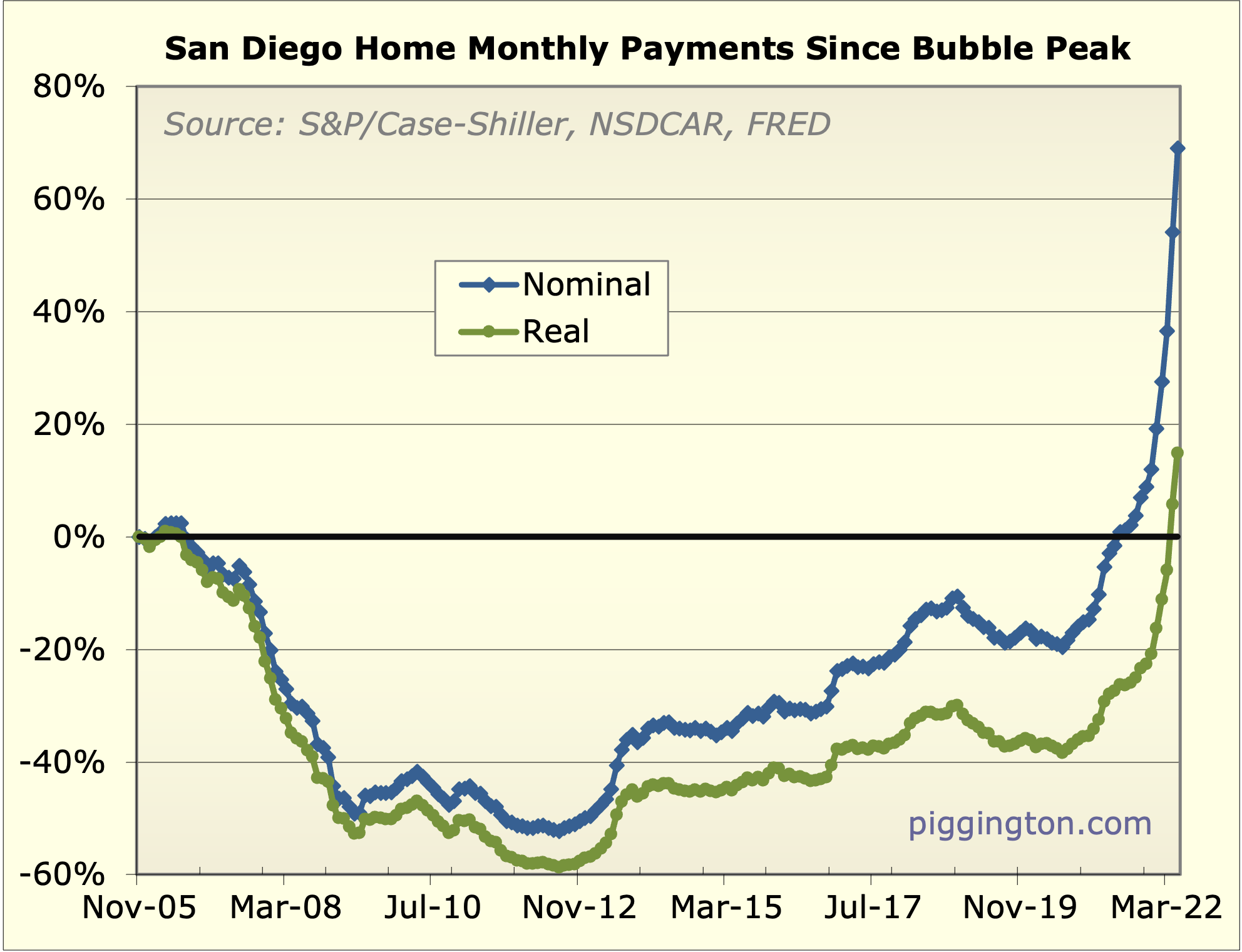

Zooming out, the inflation-adjusted monthly payment is now

comfortably above the bubble peak:

Meanwhile the Federal Reserve appears to be actively targeting a

decline in home prices (or at least valuations). Here’s Jay Powell

from last week’s press conference, emphasis mine:

“I would say if you’re a homebuyer, or a young person looking to buy

a home, you need a bit of a reset. We need to get back to a place

where supply and demand are back together. And where inflation is

down low again and mortgage rates are low again. So this will be a

process whereby ideally we do our work in a way that the

housing market settles in a new place and housing

availability and credit availability are at appropriate

levels.”

In all, my view is that something probably has to give here: if

rates don’t come down, valuations likely will. (Or some combination

of the two).

If that forecast is right, it still leaves open a lot of questions:

Will it be rates, valuations, or both? If valuations decline, how

much of that will be from nominal price declines vs. incomes

catching up to prices? Over what timeline will this all happen? Etc.

I don’t pretend to know the answer to any of these. But I do have a

pretty strong feeling that this current combination of valuations

and mortgage rates cannot be sustained.

Assorted graphs below.

Agree with everything Rich

Agree with everything Rich and coming up forward to where we are now, inventory and pendings are moving in opposite directions at a good clip. Ive long felt this Spring bump was the result of essentially a once in a lifetime supply v demand balance and fully expect us to give all or most of that back fairly quickly (i.e. by the end of 2023) but beyond that Im not so sure there’s much downside.

The inventory is rising at a good clip because demand has fallen sharply in the face of seasonal peak selling season. The unknown at this point is whether supply is and will continue to come in increasingly larger numbers. Is the supply from lifecycle sellers (minimal impact) or “I want to get out while the gettings good” type sellers in much larger numbers that could push us down a bit more than I would ordinarily expect. My bet is on the former and while I expect some of the later I dont see it as a flood and next year it will be Spring again. It always is.

“If that forecast is right,

“If that forecast is right, it still leaves open a lot of questions: Will it be rates, valuations, or both? If valuations decline, how much of that will be from nominal price declines vs. incomes catching up to prices? Over what timeline will this all happen?”

Well it’s nominal values first, which I suspect have already peaked so any sales the second half of this year will show the initial decline. I’m talking aggregate SD Case-Shiller numbers. Rates are still going higher. My crystal ball says 8% mtg. rate peak. I know some pretty smart guys who say the number will hit 10%. Hard to believe this level of inflation will be solved by the end of the year.

Over what timeline? Are we talking peak to trough nominal sales prices? I’ll throw a dart and say a 2025 bottom and reserve my right to amend….

Alot of moving parts here.

2025 sounds about right but

2025 sounds about right but most of it should happen by end of 2024 with 2024 to 2027 being the next WOO

I only watch a couple

I only watch a couple markets. 92011 (Aviara) SFR inventory is up from the low single-digits early in the year to 18 this week (its a small market). My old hood where I sold in mid-2019 92078 (south San Marcos) is up from high single-digits early in the year to 53 SFRs on the market today.

Both cases pretty material increases in inventory and the rapid rise in rates will take some time to show up in demand/pricing. The May closings above were from deals cut/rates locked in Mar/Apr when rates were still lower.

Next few months will be very telling, that’s for sure.

My rental rate/term locked through Mar 2024, hoping that will be a nice entry point after all this settles.

evolusd wrote:I only watch a

[quote=evolusd]I only watch a couple markets. 92011 (Aviara) SFR inventory is up from the low single-digits early in the year to 18 this week (its a small market). My old hood where I sold in mid-2019 92078 (south San Marcos) is up from high single-digits early in the year to 53 SFRs on the market today.

Both cases pretty material increases in inventory and the rapid rise in rates will take some time to show up in demand/pricing. The May closings above were from deals cut/rates locked in Mar/Apr when rates were still lower.

Next few months will be very telling, that’s for sure.

My rental rate/term locked through Mar 2024, hoping that will be a nice entry point after all this settles.[/quote]

Two recomendations. Might want one more year on that on a month to month basis if you can. That way is better for a smooth exit with timing you have more control over. And #2? Get yourself a better agent next time;)

2027 being the next

Mande?

Josh

barnaby33 wrote:

2027 being

[quote=barnaby33]

Mande?

Josh[/quote]

2024 to 2027 = Window of opportunity

DaCounselor wrote:”If that

[quote=DaCounselor]”If that forecast is right, it still leaves open a lot of questions: Will it be rates, valuations, or both? If valuations decline, how much of that will be from nominal price declines vs. incomes catching up to prices? Over what timeline will this all happen?”

Well it’s nominal values first, which I suspect have already peaked so any sales the second half of this year will show the initial decline. I’m talking aggregate SD Case-Shiller numbers. Rates are still going higher. My crystal ball says 8% mtg. rate peak. I know some pretty smart guys who say the number will hit 10%. Hard to believe this level of inflation will be solved by the end of the year.

Over what timeline? Are we talking peak to trough nominal sales prices? I’ll throw a dart and say a 2025 bottom and reserve my right to amend….

Alot of moving parts here.[/quote]

Looking at historical data, I would say nothing is guarantee. https://dqydj.com/historical-home-prices/. Not all recession result in decrease in nominal housing price. Actually, the majority of them do not. This time can be different. We’ll have to wait and see.

IMHO, it will come down to wage inflation and rent inflation. Those two go hand in hand. That will dictate how bad the nominal price decide is.

Sure, every recessionary

Sure, every recessionary period has a different set of facts. After SD RE values ran up about 150% in the 2nd half of the 80’s, there was a recession that corresponded with a nominal drop in SD RE prices beginning around 1990. The recession ended but RE prices continued to drop for another 3 yrs. 15% drop peak to trough.

The last bust saw RE prices drop about 20% before an “official” recession even hit, and continue to drop another 20% through the recession, and then stay flat for a few more years after the recession ended. 40% drop peak to trough.

I think SD RE values held up through dot.com and COVID recessions.

I’m not a sky is falling bear but reading the tea leaves I see a confluence of negative signs. As my friends and I say, Yous Makes Your Bets and Yous Takes Your Chances.

The biggest question I have

The biggest question I have is what will the fed do if we get stagflation? Would they keep on raising rates to fight inflation or lower rate to fight recession or great recession? There’s only 1 time period in recent history where we have stagflation. Will this time be different?

an wrote:The biggest question

[quote=an]The biggest question I have is what will the fed do if we get stagflation? Would they keep on raising rates to fight inflation or lower rate to fight recession or great recession? There’s only 1 time period in recent history where we have stagflation. Will this time be different?[/quote]

If they follow Volcker’s playbook they will target the money supply more so than rates, but in any event consumer credit will get increasingly expensive, like egregiously expensive.

What was Mr. T’s prediction in Rocky III?

My prediction? PAINNNNN!

My prediction? PAINNNNN!

Picked up a newly arrived

Picked up a newly arrived family from India today.

They were going to a rental on Mira Mesa.

His comments: rental prices like New York, they go fast.

$4800 for a 4 BR is not unusual now in MM.

Have to admit, I felt a little sorry but hopefully he has a good salary and things work out.

As long as there is that kind of income, investors like myself with low cost financing probably won’t be selling.

Other riders were telling me investors are still buying even with rates where they are.

A surgeon I work with recently got a 30 year fixed rate at 3.6% so not all the headlines are reflective of the broader reality (in past 45 days). Think the bank required 40% down.

Esco: the discount for very

Esco: the discount for very large downpayment isn’t very big once you get past 30% down. Like 0.1% off going from 30 to 50%. 3.6% 30 year was locked a long time ago and/or involved paying a lot of points for a lower rate and/or rate lock extension fees.

—

Everyone else: Oh my, so many gloomy Guses. Extending what I said earlier,

“Rates obviously matter, but prices will keep increasing as long as we have this massive supply and demand imbalance.

Furthermore, real mortgage rates are lower than 2019, dropping from about 1% to -2%. Moreover, the rate increase isn’t coming in a vacuum. It is largely from an increase in expected inflation, which includes rents.

Thus, while payments on a mortgage for a median SD home have increased, so too have both the current rent it replaces and expected future rents.”

The “high rates will melt prices” scenario seems to require rent growth cooling but rates staying high. How does that work? Housing is highly inelastic in supply and a necessity. Hard to see high inflation continuing but leaving rents behind.

For investors, alternative investments have to be considered too. Treasuries yield 3.3% and are taxed worse than RE. Seems pretty bad compared to RE where both prices and rents tend to increase with inflation, even if it is a bumpy path.

gzz wrote:Rates obviously

[quote=gzz]Rates obviously matter, but prices will keep increasing as long as we have this massive supply and demand imbalance.[/quote]

True but not useful, because it’s unknown whether the supply/demand imbalance will persist. My guess is that at these rates and valuations, it will not.

[quote=gzz]Moreover, the rate increase isn’t coming in a vacuum. It is largely from an increase in expected inflation, which includes rents.[/quote]

I don’t think this matters that much. The monthly payment is up over 50% AFTER inflation (and even more after wages, which haven’t paced inflation). This simply takes a ton of buyers out of the market at these prices/rates. A higher future income stream is a nice idea, but I’d imagine that for most people it’s secondary to whether they can actually buy the place.

Rich, I agree the monthly

Rich, I agree the monthly payment jump is big.

But so are rent increases. The three estimates I posted are 15, 23, and 30% YoY.

Only two years of those makes up for that monthly payment jump.

Where do you expect a home buyer with a 1M price and 800k/6% mortgage to be in 5 years?

My conservative best guess is that buyer:

(1) Will have had at least 1 refi opportunity to cut his payment by 1k+ a month or more;

(2) Will have a locked in housing payment while rents have increased by 25%

(3) Will be sitting on ~250k in appreciation.

Now frankly I think the appreciation and rent increases will be more than a total of 25% over 5 years, which is under 5% per year given compounding and well under expected inflation.

But won’t you at least admit that (1) these aren’t very aggressive assumptions, and (2) if they come true, buying now makes a lot of sense?

The tax-interest-ins aspect of a 800k mortgage is about 4800/mo, and mostly deductible. Skipping that now, but also skipping lost interest on the down payment.

What’s the rent now on a 1.0m sfh? Maybe 3300 but rising fast.

The initial and likely worst comparison with rent is only about 18k. A mere appreciation of 1.8% takes the buyer to breakeven. The next year, the mortgage payment will be the same, more of it will go to equity, and the rent gap may drop to about 15k.

gzz wrote:But won’t you at

[quote=gzz]But won’t you at least admit that (1) these aren’t very aggressive assumptions, and (2) if they come true, buying now makes a lot of sense?[/quote]

No. But I like the phrasing “won’t you at least admit” to suggest that you are stating perfectly reasonable, objective facts, and I’m just being stubborn or something.

[quote=gzz](1) Will have had at least 1 refi opportunity to cut his payment by 1k+ a month or more;[/quote]

Who knows. I continue to submit that you wildly overestimate your ability to predict rates and inflation. (When I first started suggesting this, you were predicting 5 year average inflation of 1.5% iirc… has something happened in the intervening year to make you think you’ve gotten much better at it?)

[quote=gzz](2) Will have a locked in housing payment while rents have increased by 25%[/quote]

Assuming inflation is less than 5% (which one has to in order to accept item 1), why should rents rise faster than overall inflation – especially after the huge surge they’ve already had? I mean this one is certainly possible, but seems over-optimistic as a base case.

[quote=gzz](3) Will be sitting on ~250k in appreciation.[/quote]

No. You can’t just assume that — not when we’re starting from nosebleed valuations/unaffordability.

This is like the people at the top of the bubble who said, yeah it’s expensive, but when you count future appreciation, it’s actually not expensive. That was circular logic back then, and it still is.

So this third assumption strikes me as aggressive (and the other two questionable).

Rich Toscano][quote=gzz

[quote=Rich Toscano][quote=gzz]

No. You can’t just assume that — not when we’re starting from nosebleed valuations/unaffordability.

This is like the people at the top of the bubble who said, yeah it’s expensive, but when you count future appreciation, it’s actually not expensive. That was circular logic back then, and it still is.

So this third assumption strikes me as aggressive (and the other two questionable).[/quote]

Lol, you crack me up Rich. Can I ask what you think will happen with San Diego valuations by the end of 2023?

Pbranding][quote=Rich Toscano

[quote=Pbranding][quote=Rich Toscano][quote=gzz]

No. You can’t just assume that — not when we’re starting from nosebleed valuations/unaffordability.

This is like the people at the top of the bubble who said, yeah it’s expensive, but when you count future appreciation, it’s actually not expensive. That was circular logic back then, and it still is.

So this third assumption strikes me as aggressive (and the other two questionable).[/quote]

Lol, you crack me up Rich. Can I ask what you think will happen with San Diego valuations by the end of 2023?[/quote]

You can ask… :-/

To really answer that, you’d have to know where interest rates will end up, whether we have a recession between now and then, how serious of a recession should one happen, etc. None of which anyone knows.

I mean, I’ll hazard a guess of “probably lower,” just because it seems like we’d have to thread the needle to keep valuations here (somehow inflation/rates coming down a lot without major economic impact). But that’s not very useful…

Rich Toscano wrote:

This is

[quote=Rich Toscano]

This is like the people at the top of the bubble who said, yeah it’s expensive, but when you count future appreciation, it’s actually not expensive. That was circular logic back then, and it still is.[/quote]

In my neighborhood in bay ho, someone bought for ~500,000 in 2007.

It was maybe 2014/5 before their house was worth 500,000 again.

Now it is ‘valued’ at 1.1 million (That value screams bubble, at least to me). But i guess they got their value after 15 years or so?

bewildering wrote:Rich

[quote=bewildering][quote=Rich Toscano]

This is like the people at the top of the bubble who said, yeah it’s expensive, but when you count future appreciation, it’s actually not expensive. That was circular logic back then, and it still is.[/quote]

In my neighborhood in bay ho, someone bought for ~500,000 in 2007.

It was maybe 2014/5 before their house was worth 500,000 again.

Now it is ‘valued’ at 1.1 million (That value screams bubble, at least to me). But i guess they got their value after 15 years or so?[/quote]

Yes, they certainly did — but it required valuations returning to levels almost as high as the bubble peak (which was in turn enabled by a move to all-time low interest rates). Neither of those outcomes was predetermined.

And now the interest rate tailwind has turned to headwind, and yet valuations remain at nosebleed levels vs. history. So my point here is that it’s not predetermined that home prices will magically rise by 5%/year in perpetuity.

Escoguy wrote:Picked up a

[quote=Escoguy]Picked up a newly arrived family from India today.

They were going to a rental on Mira Mesa.

His comments: rental prices like New York, they go fast.

$4800 for a 4 BR is not unusual now in MM.

Have to admit, I felt a little sorry but hopefully he has a good salary and things work out.

As long as there is that kind of income, investors like myself with low cost financing probably won’t be selling.

Other riders were telling me investors are still buying even with rates where they are.

A surgeon I work with recently got a 30 year fixed rate at 3.6% so not all the headlines are reflective of the broader reality (in past 45 days). Think the bank required 40% down.[/quote]

$4800/month is definitely for a larger house in MM, probably 2 stories ones.

Smaller, 3/2 and 4/2 are only around $3500.

an wrote:Escoguy wrote:Picked

[quote=an][quote=Escoguy]Picked up a newly arrived family from India today.

They were going to a rental on Mira Mesa.

His comments: rental prices like New York, they go fast.

$4800 for a 4 BR is not unusual now in MM.

Have to admit, I felt a little sorry but hopefully he has a good salary and things work out.

As long as there is that kind of income, investors like myself with low cost financing probably won’t be selling.

Other riders were telling me investors are still buying even with rates where they are.

A surgeon I work with recently got a 30 year fixed rate at 3.6% so not all the headlines are reflective of the broader reality (in past 45 days). Think the bank required 40% down.[/quote]

$4800/month is definitely for a larger house in MM, probably 2 stories ones.

Smaller, 3/2 and 4/2 are only around $3500.[/quote]

>2000 sf starts at $4500.

need to get down to 1300 sf for $3600-$4000

Escoguy wrote:an

[quote=Escoguy][quote=an][quote=Escoguy]Picked up a newly arrived family from India today.

They were going to a rental on Mira Mesa.

His comments: rental prices like New York, they go fast.

$4800 for a 4 BR is not unusual now in MM.

Have to admit, I felt a little sorry but hopefully he has a good salary and things work out.

As long as there is that kind of income, investors like myself with low cost financing probably won’t be selling.

Other riders were telling me investors are still buying even with rates where they are.

A surgeon I work with recently got a 30 year fixed rate at 3.6% so not all the headlines are reflective of the broader reality (in past 45 days). Think the bank required 40% down.[/quote]

$4800/month is definitely for a larger house in MM, probably 2 stories ones.

Smaller, 3/2 and 4/2 are only around $3500.[/quote]

>2000 sf starts at $4500.

need to get down to 1300 sf for $3600-$4000[/quote]

Yep, 2000 sq-ft is large for MM. Most SFR in MM is below 1400 sq-ft.

This site says SD rents are

This site says SD rents are up 30% YoY.

https://www.connectcre.com/stories/san-diego-rents-continue-to-skyrocket/

This source seems more credible and says it is a mere 15%:

https://timesofsandiego.com/business/2022/06/14/apartment-vacancies-plunged-in-san-diego-county-over-past-year-as-rents-rose-15/

Notably, the more conservative estimator also suggests the rapid increases will continue given the rental market is the tightest ever recorded.

“The vacancy rate across the county dropped from 2.91% in the spring of 2021 to 1.25% currently.”

Zumper tracks median asking rents. The other source is paywalled and says it looks at “weighted” rents.

Both are for apartments. I wonder of SFHs are even higher due to WFH trends, and also the fact that apartment supply is gradually increasing and SFH supply is gradually decreasing.

Here’s a third source saying the rent increases are 23% YoY in SD city.

https://www.rent.com/california/san-diego-apartments/rent-trends

Spoke to a neighbor yesterday

Spoke to a neighbor yesterday about another that rented their house. They are getting $7 to 9K/month here

Also, look out below, the

Also, look out below, the ten-year is now 0.44% below its recent high, 3.044 versus high of 3.483.

If the Fed keeps raising rates faster than EU/Japan, we will just be exporting inflation as the strong dollar means higher local currency commodity prices for them.

Personally I have better uses for my minimal funds, but if I were some German or Japanese pension manager, GSE bonds paying 4.4% right now in dollars sounds a whole lot better than risky 1.5-2% euro bonds.

My point is, the Fed’s ability to set mortgage rates is limited by yield-starved European asset managers. They got burned before buying junky private MBS, but the did fine if they bought and held GSEs.

Will Euros just raise rates too? Probably a bit, but I think their weaker economies and less inflation-averse populations will limit the increases.

Everyone in America had been propagandized about the supposed horrors of inflation. Italians get the same propaganda from their elites, but past experience indicates they are rather immune to it.

Who knows. I continue to

The inflationistas/goldbugs/rate-worry-worts have been crying “OMG THE FED IS PRINTING SO MUCH MONEY” wolf every year since the start of the Great Moderation, roughly 1985. Finally after 37 years, and a multi-generational rarity pandemic, trade war, and shooting war, they kinda got one right.

The one time after decades of shouting the “FED IS PRINTING MONEY OMG ZIMBABWE WIEMAR IS COMING!” the inflationistas kinda sorta got one right, I have not seen much in the way of intellectual modesty coming from them.

Also, my advice here is not to make bets on rates and inflation via bond derivatives or however else one does that, but to go in big in SD RE. My result doing that, which is probably typical for 2011 first time buyers, is a 5,400% gain on my primary residence down payment, which works out to 44% compounded APR over 11 years.

I have not only been right, but very right!

Further, I never said rate increases were impossible or especially unlikely. In fact, over many years, I said my background assumption is the market consensus for rates and inflation is correct, and that consensus was until the pandemic very low.

If I had some strong certainty rates would be low for a long time, as opposed to a moderate faith in the market consensus, I would not have locked my mortgages for 30 years. I believe I also told Flu and others who were considering paying off their mortgages entirely that I wouldn’t do that, because they never know if they’ll ever get such cheap money again.

It is hard to make predictions like this. However, marginal potential buyers need to decide to buy now, later, or never, and base their decision on guesses about the future, not knowledge.

Yes, it is possible that, in June 2027, we’ll look back at June 2022 as the 5-year-low in mortgage rates, and during that period there will be no real opportunities to refi to a lower rate. My guess: there will be multiple opportunities to refi to lower rates, just like there is in most 5 year periods.

I disagree that the 30-year mortgage rate can’t be far below inflation, which is what you appear to be saying here.

Indeed, the 30-year rate is currently about 5.7% while May 2022 YoY inflation is 8.6%. Why couldn’t inflation decline by 3.5 points to 5.1% and mortgage rates decline 1.5 points to 4.2%?

That’s not my assumption, but my conservative best guess based on a lot of data in a market I have been closely following since 2005.

I don’t agree valuations are nosebleed. They are well above rents for the first time in a long while. But while you are either too bearish to agree with my three predictions, or too uncertain to hazard any yourself, I think they are all pretty reasonable, and result in prices that are easily justified.

And of course with the market so tight, and new construction of any sort in SD County so low, and the quantity of coast-close SFH on 5000+sq ft unshared lots going down each year, the number of people who agree with my conservative assumptions doesn’t need to be very high for prices to keep rising.

OK, the part about “omg the

OK, the part about “omg the fed” people is confusing and has nothing to do with this conversation. I ignore those people (and just banned one) and I am going to ignore that part of your comment.

The part about your enviable RE investing track record is also irrelevant; at no point did I question your RE investing success. I invoked your wildly off-the-mark inflation forecast specifically to underscore that one should not depend too heavily on inflation/rate forecasts… that’s all.

The rest of your reply is reasonable and relevant, but I just don’t see things as you do. As you say — I believe your assumptions (notably #3) are too optimistic to be a base case. And I’ve hazarded all the predictions I feel comfortable hazarding already.

Prices will give in.

In my

Prices will give in.

In my neighborhood, zip 92129, a house went to market 4 weeks ago for $1.2M, sold for $1.0M.

wawawa wrote:Prices will give

[quote=wawawa]Prices will give in.

In my neighborhood, zip 92129, a house went to market 4 weeks ago for $1.2M, sold for $1.0M.[/quote]

What would that house sell for a year ago? Is it an increase Y-o-Y or has it gone flat? Is that a 20% price drop or was the $1.2m a wishful price?

My guess would be it sold for

My guess would be it sold for about what it would have sold for last year +/- a little. The owner was impatient and wanted a quick deal. Possibly to cash investor with 2 week close. Givee me address and I can research.

Generally speaking homes arent selling at that kind of discount but there are always outliers. You see them in MM from time to time

I’m seeing several examples

I’m seeing several examples in 92027/92127 where the most recent listing price from May was overinflaated even given the rise of the past 12 months.

Then a cut occurs but it the house is still +20% over last year.

So for now, I’m mostly seeing cuts of wish prices.

In 92078, one neighborhood I watch has what I would consider a “real” cut vs last years very inflated but still closer to a fair value price.

As so often is the case, “it’s complicated”.

Still early. We should see

Still early. We should see occasional relenters on price but we’ll see as many or more who will just pull it off the market. I just checked my area and saw about a dozen many of which were rentals get pulled off and re-rented. No doubt we are seeing increasing softness but as you said what that means and how things play out is still tbd

Esco, that matches my

Esco, that matches my observation too.

Prices rose so quickly it became very hard to price at fair market value.

I think periods of rapid appreciation also create greater submarket divergence in appreciation, both within and between neighborhoods.

Prices are way down in SF city and NYC, and to a lesser extent their suburbs. I certainly don’t dismiss a decline here, but I think we lack the outmigration of high income people unhappy with growing urban crime and general disorder, and who now have the ability to WFH in less crowded areas.

The stats on Manhattan are mind boggling, less than 10% of office workers are back to M-F in office schedules. One reason I short BXP.