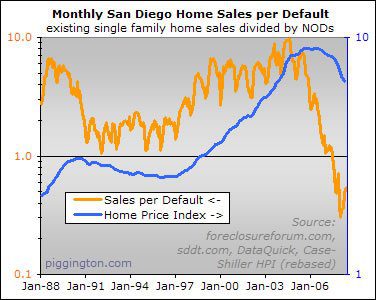

Better late than never? Maybe? Hey, I can’t help it if the GSEs go tango-uniform before I get a chance to do the monthly foreclosure charts. Here they are:

Better late than never? Maybe? Hey, I can’t help it if the GSEs go tango-uniform before I get a chance to do the monthly foreclosure charts. Here they are:

Rich,

Regarding the aging

Rich,

Regarding the aging data, at what point to items in default fall off that chart? Like are they still there when they shift to NOT status or to REO?

Also are sales calculated strictly or do they count all trustee conveyances?

It isn’t items in default —

It isn’t items in default — it’s notices of default. IE a property shows up for that single month when it gets its notice and that’s it.

Sales are dataquick resales (ie actual sales).

rich

At the risk of sounding

At the risk of sounding optimistic (I’m really not), I notice that the Sales/Default ratio has been an early predictor of price reversals, both up and down. And the last 1 -2 months are positive.

Way too early to conclude anything though. Have been false starts previously. But if we get another one or two months like this…

The key question, in my mind

The key question, in my mind is are we going to get a significant second leg down to this thing. By significant, I mean a second leg that matches or exceeds the first leg down. In terms of answering this question, I am more interested in watching the interest rates and the employment data. The feds have already lost “control” of interest rates from a consumer point of view. If this disparity widens, I wouldn’t be surprised to see double digit rates ala 1970’s. If this happens, and the employment rate in San Diego turns decidedly negative and extends beyond the housing and associated markets, prices will fall significantly further. If not, we may see a flatlining effect.

zerospeed you nailed it

zerospeed you nailed it exactly. If I may add, we also need to consider the upcoming resets in 09-12. I know of MANY a homeowner who have no plan of action to cope with the 5 year IO loan that they have that will indeed reset at this time. My bet is there will be a socialized solution that will be added to the taxpayers bill to bail these types out.

So far the unemployment and high interest rate alligators have been held off. We will see how that unfolds. While the fed has lost controls of interest rates it really has not showed up in mortgage rates yet. Rates of high 6’s and low 7’s are by no means historical but… we sure are getting there. Also what used to be a spread of about 1.25 between the 10 year treasury and a 30 year fixed mortgage just a year ago is now almost double! That is definitely problematic. So yes I could not agree with your post more.

So is the flattening NOD

So is the flattening NOD curve a sign of stabilization, or are the banks just overwhelmed?

WaitingToExhale wrote:So is

[quote=WaitingToExhale]So is the flattening NOD curve a sign of stabilization, or are the banks just overwhelmed?[/quote]

That’s the big question.

With 121,341 loan defaults in CA last quarter I find it very hard to believe all of those will be on the market within 6 or even 9 months. Same for the 63,061 homes that went to foreclosure.

With rising rates, tighter standards, and now this short-sighted ludicrous GSE bailout prices will stay higher (for a while) and people waiting to jump in will probably have to wait longer, adding to the inventory glut.

The only thing that might falsely appear good is loan reworks form this bill, but that in a growing % of the cases only delays foreclsoure.

Most people who bought during the bubble don’t even want to “own” a house worth less than their mortgage.

Any theories about the

Any theories about the uptick?

Did we ever get to the bottom of the ‘shadow inventory’ question?

Also, reading about WFC the other day and they made some accounting adjustment that reduced the number of bad loans on their books, increased stated earnings. Explanation was to give troubled borrowers more time to work things out.

Any insights here?

SD_R, any idea what that

SD_R, any idea what that socialized bailout might be? I am wondering what such a bailout might look like. There are only two things I can see actually working to bail these FB’s out. Either they allow judges to cram down morgages, cutting principal and fixing the unbelievabley low interest rates, or they buy them up through the GSE’s (or some other gov entity) and modify down at tax payers expense. I suppose they could run the inflation presses and ruin the dollar, but that wont necessarly mean wage inflation, and may backfire the way high gas and food prices are killing any stimulative effects they try right now. Any other ways they could try to F*^$ the situtation up?