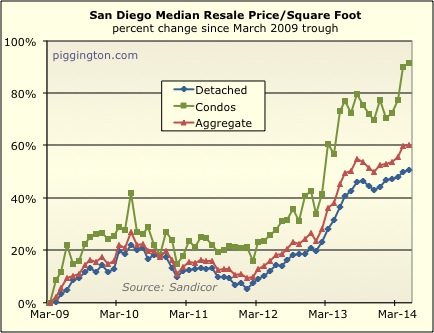

San Diego’s median price per square foot eked out a small gain in

May, with the single family home median rising .3% from April.

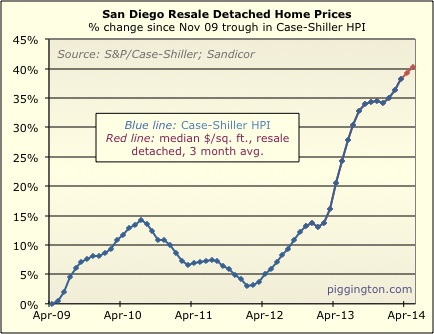

Looking at the Case-Shiller estimate, which smooths things out with

a 3-month average, the upward trend seems to have slowed a bit but

remained intact.

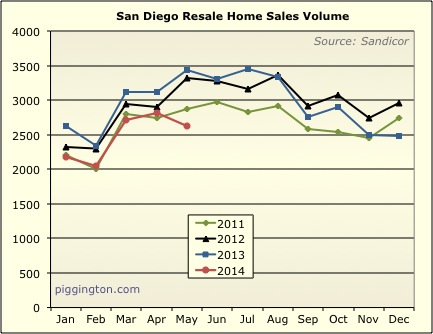

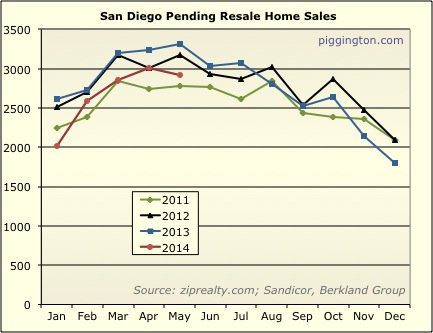

Activity backed off, with both closed and pending sales down:

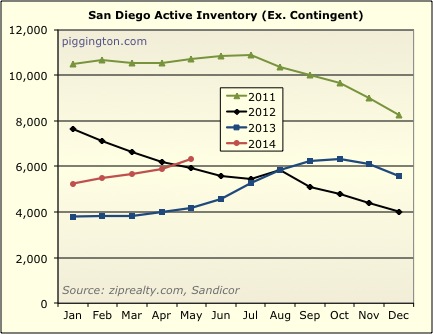

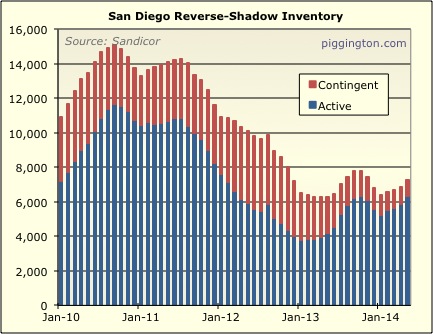

Inventory kept creeping up:

But that number masks what’s going on beneath the surface, which is

that contingent inventory (short sales awaiting bank approval,

mostly) has been declining as active inventory has risen pretty

strongly. Here’s a look at just active inventory, showing that

actives just surpassed early-2012 levels. Note how much more

active inventory there is than at this time last year:

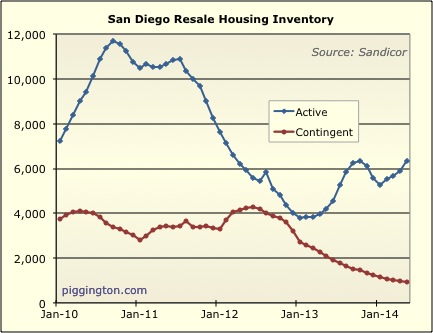

I thought it would be interesting to graph active and contingent

separately:

You can see how the two have gone in completely opposite directions

starting in early 2013, causing the decline in contingents to offset

the rise in actives. The difference is that contingents were

not really inventory in the traditional sense… they were still

listed, but they were “spoken for,” with a buyer’s offer being

reviewed by the owning bank. Active inventory, on the other

hand, is real inventory that is available to buyers, so you could

argue that actives alone are a better indicator of supply than the

overall inventory number.

Here’s a similar graph, showing how contingents were once a big

proportion of inventory… now, not so much:

Here’s a longer-term look at total inventory:

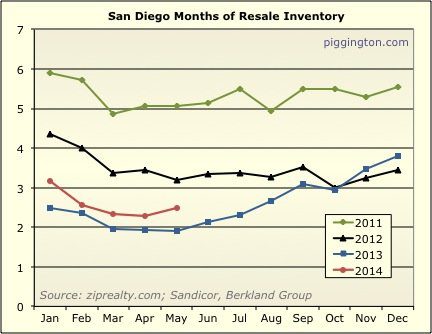

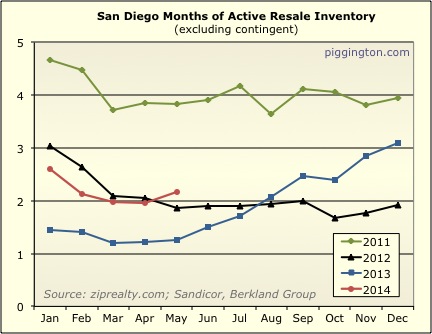

Here are the usual graphs on months of inventory. The

conclusion remains the same as it’s been recently — months of

inventory has been rising but remains quite low historically:

But given the active vs. contingent issue described above, it makes

sense to also look at months of active inventory.

These graphs suggest that the market is nowhere near so dramatically

undersupplied than it was a year ago — but that inventory is still

on the low side, historically speaking. It seems that months

of active inventory is still at a level that implies upward pressure

on home prices… but if inventory keeps growing as it has

been, and sales weaken further, that could change.

Thanks for the post. I

Thanks for the post. I learned that we can’t really predict what will happen next in the market.

It seems that months of

About time that some rationality was injected into the SD housing market!

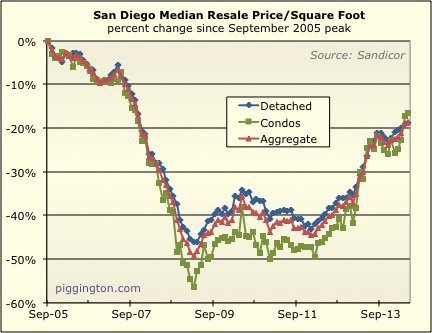

From Graph #2, I’m seeing

From Graph #2, I’m seeing that ppsf of SFR’s in SD County is about 19% lower than the Sept 2005 peak.

From Graph #5, I’m seeing that sales volume (sold SFRs) are at 850-900 units less than the same time last year. ’11, ’12 and up until Sept ’13, SD County SFR’s had successively higher sales volumes and then they began falling at the beginning of Sept `13.

The graphs comprise the entire county of resales, both newer and older inventory.

Rich, correct me if my assumptions are wrong here.

If prices are still 19% below peak and sales volume has been falling, to me this means that end users (owner occupiers) “expectations” have not adjusted after NINA and other exotic mortgages were no longer available, IMO. This is so because investors have, for the most part, left the market after realizing there would be little money to be made (or none) in “flipping” and already have enough rental homes to manage. Many would-be buyers today (mostly would-be 1st timers) saw in the past what their peers purchased and entertained in (move up and luxury homes) due to the “fog a mirror, get a loan” financing available at the time and they will not settle for less today.

In CA coastal counties, these would-be buyers would rather rent than buy a house or in an area that they consider “below their lofty expectations.”

Until these unrealistic expectations catch up with reality, most of these pollyanna would-be buyers will continue to be at the behest of their landlords as the vast majority of the most well-located and well-established resale inventory in CA coastal counties is now controlled by owners who can sell at any future date of their choosing and can choose to keep their non-owner-occupied SFRs in rental service (or even vacant, with furniture) for as long as they so desire … or even pass the rental property onto their heirs.

My advice to would-be buyers out there who are still waiting to find “the `perfect home'” is, take it or leave it … or go find a highly motivated (underwater or near underwater) owner to make a deal with out in lizardland, with all its attendant extra fees and taxes. Nothing has changed in this regard in the last 40 yrs (in my memory) except for the decimation of thousands of acres of lizardland and the resultant creation of “Community Facilities Districts” and all the attendant fees and taxes attaching thereto.

The “millenium boom” buyers (and buyers who bought distressed property cheaply in the ensuing years) raised today’s would-be buyer’s expectations of a first or second home through the roof. Even though most of the distressed SFR’s purchased within the county at low prices between ’09 and ’12 needed major work that most buyers are unable to do themselves and can’t afford to hire done, psychologically, the “disconnect” of what is available in their price range today and what these (holdout and more recent) would-be buyers feel they deserve is a difficult nut to crack.

All is as it should be and always was.

What used to be the

What used to be the (“well-built”) 1200 – 1600 sf SD “starter home” is now “investment grade” to Gen Y. It’s not good enough to buy for their first home IF they can even afford it. If they CAN afford it, the area it sits in is not “good enough” for them. Both were “good enough” for previous generations’ first and subsequent homes (this was LONG BEFORE all the expensive `gentrification’ took place around them) but it is not “good enough” for the vast majority of today’s 1st and 2nd time buyers.

This is the biggest reason for the stalemate (drop in lower-priced sold comps) in recent months, in my humble opinion.

If there is actually a drop in move-up/luxury home transactions in the county ($650K+), I don’t know what the reason would be for that.

The graphs shown here don’t break down sold statistics by property tier (low, mid and higher-priced) so it is difficult to tell what is really happening on the street or in particular micro-areas. I’m personally seeing low and mid-priced SFR’s listed as “traditional sales” sit on the market longer in the established zip codes I follow.

[snark]The best way to teach

[snark]The best way to teach a Gen Y about supply and demand, the early bird gets the worm and to be more decisive in life and to be ready to act when the oppt’y presents itself is to get them a job in Silicon Valley and place them in SF or any point north or south for ~45 miles (or east for ~25 miles) and tell them to find a place to live within a week and/or start making offers on homes today.

Their “lofty expectations” will have completely corrected themselves within one hard day of “shopping.”

As it should be.[/snark]

Good to see you are still

Good to see you are still around BG. Do you think it is really about FTBs expectations? Many of them won’t have any past reference to measure their ‘expectations’, perhaps apart from the home they grew up in. The graphs show a massive three fold decline in inventory from 2006/7 till now. If you look at how prices track inventory levels, any buyer who has done his homework is going to think about timing. Add in the competition that many FTBs face from cash investors and you might conclude this isn’t about misplaced expectations so much as a distorted market, where the option to rent may be preferable. Having said that, I believe we (most of us) have some kind of innate sense of worth, or value. They will differ, but there will be a consensus.

As I stated before Jazzman, I

As I stated before Jazzman, I believe the unrealistic expectations of 1st and 2nd time buyers in CA coastal counties (Gen Y/younger Gen X) stem from what they have seen their peers able to buy between 2004 – 2007 (w/”exotic” financing) and 2009-2012 (w/all cash or large cash downpayment PLUS DIY skills that they don’t have).

They saw the upgraded tract homes and locations of of the homes their millenium-boom buyer-peers bought (who technically couldn’t afford the home OR the location) and the glitzy upgrades put in older homes by their post millenium-boom buyer peers and have absolutely no idea how much money and work it took to get it that way.

They can only “see themselves” in a home with granite, low-E windows, expensive slate/tile roof, entertainment backyard, etc, due in part to HGTV showing their “peers” buying this type of home in flyover America for a song ….

When they actually “look” at a circa 1947 listing in a CA coastal area of their choice (common example in established, coveted area in coastal CA county, possibly with view) with its small closets, no foyer, porch stoops to front and back doors, wall heater, composition roof, lack of room in bath(s) for two sinks, possible undersized garage, etc, they don’t want it even if they can afford it and it is a better investment than a tract home in Rancho Faraway.

They want the lizardland-type cheaply-built 1900+ sf house with larger lot in the best, most established areas of SD and those houses (although far better-built) typically have asking prices +/- $1M (even at 19% below peak). These buyers won’t take what’s on offer in their price range in the area of their dreams or even an adjacent area so they invariably make the tradeoff to buy something in lizardland and commute.

A huge contingent of would-be 1st time buyers can’t be pleased at all in SD County, no matter what their price range is. For this and all of the above reasons, I would HATE to waste my time with this type of buyer for fear they would attempt to run me ragged for months or years and never consummate a deal. 1st and 2nd timers didn’t used to be so picky but, of course, there was much less “newer” construction available (<15 yrs old) for sale at any given time prior to 2000.

Aside from the high-priced view areas (ex: La Playa SD), this leaves most of SD County’s older, established areas with a small captive audience of buyers who grew up there and/or want to live near other established relatives and/or jobs located in the urban core.

It’s the same in ALL coastal counties of CA and it’s never going to change. The reason it won’t change is Props 13, 58 and 193. There is absolutely no incentive whatsoever for a longtime owner or their heir to sell a perfectly decent SFR with annual taxes of 1/2 to 1/12 of what they should be. They make out far better by renting it out and paying $1000 to $2000 annually in taxes and insurance. OR, if they don’t need the proceeds from rental income or a sale, furnish it and let guests use it every few months.

There are several houses around me which have been “vacant” and furnished for many years and have never been listed and my ‘hood is but just ONE small microcosm of the county.

The young buyers of today aren’t going to be able to wear down owners like this on price in a listing, unless the last owner just died and none of their heirs want the property (rare in coastal counties). In other words, these listings are typically in the “strongest hands.” No one can’t fix this. It is institutional and this is what today’s FTB’s (and 2nd time buyers who may be a FTB in a CA coastal county) don’t understand. Like you stated here, Jazzman, they don’t see value in urban SFR’s which may be a little outdated because they don’t understand what constitutes “value” in a CA coastal county. It’s the “cheap glitz” (ex: painted hole in LR wall in lizardland vs floor-to-ceiling brick FP with raised hearth in older area) that draws them in out in lizardland and most of them honestly have no idea exactly what it is that they are buying (land/location wise) or how the area will fare value-wise in the future because it is untested or tested very little (with mostly heavy distress sales in recent years). An agent can’t steer them otherwise. That is what they want and they know it when they see it. The reality of what they just purchased doesn’t hit them until they have to begin paying pricey MR and HOA dues and/or a major wildfire strikes behind their backyard.

As time marches on, more and more of the SFR inventory in the best locations throughout the state will be deliberately withheld from the market. This has nothing to do with area or sellers trying to “time the market” and everything to do with a property’s ultra-low assessment and a family holding it for eventual heirs.

Let me ask you, Jazzman … if you owned or “inherited” a 1400 sf 3/1/1 home located in SD County (circa, say, 1950) which would rent for a steady $1750 month and cost you $1250 in taxes and insurance annually (total carrying expense), would you move into it yourself, rent it out or put in on the market?

bearishgurl wrote:

Let me ask

[quote=bearishgurl]

Let me ask you, Jazzman … if you owned or “inherited” a 1400 sf 3/1/1 home located in SD County (circa, say, 1950) which would rent for a steady $1750 month and cost you $1250 in taxes and insurance annually (total carrying expense), would you move into it yourself, rent it out or put in on the market?[/quote]

1) I would not move into to it, because I doubt it would meet my “expectations” 🙂

2) I wouldn’t rent it because it is unlikely to meet my benchmark cap rate.

3) I would have sold in 2006/7, or might consider selling it in this market, and would reinvest for a better return elsewhere.

Incidentally, anyone know Richmond, VA or Savannah GA? Some beautiful properties at quite reasonable prices in both places.

http://www.trulia.com/property/3080285801-5113-New-Kent-Rd-Richmond-VA-23225

http://www.trulia.com/property/3094809509-40-E-50th-St-Savannah-GA-31405

Jazzman wrote:bearishgurl

[quote=Jazzman][quote=bearishgurl]

Let me ask you, Jazzman … if you owned or “inherited” a 1400 sf 3/1/1 home located in SD County (circa, say, 1950) which would rent for a steady $1750 month and cost you $1250 in taxes and insurance annually (total carrying expense), would you move into it yourself, rent it out or put in on the market?[/quote]

1) I would not move into to it, because I doubt it would meet my “expectations” 🙂

2) I wouldn’t rent it because it is unlikely to meet my benchmark cap rate.

3) I would have sold in 2006/7, or might consider selling it in this market, and would reinvest for a better return elsewhere….[/quote]

Jazzman, I don’t think you’re quite understanding here. That’s $1250 ANNUALLY in total carrying expense, NOT $1250 monthly. It meets my “benchmark cap rate” just fine. If you can do better, let us all know how, please.

bearishgurl wrote:Jazzman

[quote=bearishgurl][quote=Jazzman][quote=bearishgurl]

Let me ask you, Jazzman … if you owned or “inherited” a 1400 sf 3/1/1 home located in SD County (circa, say, 1950) which would rent for a steady $1750 month and cost you $1250 in taxes and insurance annually (total carrying expense), would you move into it yourself, rent it out or put in on the market?[/quote]

1) I would not move into to it, because I doubt it would meet my “expectations” 🙂

2) I wouldn’t rent it because it is unlikely to meet my benchmark cap rate.

3) I would have sold in 2006/7, or might consider selling it in this market, and would reinvest for a better return elsewhere….[/quote]

Jazzman, I don’t think you’re quite understanding here. That’s $1250 ANNUALLY in total carrying expense, NOT $1250 monthly. It meets my “benchmark cap rate” just fine. If you can do better, let us all know how, please.[/quote]

There is not enough to go on to give an accurate picture, but rental property insurance costs alone would be close to $1,250. When you add in what you normally pay for property taxes in CA, most homes are going to be much higher. Very few homes is CA provide a decent cap rate. That’s well documented. Prove me wrong and I’ll buy one from you. Show me a property I can buy today that offers me a net return of 5%, and is average risk (so no war zones). This isn’t even achievable in Las Vegas, or Phoenix anymore due to price hikes. Note, you cannot use yesteryears’ prices, otherwise you will need to provide opportunity costs. Here’s the numbers you need to provide to arrive at a true net return:

Market or Appraised Value

Purchase Price

Closing Costs & Fees

Total Cash Investment

Monthly Rent (GSI)

Annual Property Tax

Annual Utilities

Annual Landscaping

Annual Insurance Premium

Vacancy Rate (% of GSI)

Maintenance Rate (% of GSI)

Property Mgmt Rate (% of GSI)

Gross Scheduled Income (GSI)

Less Vacancy Amount

Gross Operating Income (GOI)

Annual Operating Expenses

Property Management

Annual Property Taxes

Annual Utilities

Annual Landscaping

Annual Insurance Premium

Repairs & Maintenance

Total Operating Expenses

Net Operating Income

Less Debt Service

Before-Tax Cash Flow (BTCF)

Cash-On-Cash ROI

But this isn’t the issue. You raised the point over FTBs unrealistic expectations of ‘bang for their buck’. I believe that for the majority of FTBs who expectations are not met, they are justified. It’s a rotten deal for many of them. Being pulled in by record low rates, either then to be turned down for a mortgage because the don’t meet the tighter credit standards, or to lose out to cash rich investors who don’t care how much they pay. Then to have so little choice, and to be paying over the odds for it. I sympathize. FTBs should be maintaining or raising their expectations, not lowering them. It wasn’t their fault.

You make a lot of very good points, but I’m left wondering whether you just had a bad experience with one or two FTBs, or there’s an element of sour grapes on your part.

As usual, Jazzman, you’re

As usual, Jazzman, you’re overthinking everything, just like you did with your failed CA house search (literally UP and DOWN the state) a few years back, when asking prices were substantially lower than today. It is telling that you still don’t have a house in CA. Perhaps you don’t want one anymore.

I’m telling you that I was there when the owner wrote her annual check to her insurance company last month. Owner occupied, said home’s annual insurance premium was $650 (not in fire-prone area or type A floodplain). There is no earthquake insurance. I just double-checked its tax bill yesterday online and it was just short of $600 annually. I fudged a little on the age of the house +/- 3 years but the current owner has owned it since 1956-57. THOSE ARE THE ANNUAL EXPENSES! The owner is free to manage it themselves, get a relative to manage it for them or hire it managed at 8-10% of rent.

*****

Most inexperienced buyers are not being wise when they shun property for age, minor problems or because the house is a little too small. They also aren’t wise signing up for exhorbitant HOA/MR when they are still planning on growing their family or already have two or more minor kids, imho. Kids cost way too much today to throw away many thousands per year on HOA/MR (for ANY income level). There are too many unknown variables in the lives of a (vulnerable) family of four or more, including being at the mercy of multiple landlords for years if they are planning on staying in the same area and not purchasing a home because they can’t get an accepted offer on a “dream” property. The generations before them “settled” on their first and second home purchases (yes, right here in SD County). Gen Y believes they are too good to “settle” in their home purchase. They don’t believe in the concept of “starter” homes. Most want the moon on a beer budget and are “picky” beyond belief for all the reasons I stated above. This causes them to end up making poor buying decisions for themselves (condo when they could have gotten a SFR with much better appreciation, high HOA dues and/or MR, etc) because they feel they are too smart to listen to counsel. It’s not like this everywhere, namely SF Bay area (close in), where Gen Y feels extremely fortunate to have an 1150 sf bunglow circa 1947 for their family of four. But SD County 1st (and 2nd) timers today have a HUGE sense of entitlement. The type of home they want for their 1st/2nd home is the type I bought for my 9th home. So they stay renters for many more years than I did.

This dearth of “end-users” for low, moderate and mid-priced SFR’s today in SD County is a large part of the reason for slowing sales. This same group was whining when they felt they couldn’t compete with cash investors in recent years and now that the bulk of those buyers are gone, where are these holdout buyers now?

They’re still on the sidelines bitching and complaining that home prices are too high (all the while their kids are growing up in front of their faces) instead of buying something reasonable and permanent to raise their families in.

GROW UP, Gen Y! Every generation had the same problem except YOU get the benefit of ultra-low fixed mortgage rates. If you don’t take advantage of them while the getting is good, you will miss out and wish you had down the road … while you’re opening up another rent-increase letter…

Oh, I forgot to mention that

Oh, I forgot to mention that the property in question is worth approx $385K (minus ~$25K for selling costs, incl tent fumigation) leaving $360K to seller at COE. To the vast majority of these owners, a property like this is not worth selling, due to the $600 annual tax bill and this particular owner (like most of them) doesn’t need the sales proceeds.

This leaves an “investment amount” of approx $360K

Your annual expenses are approximately $1450 (adding $200 to a $650 homeowner’s policy for rental liability)

Your mgmt fee would be approx $140 – $175 mo if you chose not to manage it yourself

A gardener would only cost about $150 per month because it isn’t complicated. A prospective tenant may agree to take care of the landscaping

Partial reimbursement for tenant water bills (for landscaping) might cost $20 – $30 per month six months per year (upon presentation of tenant’s water bills)

A year’s rent would be $21,000 in income assuming it was rented all 12 months. Expenses would average $5700 per year if you hired a property mgr (excluding emergency repairs). This leaves a pretty steady passive net income of $15,300 on an “investment” of $360K or 4.25% (without major repairs) for basically doing nothing.

Bear in mind that if you decide to sell this property, its ultra-low assessed value will disappear. That’s why the many thousands of owners just like this one will withhold these properties from the market into eternity. There is absolutely no reason whatsoever to sell if you don’t need the cash.

The claims above fly in the

The claims above fly in the face of fact, at least as known to me. Last year I bought a 1930’s vintage house in Kensington, from a seller who had lived there for 40 years and had a $1500 assessed tax base on a property in the 75th percentile of asking prices in SD county. As I write this there are multiple other houses on the market in Kensington with similarly low assessed values, implying decades long ownership.

Goofy wrote:The claims above

[quote=Goofy]The claims above fly in the face of fact, at least as known to me. Last year I bought a 1930’s vintage house in Kensington, from a seller who had lived there for 40 years and had a $1500 assessed tax base on a property in the 75th percentile of asking prices in SD county. As I write this there are multiple other houses on the market in Kensington with similarly low assessed values, implying decades long ownership.[/quote]

Hi Goofy. Welcome to Piggington! I think Kensington is a jewel and a very special community … one of a kind. Congratulations on your successful purchase in one of SD’s finest and most well-located communities! Based upon your post, it appears that your seller paid $61-62K for your home in ~1973. The average price for a home in SD County back then was likely ~$35K so the original portion of your home (if it has been remodeled at some point) must have been larger than the average 1500 sf home of that era and/or had plenty of appealing architectural details. What a windfall your seller was able to make by selling in 2013 (irrespective of improvements they made to the property over the years)! This windfall (assuming no outstanding mtg was on the property) no doubt certainly lessened the pain of losing their ~$122K assessed value on the property. However, the $750K++ ? sale proceeds this seller made over his original purchase price is not the norm in SD County. It is well above the norm for all the reasons stated above.

The subject property I referred on this thread was sold for approx $16-17K in 1956-57 and is worth approx $385K today. This depiction of a “bread and butter” home long-owned by the 75+ yr old demographic is representative of the many thousands of paid-off homes with low assessments in SD County which I was referring to.

I found two current listings (possible comps to your home?) in Kensington which could have possibly been long-owned by the seller where it appears they would lose their ultra-low assessment if they were got an offer they would accept.

small house with Mills Act potential, asking $849K:

http://www.sdlookup.com/MLS-140023655-4150_Lymer_Dr_San_Diego_CA_92116

Assessed at $89,446; current tax bill $1100

***

med-sized house on nice lot, asking $1,399,999:

http://www.sdlookup.com/MLS-140030668-5032_Hastings_San_Diego_CA_92116

Assessed at $146,911; current tax bill $1776

***

Both of these homes apparently sold to the current owner prior to 1/1/82 (the earliest date of online county recorder filings) but we can’t tell when without viewing the filed documents.

I think it is very interesting that these owners are listing these “trophy properties” with extremely low tax bills. They will undoubtedly make a lot of money if successfully sold for their listed price (even factoring in remodeling and improvements). Both of these homes are well above the SD norm in pricing and value.

I haven’t studied any micro-areas recently to find out the percentage of listings withdrawn from the market due to seller’s not being able to get their price. The possibility exists that sellers with very low assessments, such as the ones who own these two listings, are “testing” the market but I can’t comment if these asking prices are fair.

Perhaps urbanrealtor can chime in here.

Thanks for your post, Goofy. Do you know of any other current listings in Kensington which are currently being listed by owners with very low tax assessments? Even pocket listings?

bearishgurl wrote:

Based upon

[quote=bearishgurl]

Based upon your post, it appears that your seller paid $61-62K for your home in ~1973… snip… This windfall (assuming no outstanding mtg was on the property) no doubt certainly lessened the pain of losing their ~$122K assessed value on the property. However, the $750K++ ? sale proceeds this seller made over his original purchase price is not the norm in SD County. It is well above the norm for all the reasons stated above.

[/quote]

Analysis is pretty much spot on. I don’t think the profit was quite $750k++, but definitely north of $675k. We feel very fortunate that we were able to buy a gorgeous old spacious house with high ceilings and lots of light, with nothing other than cosmetic maintenance required and one bathroom renovation, for less than $360/sqft. Seller was pretty motivated, and the home was selling “only” $50k above the upper range of the hot band, where new listings went pending on the Monday after being listed.

[quote=bearishgurl]

The subject property I referred on this thread was sold for approx $16-17K in 1956-57 and is worth approx $385K today. This depiction of a “bread and butter” home long-owned by the 75+ yr old demographic is representative of the many thousands of paid-off homes with low assessments in SD County which I was referring to.

[/quote]

The same is largely true in Kensington. I will enter my 50s a few years from now, and we are the “young babies” in the neighborhood. Every time an ambulance goes by I exercise my black humor with my wife… “here goes another home on the market”.

However, there are also demographic factors at play that you do not account for in your analysis. Schools around Kensington are terrible, if we had school-aged kids we would have probably never contemplated a purchase there since we can’t afford Kensington AND private school. The lack of modern amenities does not appeal to many in their 30s and 40s, even if they can afford the price tag. Rooms tend to be boxy, layouts somewhat cramped, closet space often non-existent. These are very real considerations that probably drive much of the Rancho Far Away purchasing logic. My boss, who can afford to buy pretty much anything in Kensington or Mission Hills, but has 4 kids, built a custom multi-M$ house in a ritzy enclave in far North County.

[quote=bearishgurl]

I found two current listings (possible comps to your home?) in Kensington which could have possibly been long-owned by the seller where it appears they would lose their ultra-low assessment if they were got an offer they would accept.

[/quote]

These are two that came to mind, there may be one more. The inventory in Kensington is surprisingly high – after being close to zero last year, there is now at least one house for sale on pretty much every block.

[quote=bearishgurl]

I think it is very interesting that these owners are listing these “trophy properties” with extremely low tax bills. They will undoubtedly make a lot of money if successfully sold for their listed price (even factoring in remodeling and improvements).

… snip…

Thanks for your post, Goofy. Do you know of any other current listings in Kensington which are currently being listed by owners with very low tax assessments? Even pocket listings?[/quote]

There are at least 1-2 more with mid’80s assessments and $3-4k tax bills that are also on the market. I agree that Kensington is not exactly representative of the SD market at large, and seems to be zigging when everyone is zagging – plentiful inventory and properties staying on the market 30+ days.

I guess I’m a would be FTB.

I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.

danthedart wrote:I guess I’m

[quote=danthedart]I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.[/quote]Obviously hind sight is 20/20, but just out of curiosity, why didn’t you increase your bid after 1-2 places that you were being out bid on? After a few failed bid, didn’t you feel like what you were offering was below market, hence others are willing to bid higher?

AN wrote:danthedart wrote:I

[quote=AN][quote=danthedart]I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.[/quote]Obviously hind sight is 20/20, but just out of curiosity, why didn’t you increase your bid after 1-2 places that you were being out bid on? After a few failed bid, didn’t you feel like what you were offering was below market, hence others are willing to bid higher?[/quote]

Because we couldn’t afford to raise our bid.

We offered list and a few times a bit above list, but we really couldn’t afford to do that. It would eventually get sold for all cash to an investor. What it comes down to is that we never could actually afford a house in the area. I’m guessing would have had to offer 400k+ plus a lot of renovation. So comparing to the houses on the market now for 450k+, the actual cost isn’t very different now than it was for us back then… just the prices were deceiving. Those prices were for investors, not for FTBers. So we thought we could afford a house when we really couldn’t.

danthedart wrote:AN

[quote=danthedart][quote=AN][quote=danthedart]I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.[/quote]Obviously hind sight is 20/20, but just out of curiosity, why didn’t you increase your bid after 1-2 places that you were being out bid on? After a few failed bid, didn’t you feel like what you were offering was below market, hence others are willing to bid higher?[/quote]

Because we couldn’t afford to raise our bid.

We offered list and a few times a bit above list, but we really couldn’t afford to do that. It would eventually get sold for all cash to an investor. What it comes down to is that we never could actually afford a house in the area. I’m guessing would have had to offer 400k+ plus a lot of renovation. So comparing to the houses on the market now for 450k+, the actual cost isn’t very different now than it was for us back then… just the prices were deceiving. Those prices were for investors, not for FTBers. So we thought we could afford a house when we really couldn’t.[/quote]Hmmm… a few years ago means 2008-2011. A 3/2 in West side of Mira Mesa were going for ~$325-350k. I know, because I was a first time buyer in that time frame as well. There were even threads on here where some lucky people landed short sales below $300k. So, I’m not sure why you’d say you can’t get a place between $300-400k. All 3/2 & 4/2 were between $300-400k back then. It didn’t really cross over $400k until ~2012-2013. Unless you were only interested in completely remodeled places, which were bought and flipped by flippers.

danthedart wrote:I guess I’m

[quote=danthedart]I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.[/quote]

dan, there are plenty of other communities in SD County where you can still buy a SFR for $300 – $400K. MM, although convenient to high-tech jobs, isn’t the be-all and end-all of moderately-priced SFR’s in the county. You can likely get more bang for your buck in some areas of South County, East County or North County. Most of SD Metro (where MM lies) is a hard nut to crack for moderate income buyers, price-wise.

So yes, you’re being “too picky” because you have not expanded your search.

For example, I just received this “sold comp” in my e-mail this morning:

http://www.redfin.com/CA/Chula-Vista/620-Date-Ave-91910/home/5967288?utm_source=myredfin&utm_medium=email&utm_campaign=instant24_listings_update&utm_content=address&reinfo=ZXhwSWQ9MjExNzY4MyZleHBJbnN0YW5jZUlkPTE3MjkyMjE1NzY5MjEmY2F0ZWdvcnk9ZW1haWwubGlzdGluZ2FsZXJ0cyZjb2hvcnRJZD1Nb2JpbGVGaXJzdCZ0YXJnZXQ9aG9tZS5hZGRyZXNzJmxvZ2luSWQ9MTU3NjkyMQ==

It’s quite a bit bigger than the avg MM house (due to permitted room addition(s)) and is situated less than one block behind a regional mall (NOT a trafficky street) in a very safe and tidy established area. It’s also on a local bus line (to the trolley) and just 3 blocks from a bus line which goes into DT SD.

Closed yesterday for $375K.

Oh, and I forgot to add that this area runs 8-12 degrees cooler than MM about six months per year 🙂

bearishgurl wrote:danthedart

[quote=bearishgurl][quote=danthedart]I guess I’m a would be FTB. But I just can’t afford it anymore. A few years ago I was trying to buy a home in Mira Mesa in the 300k-400k range and constantly got outbid by investors. Now that the investors are gone, these homes are now 450k+ and out of my range. I guess I just don’t make enough money. I don’t think I’m being too picky.[/quote]

dan, there are plenty of other communities in SD County where you can still buy a SFR for $300 – $400K. MM, although convenient to high-tech jobs, isn’t the be-all and end-all of moderately-priced SFR’s in the county. You can likely get more bang for your buck in some areas of South County, East County or North County. Most of SD Metro (where MM lies) is a hard nut to crack for moderate income buyers, price-wise.

So yes, you’re being “too picky” because you have not expanded your search.

For example, I just received this “sold comp” in my e-mail this morning:

http://www.redfin.com/CA/Chula-Vista/620-Date-Ave-91910/home/5967288?utm_source=myredfin&utm_medium=email&utm_campaign=instant24_listings_update&utm_content=address&reinfo=ZXhwSWQ9MjExNzY4MyZleHBJbnN0YW5jZUlkPTE3MjkyMjE1NzY5MjEmY2F0ZWdvcnk9ZW1haWwubGlzdGluZ2FsZXJ0cyZjb2hvcnRJZD1Nb2JpbGVGaXJzdCZ0YXJnZXQ9aG9tZS5hZGRyZXNzJmxvZ2luSWQ9MTU3NjkyMQ==

It’s quite a bit bigger than the avg MM house (due to permitted room addition(s)) and is situated less than one block behind a regional mall (NOT a trafficky street) in a very safe and tidy established area. It’s also on a local bus line (to the trolley) and just 3 blocks from a bus line which goes into DT SD.

Closed yesterday for $375K.

Oh, and I forgot to add that this area runs 8-12 degrees cooler than MM about six months per year :)[/quote]

Well yeah I guess if you want to think about it that way, then yes I am picky. But I’m not holding out for granite counter tops 1900+sqft or anything like that.

Why am I being picky? I grew up in PQ and Poway, in much bigger homes than I’m looking for in Mira Mesa, and I just kinda want to stay in the area I grew up in. My parents didn’t have better work than I have now, but they were able to afford it. Dunno. I guess I’ll just wait and inherit property from them.

danthedart wrote:Well yeah I

[quote=danthedart]Well yeah I guess if you want to think about it that way, then yes I am picky. But I’m not holding out for granite counter tops 1900+sqft or anything like that.

Why am I being picky? I grew up in PQ and Poway, in much bigger homes than I’m looking for in Mira Mesa, and I just kinda want to stay in the area I grew up in. My parents didn’t have better work than I have now, but they were able to afford it. Dunno. I guess I’ll just wait and inherit property from them.[/quote]

dan, almost ZERO FTB’s are able to get the same kind of home they grew up in straight out of the gate! Was the home you grew up in PQ and Poway your parent’s first home? Or even their second home?? Do you know if they had to put in their own renovations in it over the years in order to get it like it was when you were going to HS? Or were you too young to remember just how hard they had to work (DIY?) to get it looking like it does today?

If you think you’re going to be able to “wait it out” while your kid(s) grow up in front of your eyes to “inherit” your parent’s home, more power to you, dan. Did it ever occur to you that you could likely be 55-70 years old before your last parent passes away (assuming they still live in their house)? And do you have any siblings you’ll have to “duke it out with” to decide who is able to buy out the other(s) to get title to the family home? Just wondering ….

You can’t compare your parents lives as young newlyweds/young parents to your own. IT DOESN’T MATTER WHAT THEY DID FOR A LIVING OR IF YOU THINK THEY DIDN’T HAVE BETTER “WORK” THAN YOU. If they had a 8-5 pm W-2 job in SD County, I would bet marbles to chalk that your parents had a lot more regulations at work than you do (likely had to punch a time clock?), had to do a lot more “face time” at work than you do, were not able to “telecommute” under any circumstances, obviously had no internet at work (or anywhere else for that matter), had no cell phones and may have had to work much (physically) harder than you ever had to.

I don’t think you would want to trade in your life today for theirs. Yeah, sure, they might have gotten a (rundown?) PQ or Poway house for $90 – $125K but at what interest rate? How about 10-11% (on average) for a fixed rate mortgage?

As a FTB, dan, you CANNOT EXPECT to have a move-up home or a home in a “move-up” area for your first home, unless your family income is in excess of $150K, you have very little in monthly health insurance outlay, you have no outstanding student loans and you have saved a minimum of $100K (+ closing costs) for a downpayment.

If you feel you MUST have this type of home in SD County and none of the above paragraph applies to your household, your household needs to figure out (1) how to consistently bring in more money; (2) how to save more money and save it faster; (3) and/or how you’re going to bring some heavy-duty DIY skills to the table so you can purchase a “heavy fixer” that flippers would purchase to fix and sell for a profit.

So in sum, you are too picky for your qualifications and will never be able to buy a home unless you expand your search or do the things in the preceding paragraph.

You can start by asking your parents what they had to do in order to qualify to buy their current home which you aspire to “inherit.” You might be surprised to learn of all the sacrifices that they had to make to buy it and then keep it over the long term.

bearishgurl wrote:dan, almost

[quote=bearishgurl]dan, almost ZERO FTB’s are able to get the same kind of home they grew up in straight out of the gate![/quote]I know many FTB who either bought the same kind of home they grew up in or bought bigger homes in the same area or bought in a higher end area. So, this statement is bogus.

AN wrote:bearishgurl

[quote=AN][quote=bearishgurl]dan, almost ZERO FTB’s are able to get the same kind of home they grew up in straight out of the gate![/quote]I know many FTB who either bought the same kind of home they grew up in or bought bigger homes in the same area or bought in a higher end area. So, this statement is bogus.[/quote]

Yes, it is possible if FTB’s take out a HUGE mortgage (assuming they’re qualified) as most of them have very little to put down (due to having no prior home equity to invest). I’m NOT speaking here of the FTB’s between 2004-2007 who successfully “fogged a mirror” and “got a loan.”

As to MM, yes, your statement may be true for MM as it is a “moderate to middle-income area.” Even though it may have a couple of “newer, nicer” pockets, MM is not really considered a “move-up” area.

AN, I understand that YOU bought your first house in MM (in 2008, as the market was falling?) and that you grew up there. You have to admit that your home wasn’t “perfect” when you bought it and that you yourself put numerous? improvements into it since you bought it. Was/is your first home actually bigger and “better” than the home you grew up in there?

Acc to his posts, “danthedart” is apparently only qualified to buy a home in the $325 – $375K range? and is “stuck” on Poway/PQ where an “entry-level” home which needs a lot of work is likely $475-$550K, assuming he can even find a listing like that.

You’re correct that if dan was really shopping in the 2009 to the beginning of 2012 era in MM that he should have been able to buy something in MM but probably got outbid by cash buyers looking to rent out or flip. This tells me that he didn’t have a substantial downpayment in order to compete with those cash buyers and didn’t have the qualifications (income) necessary to increase his mortgage enough to raise his bid when counter offers were made to him (if any). Therefore his income was too low to be shopping in that area under the prevailing market conditions at that time.

AN, did you buy your first home PRIOR to MM becoming a “hot” investment opportunity for cash investors? I seem to remember that you did, you took out a mortgage and it was also purchased as a “cosmetic fixer.” Am I correct?

Based upon his posts, it is entirely possible … even probable… that dan didn’t place any offers on cosmetic fixers in MM … only houses ready to immediately move into which didn’t need anything. Hence, he was trying to buy an already flipped property (to profit the flipper), as you so astutely noted.

A LOT of FTB’s today MUST have their first house “perfect” before a stick of furniture is moved in and dan was likely no exception. If there were not going to be any funds left to make it “perfect” after COE, then the listing itself had to be “move-in ready,” (which is a very subjective “condition” depending on which generation one belongs to).

Correct me if I’m wrong here, dan. I still maintain that you can find a single-family home to buy today in SD County if you really wanted to.

btw, the house in the Chula Vista link I posted here was a probate sale and had tons of deferred maintenance. Nevertheless, it recently sold for $375K … no doubt due to its excellent location and legally-permitted room addition(s).

This interesting thread

This interesting thread bolsters my long-held belief that FTB’s will no longer “settle” for homes which they can actually afford today under normal lending guidelines. If they can’t have a move-up home, or, some cases, what would be considered to be a “luxury” home (or buy a home/condo in a “move-up” or “luxury” area), then they will continue to rent.

Under no circumstances will the vast majority of SD County FTB’s buy a SFR which is suitably-sized and within their means if the area doesn’t meet their “stringent qualifications” (ironically, even the ones on a beer-budget).

Thus, there are a lot of SFR’s in moderate income areas which aren’t moving very fast right now due to the dearth of interested cash investors.

When a FTB states here that they’ve made offers recently between $325K and $450K and can’t seem to get an accepted offer, I have to wonder whether they really DID make those offers or if those offers were “lowballing” a much higher-priced listing.

Dozens of local SFR listings in this price range are out there … in dozens of zip codes. If a percentage of these listings are being “shunned” by qualified buyers, then those buyers aren’t really serious about buying a house. It’s sad, because it isn’t going to get any easier for these buyers to consummate a deal (esp FTBs) in the coming years. I don’t believe that even a bump in interest rates of 2% is going to affect today’s entry-level SFR asking prices one iota. All it will do is cause buyers to have to come up with more cash to buy the same home.

I feel this is so because many of these affected areas are just beginning to “right themselves” to ’99 to ’02 values (from a severe artificial local drop in values due to the proliferation of short-sale and REO listing sold comps in the immediate area). FTB’s should not expect prices today to be less than the ’99 – ’02 levels anywhere since full doc loans were the norm in that era. It’s not going to happen.

BG, I’m not the only FTB out

BG, I’m not the only FTB out there. As I said and let me repeat, I know many who bought in the same area where they grew up, bought bigger houses than where they grew up in the same neighborhood, or bought in better areas. So, your statement:

[quote=bearishgurl]dan, almost ZERO FTB’s are able to get the same kind of home they grew up in straight out of the gate![/quote]Is false.

[quote=bearishgurl]Yes, it is possible if FTB’s take out a HUGE mortgage (assuming they’re qualified) as most of them have very little to put down (due to having no prior home equity to invest). I’m NOT speaking here of the FTB’s between 2004-2007 who successfully “fogged a mirror” and “got a loan.”[/quote]Neither was I.

[quote=bearishgurl]Was/is your first home actually bigger and “better” than the home you grew up in there?[/quote]Yes, by a wide margin.

[quote=bearishgurl]Acc to his posts, “danthedart” is apparently only qualified to buy a home in the $325 – $375K range? and is “stuck” on Poway/PQ where an “entry-level” home which needs a lot of work is likely $475-$550K, assuming he can even find a listing like that.[/quote]He said $300-400k and he was looking in MM.

[quote=bearishgurl]AN, did you buy your first home PRIOR to MM becoming a “hot” investment opportunity for cash investors?[/quote]Nope, MM was hot back then too.

[quote=bearishgurl]I seem to remember that you did, you took out a mortgage and it was also purchased as a “cosmetic fixer.” Am I correct?[/quote]Nope, it was livable. I just have higher end tastes.

If my comment was “false,”

If my comment was “false,” then your “FTB acquaintances” who bought “better” houses than their parents were able to because they:

used a LOT of OPM to do so (had a superconforming or jumbo mtg); and/or,

were given a “gift” by parents or grandparents for a substantial downpayment; and/or,

were virtually given their home by parents or grandparents who bought it themselves, either recently (and deeded it to them at COE) OR many years ago and deeded it to them recently; and/or,

used an inheritance or trust-fund corpus to fund their downpayments or entire home purchase; and/or,

lived in their parents’ low-value home with their moderate-income or poor family of origin while growing up until they started their own careers and began making good enough money to buy a better home.

THE REASONS BEING that the vast majority of 20/early 30-something FTBs (Gen Y) haven’t had enough time to save a 20% downpayment to buy a “better” or “luxury” home.

Which category do you fall in, AN? (just wondering)

bearishgurl wrote:If my

[quote=bearishgurl]If my comment was “false,” then your “FTB acquaintances” who bought “better” houses than their parents were able to because they:

used a LOT of OPM to do so (had a superconforming or jumbo mtg); and/or,

were given a “gift” by parents or grandparents for a substantial downpayment; and/or,

were virtually given their home by parents or grandparents who bought it themselves, either recently (and deeded it to them at COE) OR many years ago and deeded it to them recently; and/or,

used an inheritance or trust-fund corpus to fund their downpayments or entire home purchase; and/or,

lived in their parents’ low-value home with their moderate-income or poor family of origin while growing up until they started their own careers and began making good enough money to buy a better home.

THE REASONS BEING that the vast majority of 20/early 30-something FTBs (Gen Y) haven’t had enough time to save a 20% downpayment to buy a “better” or “luxury” home.

Which category do you fall in, AN? (just wondering)[/quote] who cares how FTB get their downpayment. The fact is, your statement about almost zero FTB can’t afford to buy in where they grew up is false.

You miss one scenario. Make money, live frugal and save for the down payment. Grew up in modest neighborhood.

AN wrote:bearishgurl wrote:If

[quote=AN][quote=bearishgurl]If my comment was “false,” then your “FTB acquaintances” who bought “better” houses than their parents were able to because they:

used a LOT of OPM to do so (had a superconforming or jumbo mtg); and/or,

were given a “gift” by parents or grandparents for a substantial downpayment; and/or,

were virtually given their home by parents or grandparents who bought it themselves, either recently (and deeded it to them at COE) OR many years ago and deeded it to them recently; and/or,

used an inheritance or trust-fund corpus to fund their downpayments or entire home purchase; and/or,

lived in their parents’ low-value home with their moderate-income or poor family of origin while growing up until they started their own careers and began making good enough money to buy a better home.

THE REASONS BEING that the vast majority of 20/early 30-something FTBs (Gen Y) haven’t had enough time to save a 20% downpayment to buy a “better” or “luxury” home.

Which category do you fall in, AN? (just wondering)[/quote] who cares how FTB get their downpayment. The fact is, your statement about almost zero FTB can’t afford to buy in where they grew up is false.

You miss one scenario. Make money, live frugal and save for the down payment. Grew up in modest neighborhood.[/quote]

My statement wasn’t false because the FTBs themselves couldn’t afford to buy the “move-up” properties they did (or even a “starter home” in many instances). They did so by having a(n older) relative provide all or most of the downpayment or buy it outright for them. How do I know this? I’ve heard many times from my own brethren (and older) why they feel compelled to do this, “I can’t bear to see my grand child(ren) have to move again in the middle of the school year to get out from another rent hike.” AND, “My grandchild(ren) moved four times last year. Never, ever, again, if I can help it.”

I know that “one scenario” is you, AN, and it’s not the norm, so yes, I did miss it. You’ve posted here many times here that you grew up in MM and are/were able to live modestly. Most of MM is a “modest area” and not too pricey. I’m happy for you that you were able to get a house close to your family. You seem practical and didn’t purchase a ridiculously-priced mcmansion or cheaply-built zero-lot-line monstrosity with HOA/MR like so many of your compadres seem to “aspire to” and so that in and of itself makes you a “Gen-Y Outlier.” For this, you have much more freedom in life and in my book, that’s worth a lot 🙂

Give it a rest!!!!! The

Give it a rest!!!!! The sniping here is quite childish.

Some June stats are

Some June stats are available:

http://sandicor.com/resources/sales-statistics-2010-2014/

No resale/new breakdown, but the trend there shows continued rise in months of inventory.