Last month I introduced a chart of the year-over-year price change,

and I belatedly realized that I should have included an inflation

adjustment. That is after all the more relevant figure — if your

house’s price went up 1%, but inflation rose by 2%, your house is

now worth less than it was in purchasing power terms, which what

actually matters.

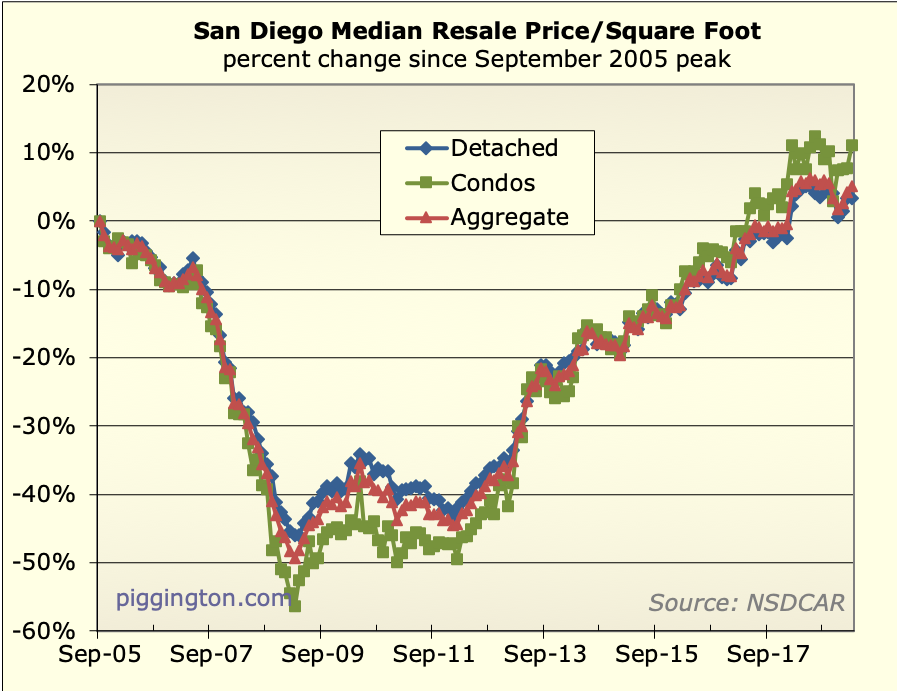

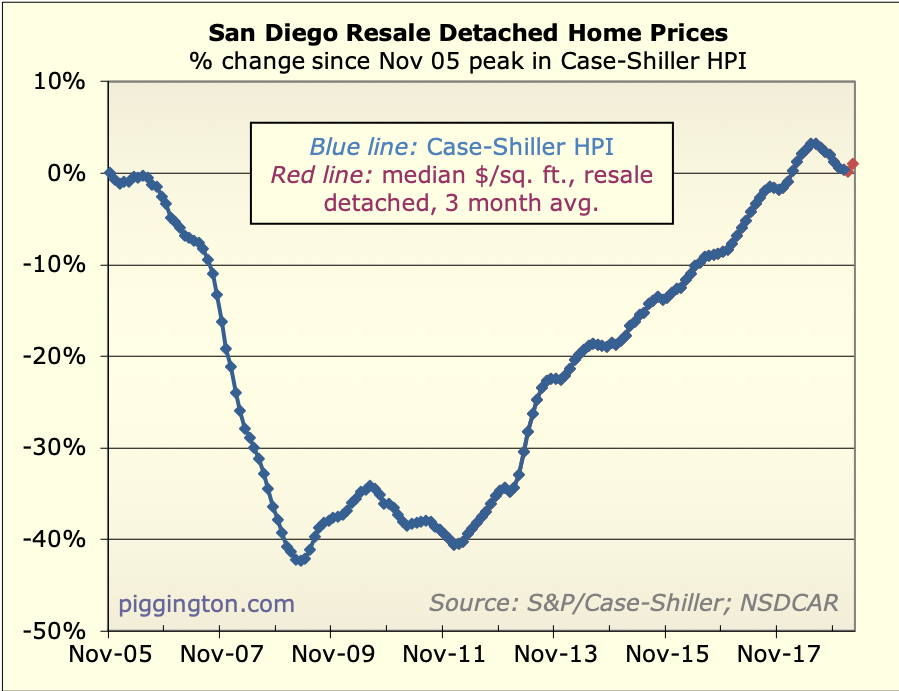

And on that note, the real “home price” (actually 3-month average of

the single family price per square foot) did indeed go

ever-so-slightly negative last month. This marks the first time in

negative territory since 2012:

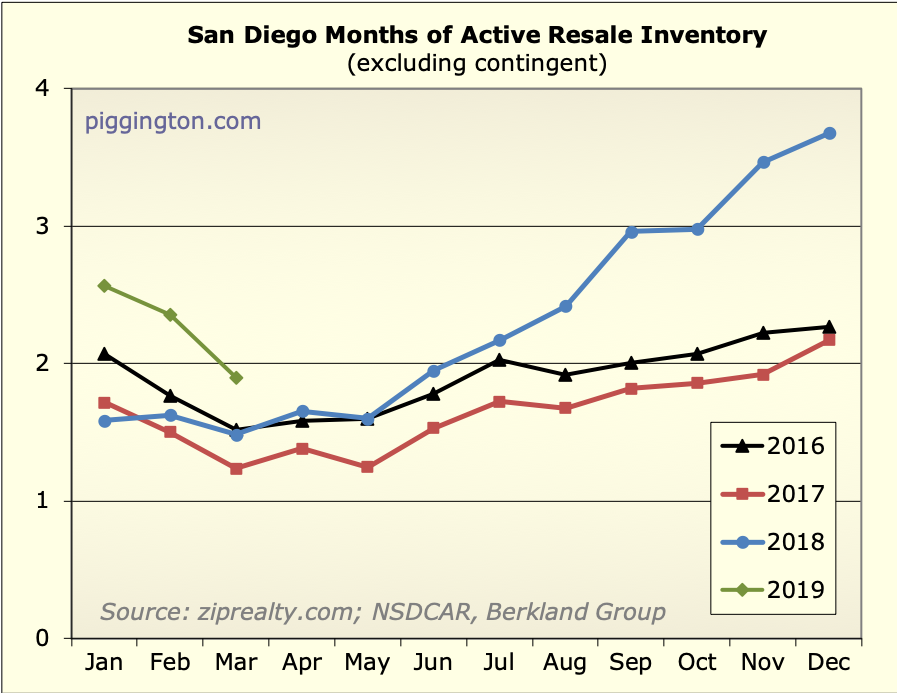

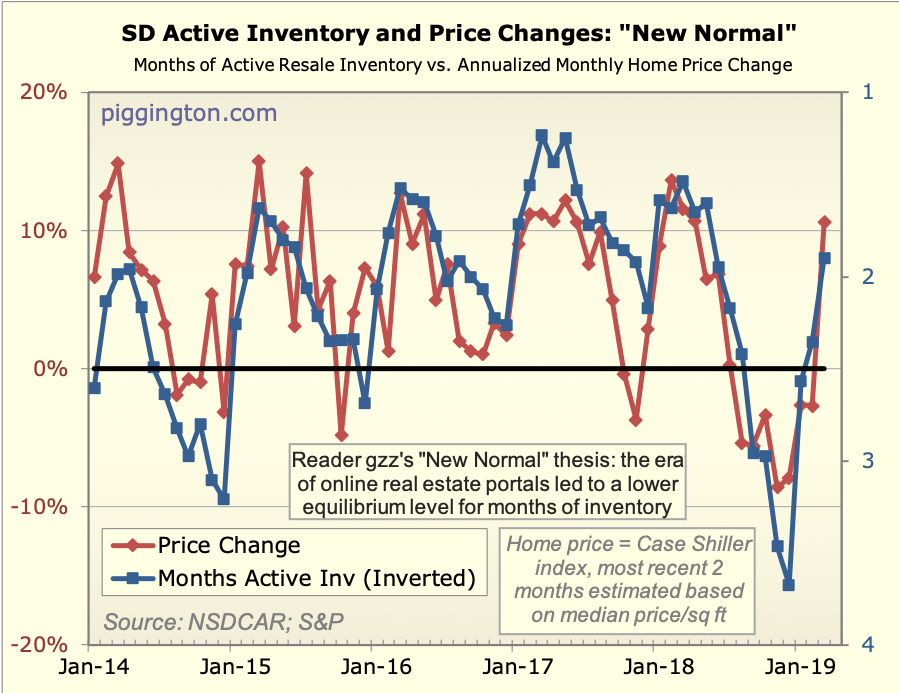

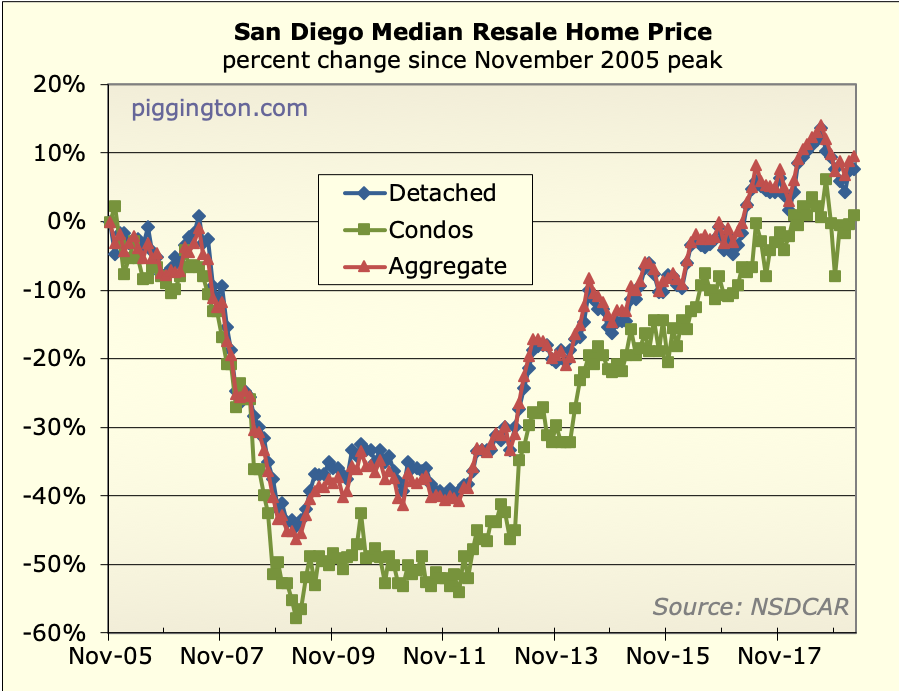

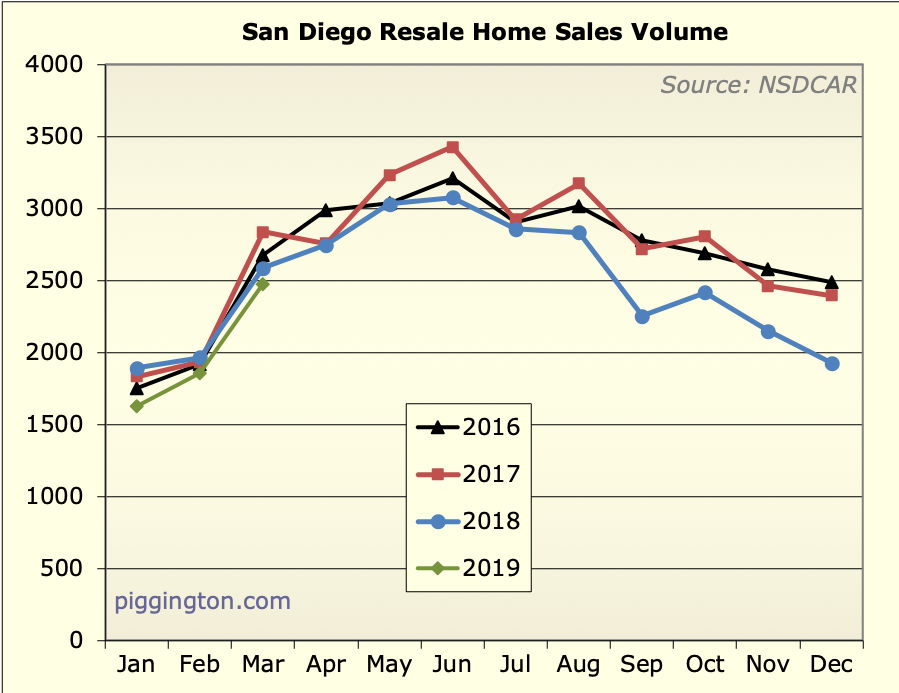

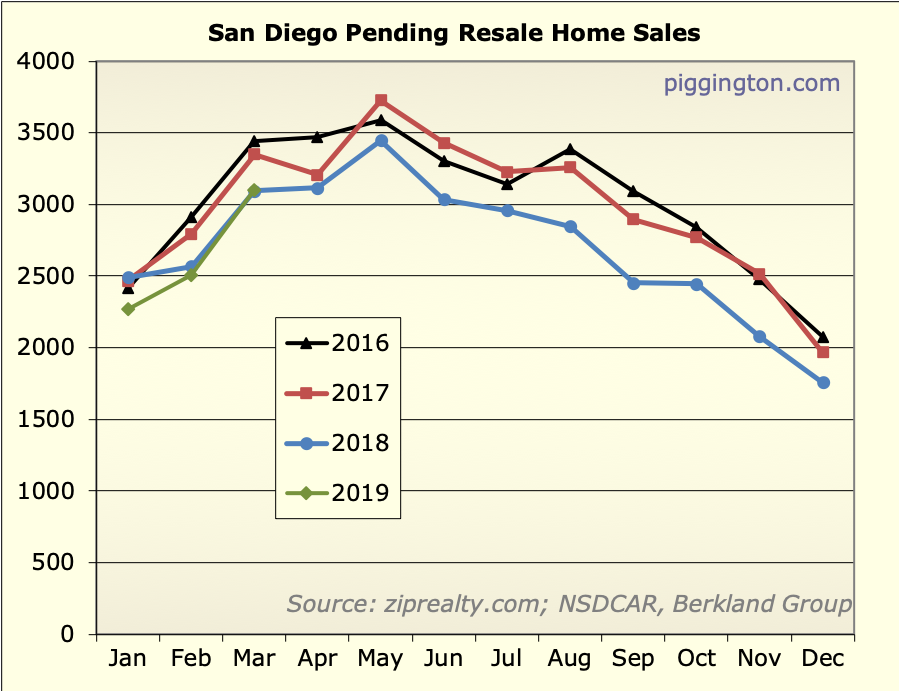

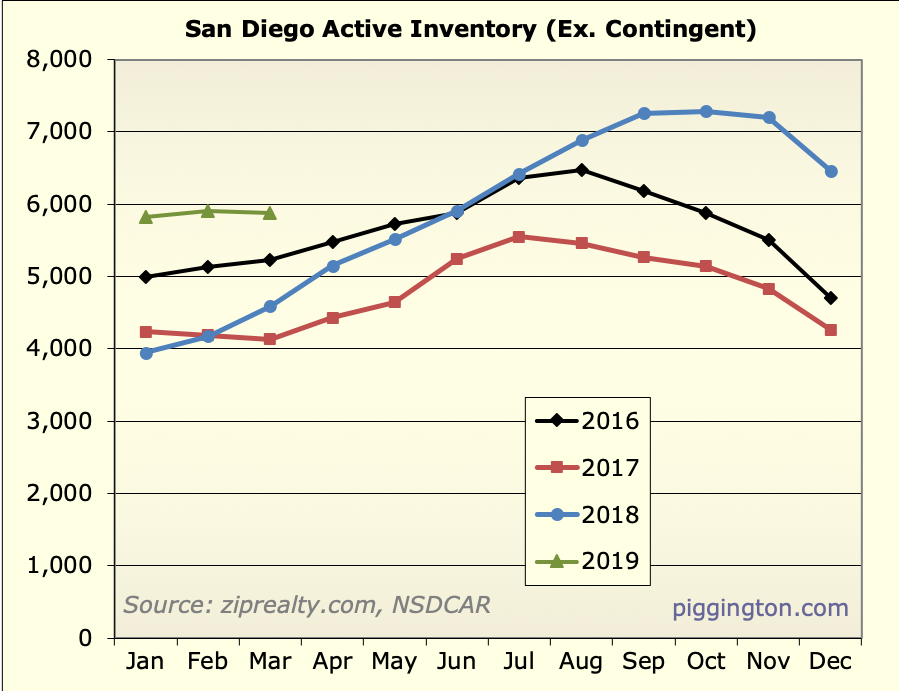

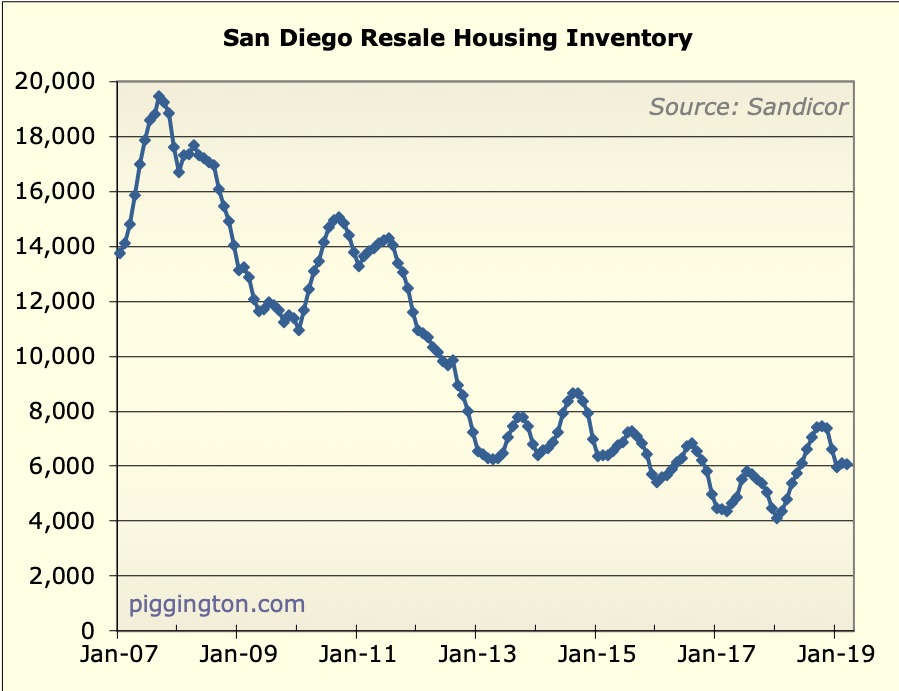

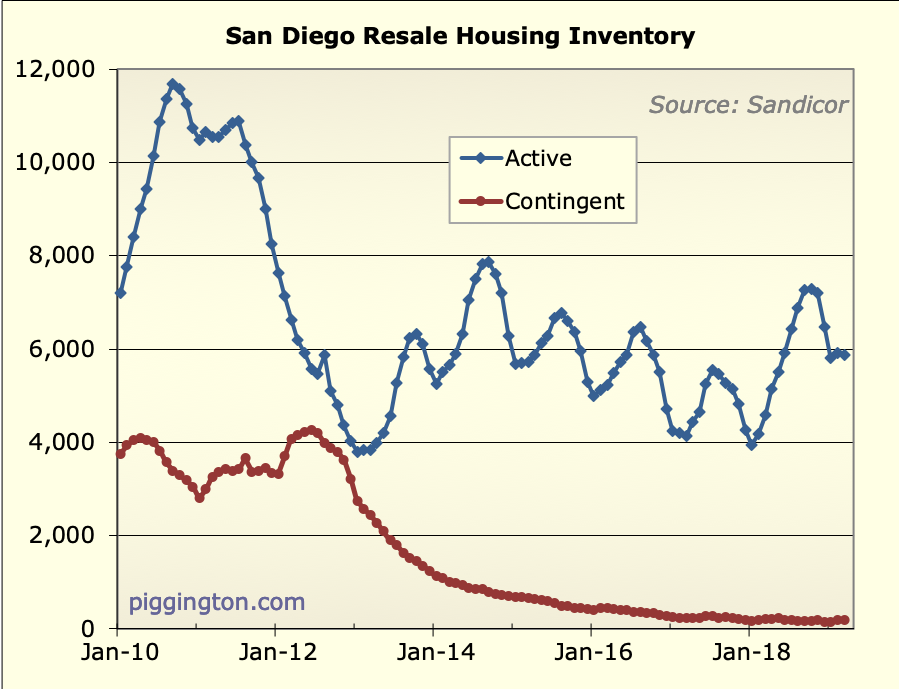

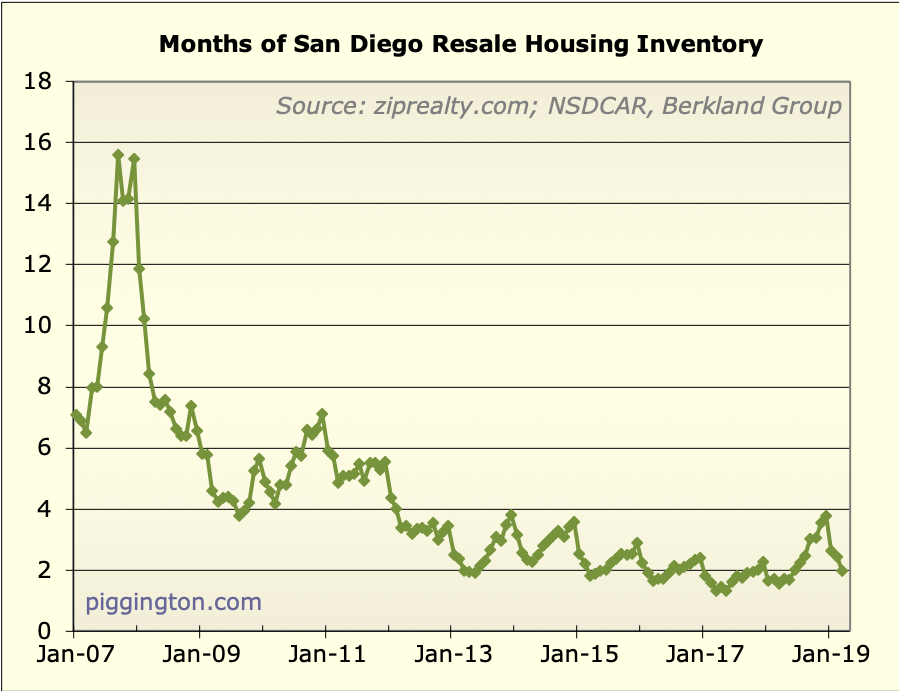

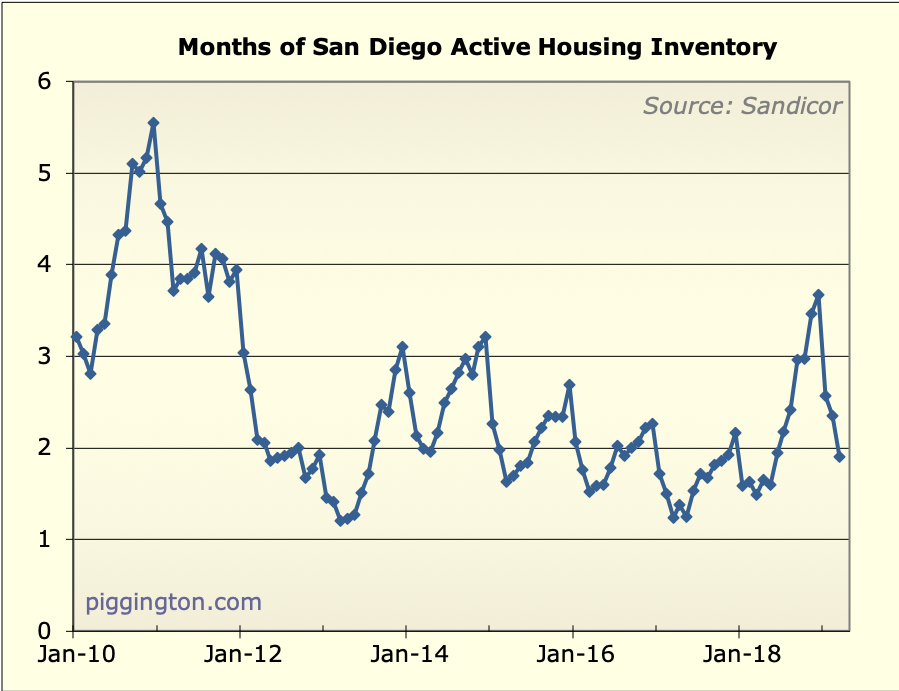

Weep not for the market, though, as it has shown some resilience of

late, with months of inventory declining:

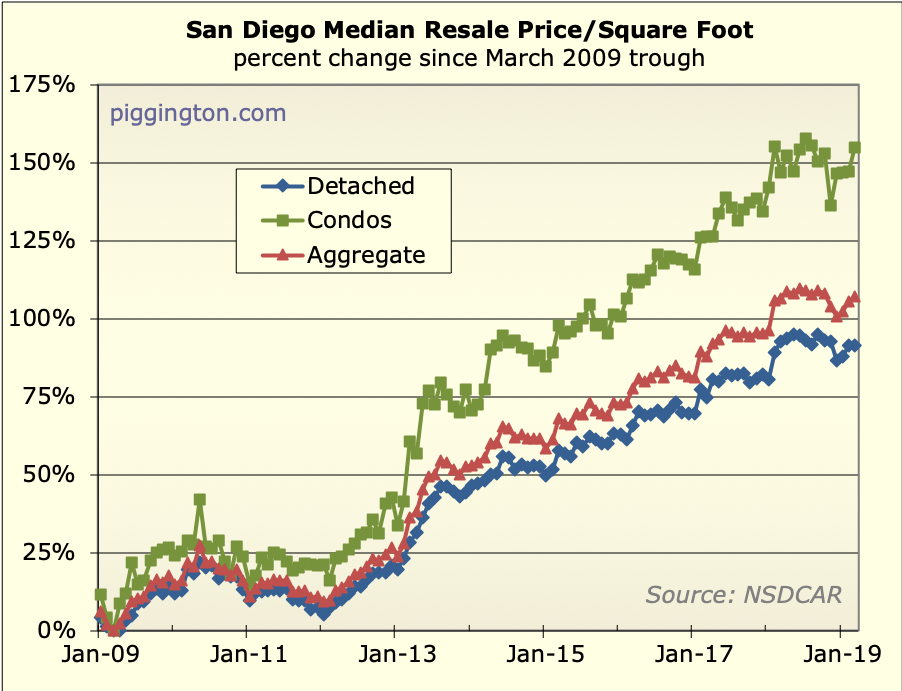

… and prices bouncing a bit:

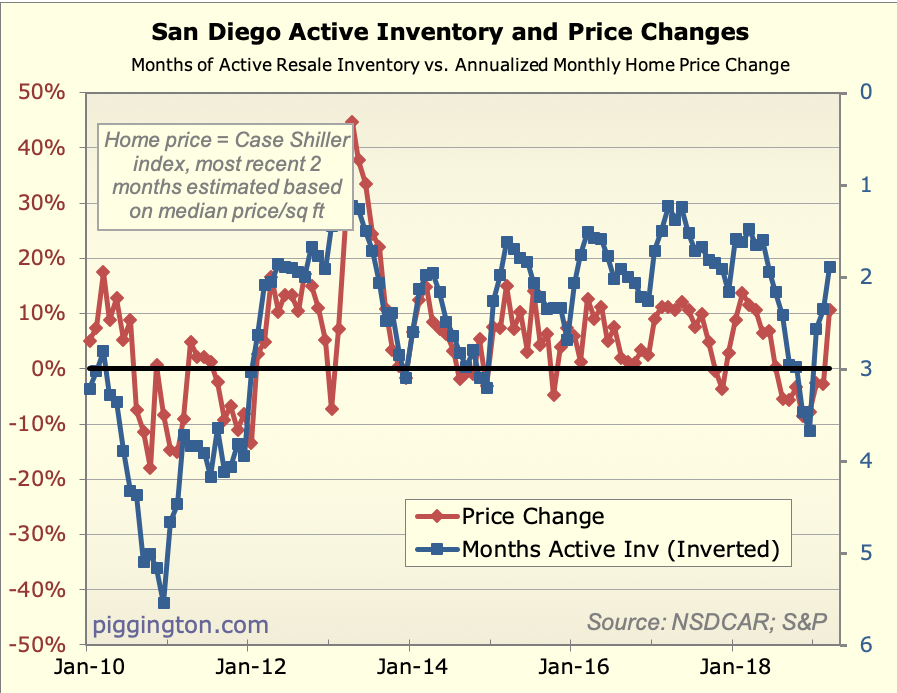

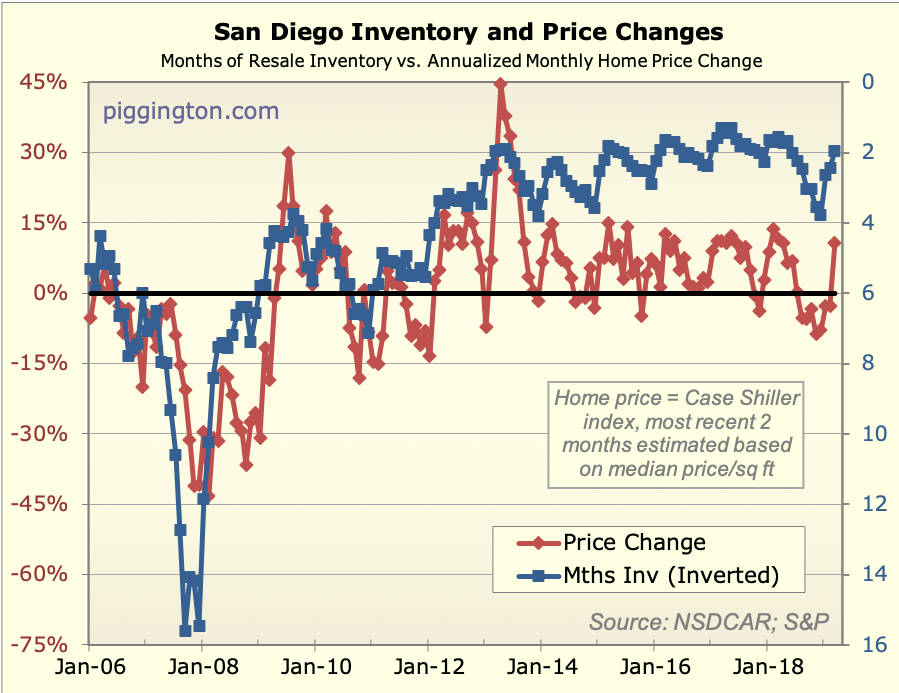

Here are price changes and (inverted) months of inventory

overlaid… it’s amazing how well this relationship has held up,

including during the recent pretty violent plunge and snapback (only

some of which was seasonal):

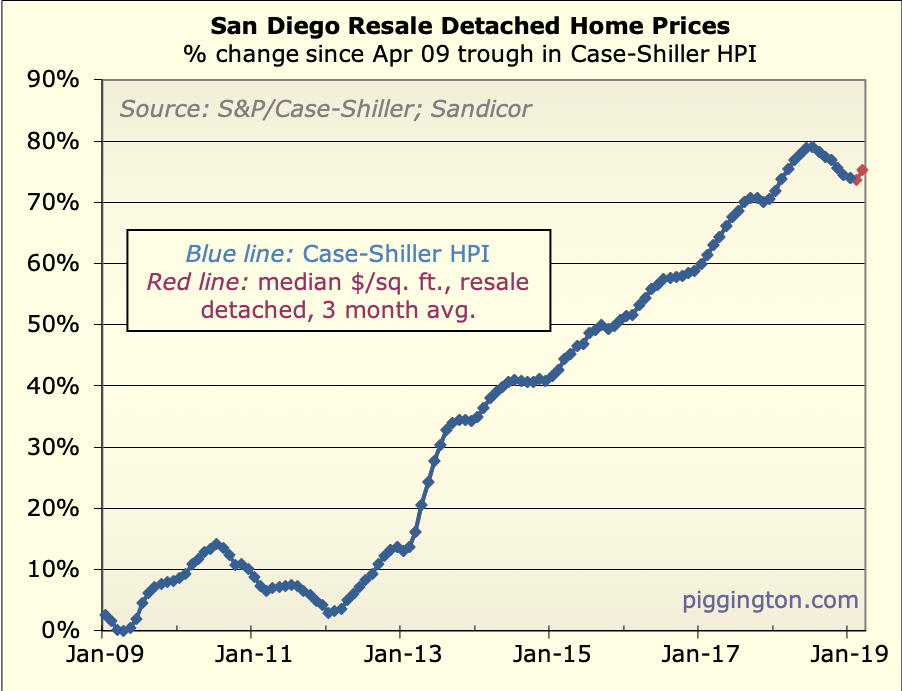

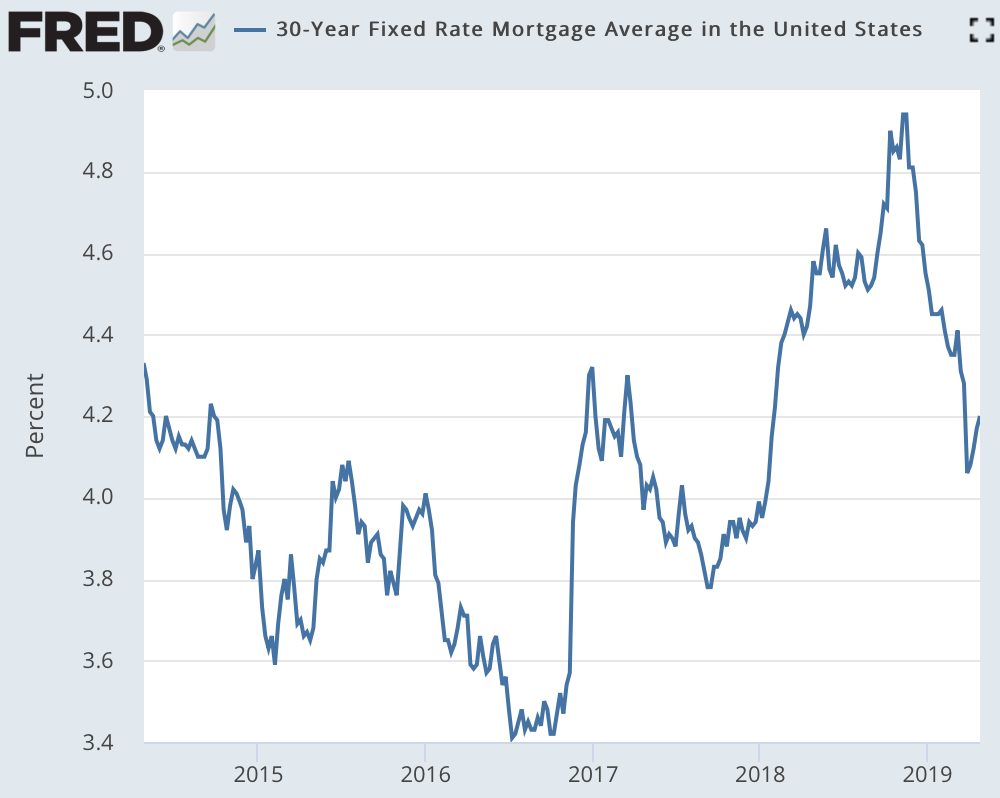

I think it’s likely that the recovery is largely owed to the plunge

in mortgage rates:

My brief defense of this is pretty straightforward: rates went up

hard and fast into late 2018, and the market weakened notably

(becoming the weakest since the boom began). Then rates dropped and

housing started to bounce back. Like I said, pretty straightforward!

The problem for the housing bulls is that rates dropped so hard

because people downgraded their forecast for economic growth. A weak

economy is not in itself good for housing, obviously. But a strong

economy would likely see a resumption of Fed tightening and higher

rates. So this current housing mini-rebound seems to require a very

delicate balance that is unlikely, in my opinion, to persist

for too long. But we’ll see.

More graphs below…

Nice graphs. thanks Rich!

Nice graphs. thanks Rich!

Thanks for adding the

Thanks for adding the mortgage rate chart with this post. For the last couple of years I’ve been thinking the market is on pretty solid footing, but the way a less than 1% increase in mortgage rates slowed the market in late 2018 leads me to wonder if the market isn’t more fragile than I think. Does it seem to others that the market is more sensitive to interest rates than it used to be?

Yes, I think the market is

Yes, I think the market is probably unusually sensitive to rates. With valuations (price to rent/income), buying only pencils out if rates are low. It makes intuitive sense, and I think the past year bears it out (rates went up and the market weakened; then rates went down and the market started to bounce back).

The good news for housing bulls is that while valuations are high, they are “rationally” so, in that low rates have made purchasing a reasonable decision from a cash flow standpoint. (As opposed to the mid-2000s, when valuations were pushed up by euphoric sentiment and unrealistic expectations of future price gains).

The bad news is that the whole thing really depends on rates staying low. Which gets back to your observation and my agreement that yes, the market is unusually sensitive to rate changes.

The less bad news is: while it won’t be great for the market if rates go up, we aren’t looking at a mid-2000s-like situation. It could be that valuations have to drift down to accommodate higher rates (which could happen simply by prices flattening for a sufficiently long time, as incomes/rents catch up). But that’s very different from a speculative bubble which must burst when the edifice of nutty expectations on which it was built finally comes crashing down.

(edited to fix a couple typos)

Unemployment hits 3.6%, 49.5

Unemployment hits 3.6%, 49.5 year low:

https://mobile.reuters.com/article/idUSKCN1S9075

More jobs, more economic growth, higher rents, higher real estate prices.

Are mortgage rates actually low or do they have room to fall?

Adjusted for inflation 30 years are about 2-2.5%.

There are lots of different means US rates could converge toward.

One is relative to other countries. Currently US 10 year is higher than Israel, Canada, Cyprus, New Zealand, Australia, Ireland, and Spain. That’s basically unprecedented. So is our rates being MUCH higher than France, Netherlands, and Belgium.

I am not so much arguing for lower rates as saying there is equal uncertainty in both directions, and high nominal rates in the 1980s and 1990s are pretty irrelevant to the coming 2020s.

In general, if you want a positive return after inflation, plus currency stability, and the legal stability and protections of a developed Western system, the USA, Canada, and Australia are your only bets. Japan, South Korea, Taiwan, and Europe are zero growth and have shrinking labor forces. BRICs have a lot of unique risks. Net capital flows I believe will favor the USA more and more, push our rates toward developed world means, not our current rates which are akin to developing nations like Thailand and Morocco.

gzz wrote: More jobs, more

[quote=gzz] More jobs, more economic growth, higher rents, higher real estate prices.

[/quote]

I don’t think you can in all fairness make this blanket statement. While we have seen more jobs and economic growth, we haven’t seen much increase in wages, which means higher rents and higher real estate prices are not a foregone conclusion. Higher rents and real estate prices might still happen (due to limited supply or lower interest rates) but it isn’t a clear logical step as you imply.

The rest of your post I don’t disagree with and you raise some great questions.

Labor force size has

Labor force size has decreased by 740,000 people since December of 2018, when it peaked in size. It’s been steadily decreasing for four months, in fact. 3.6% doesn’t look as good as you’d think considering this fact.

spdrun wrote:Labor force size

[quote=spdrun]Labor force size has decreased by 740,000 people since December of 2018, when it peaked in size. It’s been steadily decreasing for four months, in fact. 3.6% doesn’t look as good as you’d think considering this fact.[/quote]

ever considering bigger picture of the “Civilian labor force participation rate” which is down over decades,…

https://www.bls.gov/charts/employment-situation/civilian-labor-force-participation-rate.htm

combined w/ other stuff like the fact that don’t think the fed understands the euro-dollar funny business (i.e. “credit” created outside the USA pumps $$$ into the global system),… make me wonder how much longer the market(s) can stay irrational,… things could stay rosy for those w/ access to capital for awhile longer, but eventually the tab has to be reconciled

gzz wrote:

I am not so much

[quote=gzz]

I am not so much arguing for lower rates as saying there is equal uncertainty in both directions

[/quote]

Rates are just about the lowest they’ve been in recorded history. So I think it’s pretty bold (to put it mildly) to claim that there is equal uncertainty in both directions.

PS this is where I got that

PS this is where I got that stat:

https://www.bloomberg.com/news/audio/2018-08-16/richard-sylla-on-the-lowest-interest-rates-in-history-podcast

‘Sylla is the author or co-author of several books, including “A History of Interest Rates.” He notes that rates in recent years are “the lowest in history, from the Code of Hammurabi to Babylon Civilization, Greek and Roman Civilization, the Middle Ages, Renaissance, right up until the present.”‘