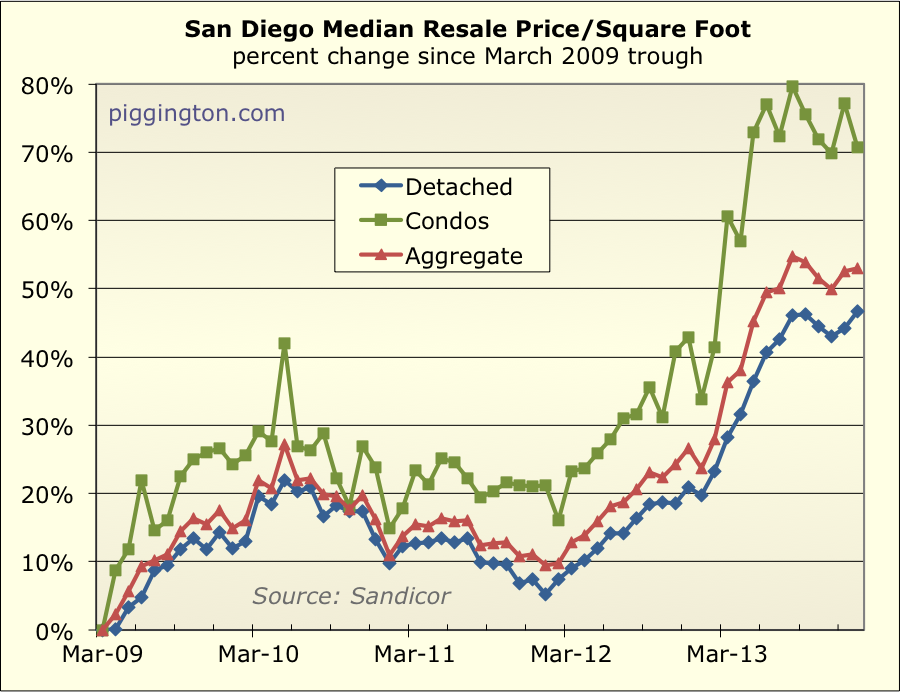

So much for that price pullback. The median price per square foot

for single family homes rose in January, just hitting a new

post-crash high:

The always wild condo median price per square foot was actually down

for the month, but prices rose in aggregate.

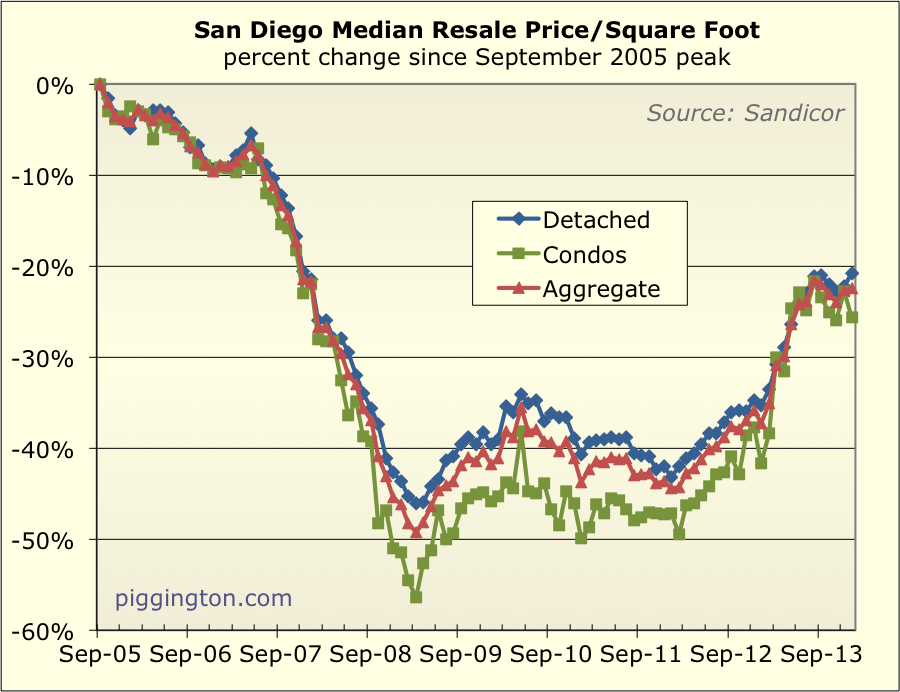

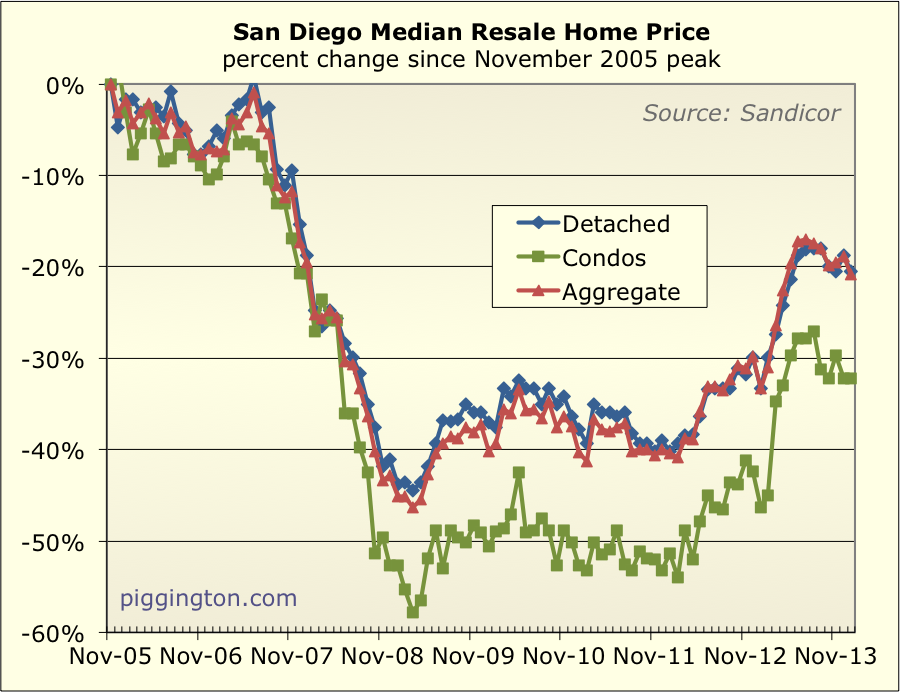

Here’s a look from the peak:

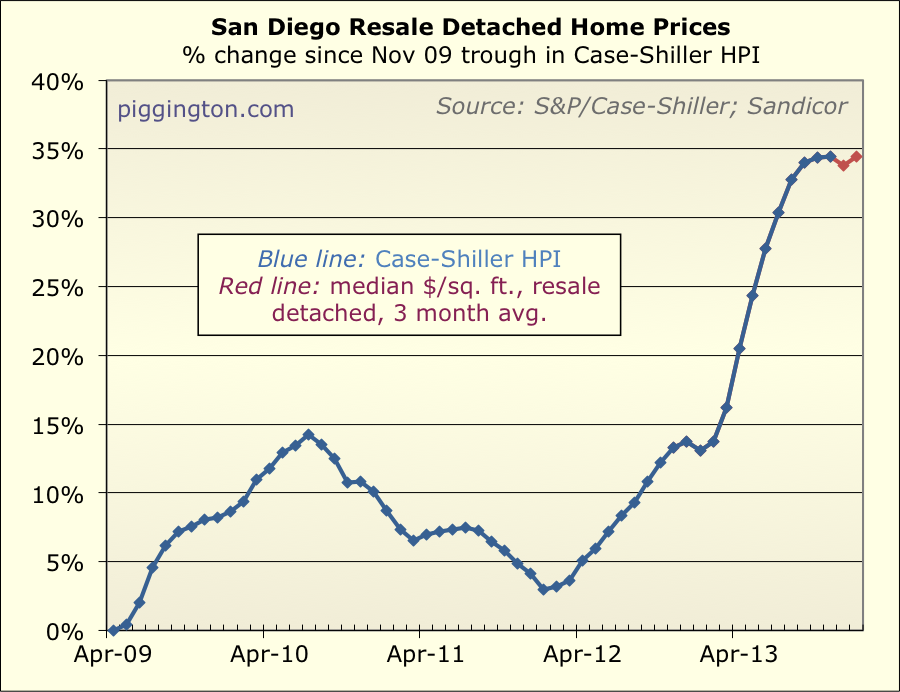

Here’s the CS Index with the past two months estimated based on the

price/square foot:

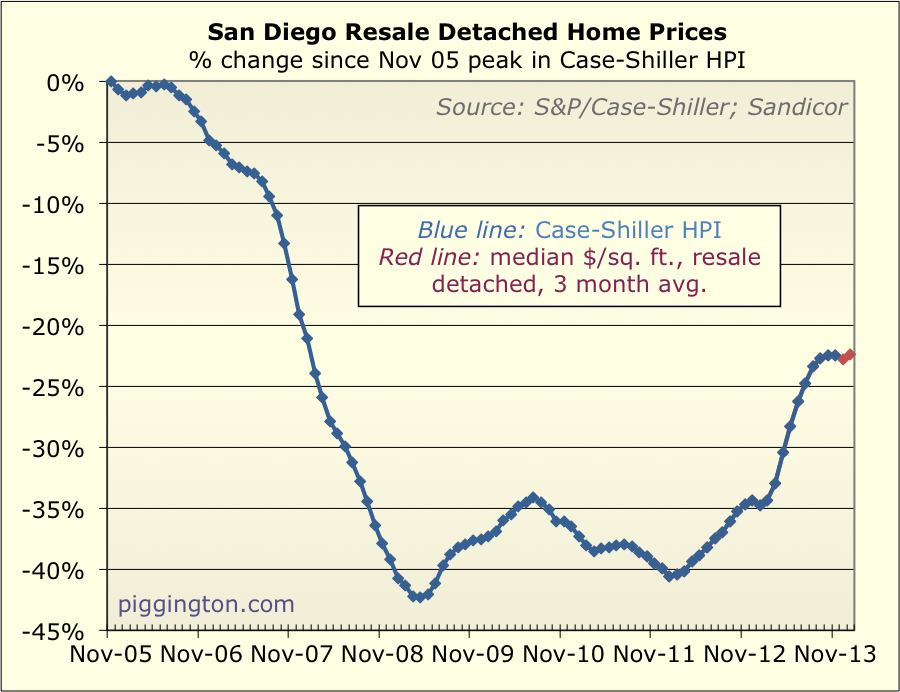

Same thing from the peak:

The median sale price (not per square foot) has actually been

declining for both property types for several months:

This is actually interesting. It looks like the median price

pretty much topped out before rates went up, and has been in a

downtrend since. However, the median price per square foot has

been flat to up, meaning that people sacrificing quality and getting

smaller homes.

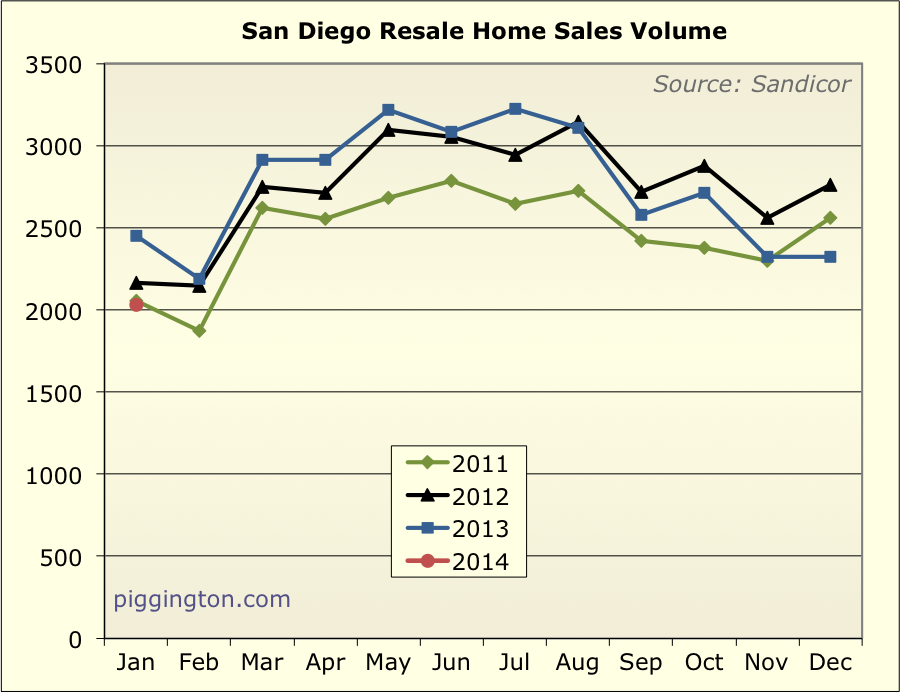

For the supply and demand stuff, I like to compare to the same month

in prior years, as there is a big seasonal impact. This is

especially important in December and January, as things usually get

thrown off due to the holidays. So on the charts below, note

January’s red dot, and compare to Januarys over the past 3 years.

Starting with sales — they were down 17% from last year, and back

to about their 2011 levels. This is a pretty significant

decline from this month last year. And unlike the recent spate

of disappointing US economic reports, this can’t be blamed on the

weather!

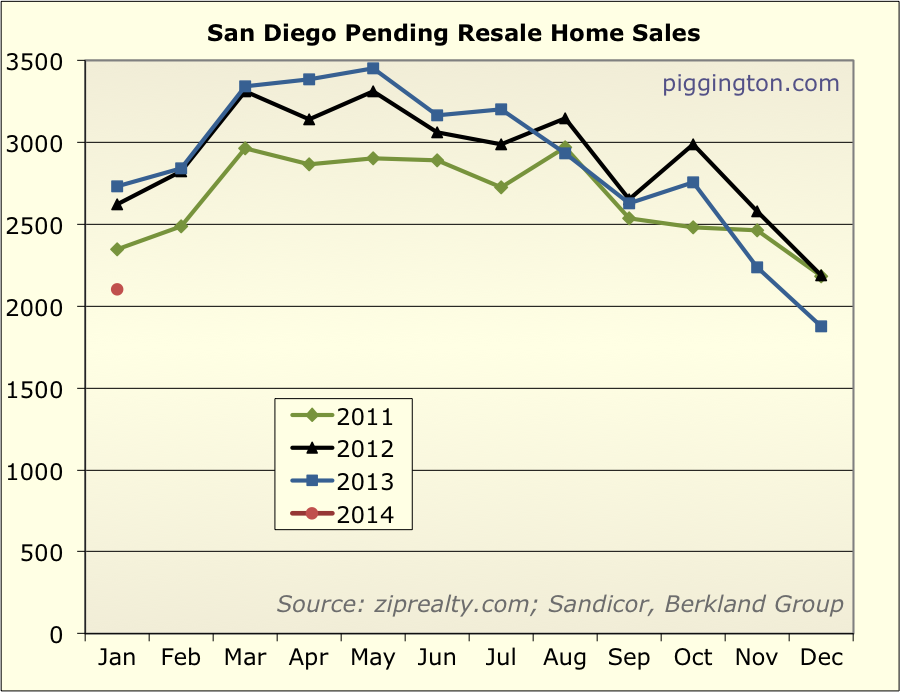

Pending were even weaker… worse than any January of the past 3

years, and 23% below last January’s level:

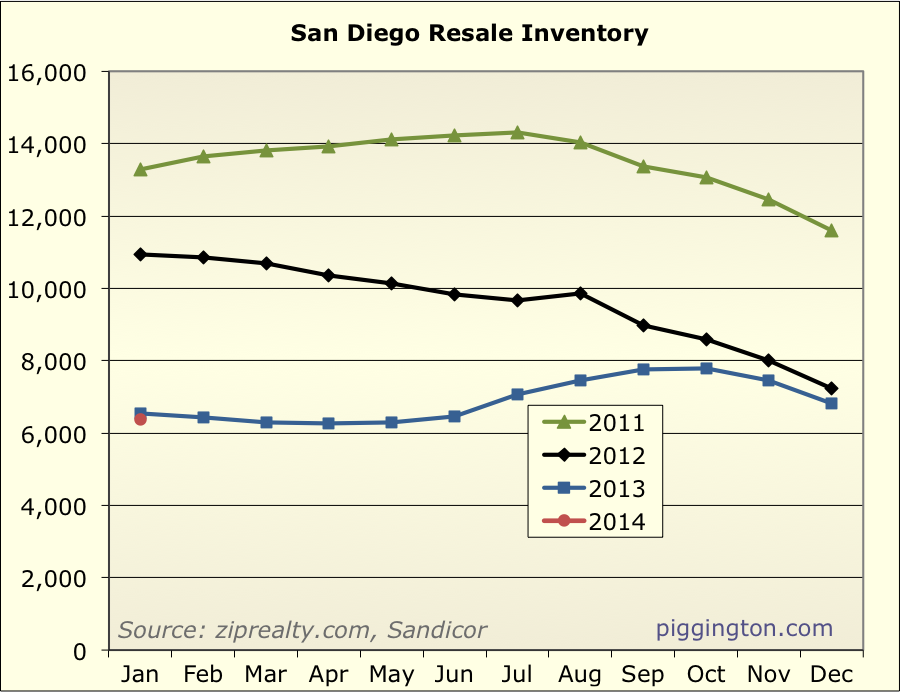

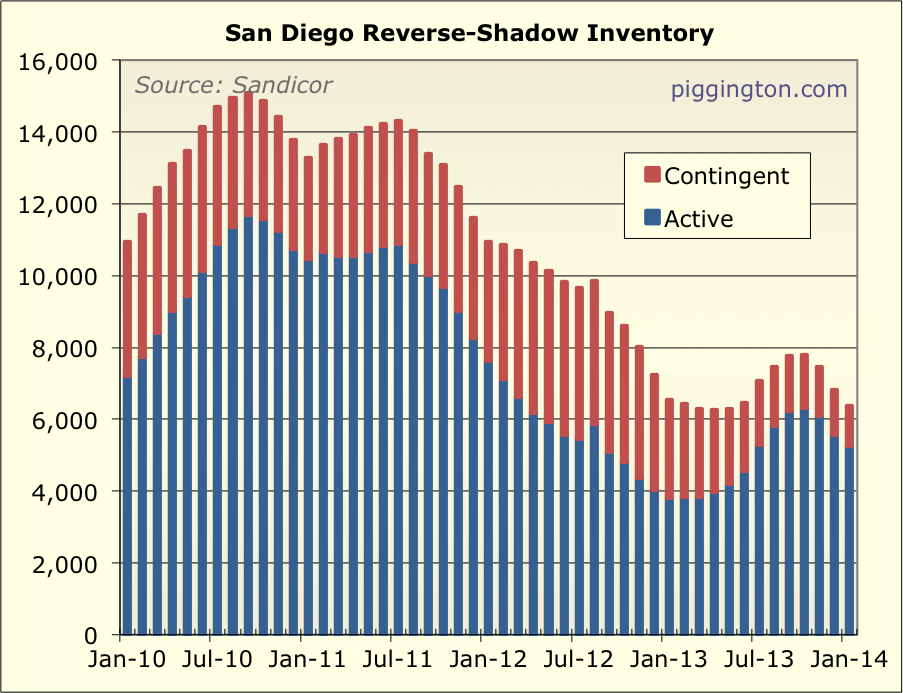

Inventory remains low:

However, the decline in inventory is entirely in the “contingent”

category. Contingent properties are usually bank-owned homes

that have an offer pending approval from the lender that owns the

property. Thus, they aren’t inventory in the typical sense, as

they are already “spoken for.” They were a pretty huge part of

inventory for a while, as the below graph shows, but as the short

sales and foreclosures have subsided, they’ve been shrinking fast:

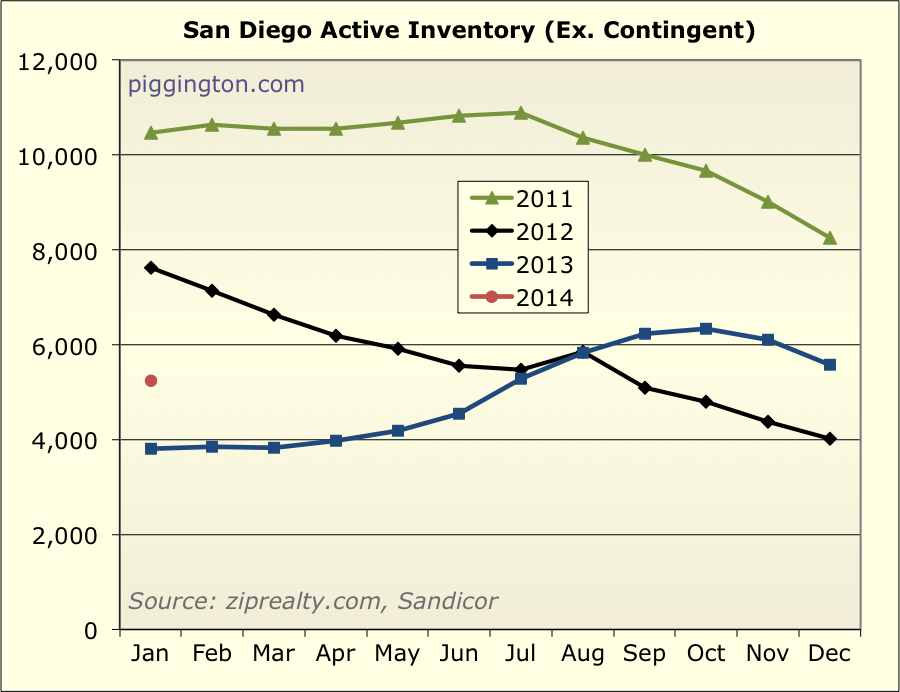

Here is just the active inventory, with contingent properties

removed. There is actually 38% more active inventory than

there was a year ago — coming off a low base, to be sure, but a

significant jump:

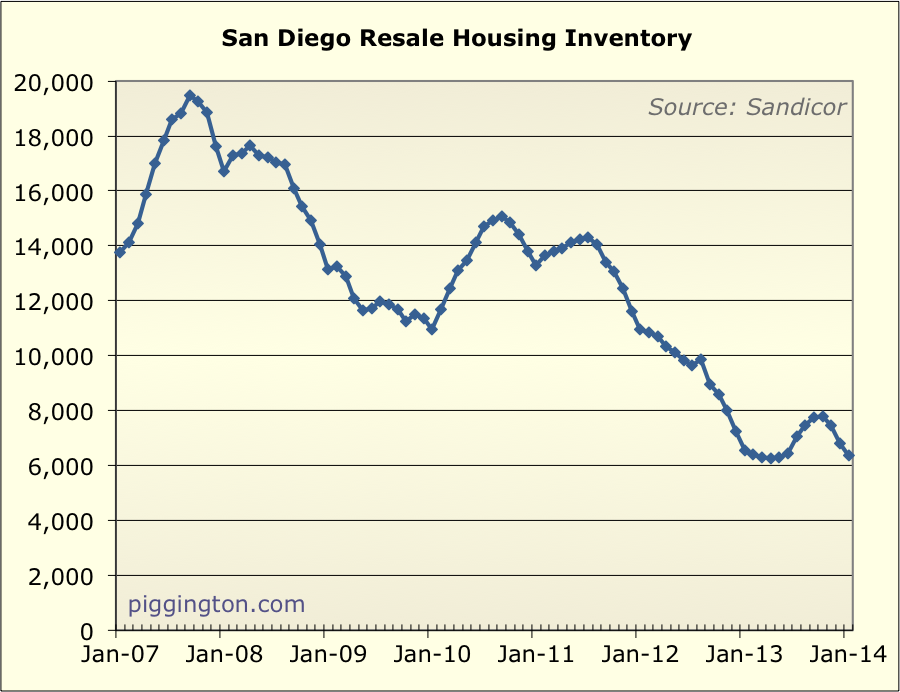

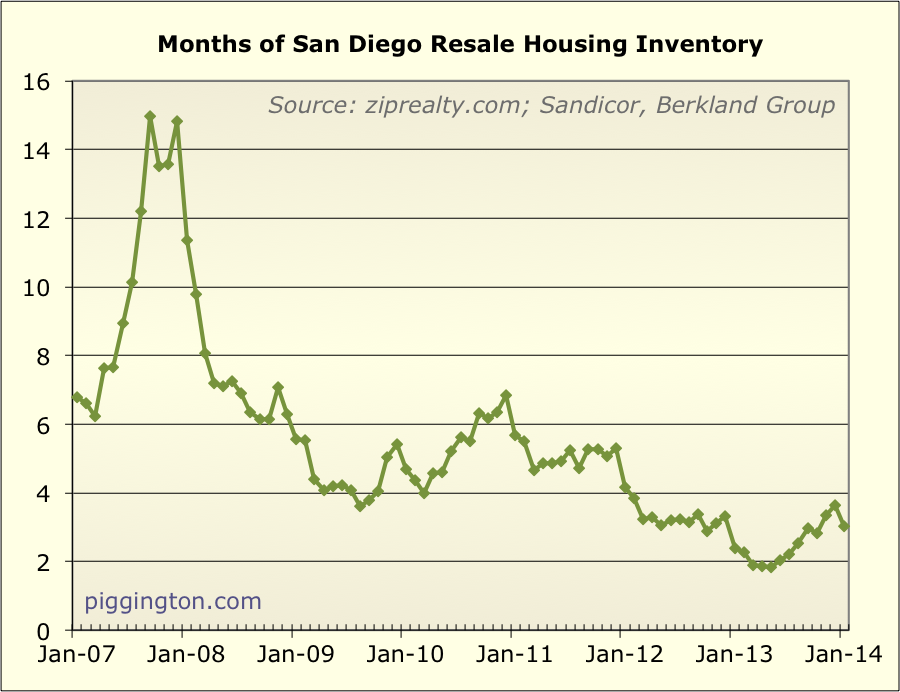

Here’s a linear look at inventory (active and contingent) going back

to 2007. Unfortunately I don’t have an active series going

back that far.

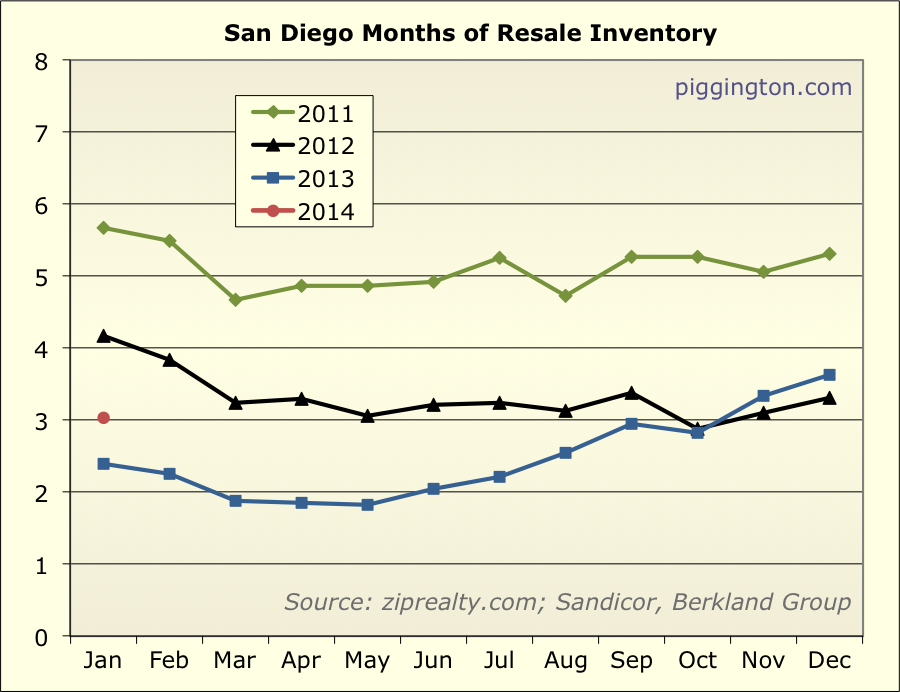

The all-important months of inventory measure was 27% higher than

last year:

But that was coming off an extremely low base, and months of

inventory still shows a scarcity of homes for sale compared to

demand:

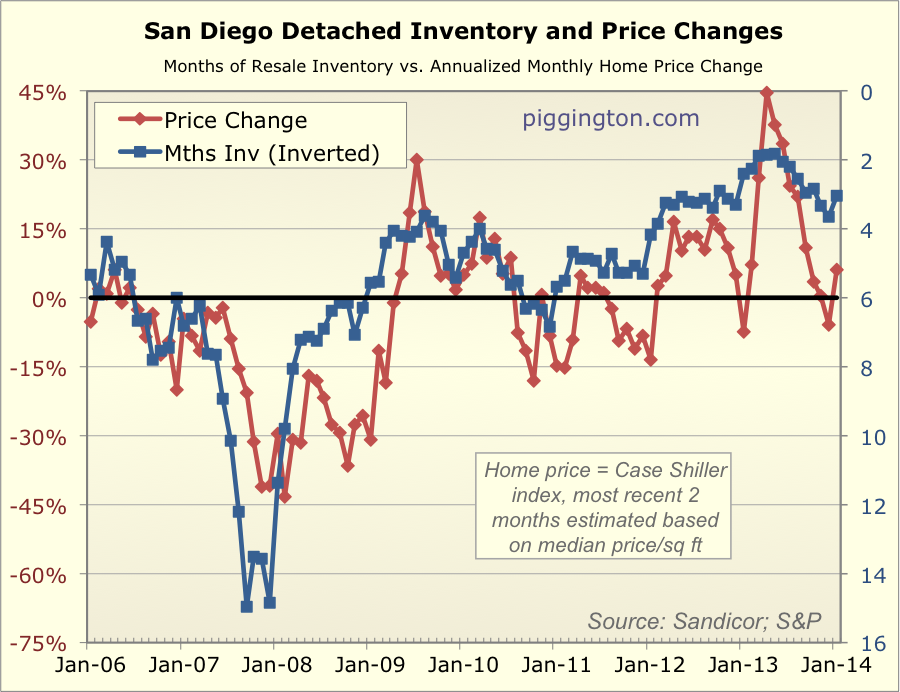

Here’s the chart comparing months of inventory and price

changes.

Notwithstanding the recent (and thus far very short-lived) price

dip, the tight level of inventory suggests support for home prices

in the months ahead. However, sales are weaker than this time

last year, and active inventory is higher, so I wouldn’t expect

anything like 2013’s price surge.