My pal Ramsey is a retired real estate broker and grizzled 1990s housing bust veteran. When he’s not dragging me to Chinese restaurants on the Department of Health watchlist, he spends his time thinking about how this particular real estate cycle is going to play out, placing a special emphasis on new age lending practices. A couple weeks back Ramsey sent me an excellent (and very long) treatise on foreclosures, which I reproduce in its entirety below.

Foreclosures, Real Estate Financing, and Their Impact to the Real Estate Market

Starting from 2002, every participant in the broad real estate arena has been trained to ignore financing as an integral part of all real estate transactions. It is so easy that it seems anyone who wants a loan can get a loan. No down payment? No credit? No problem.

So where do we go from here? As most of you know, since 1982, my specialty in real estate was foreclosures. I have never seen a cycle like this before so I have no historical comparison to draw from. All I can offer is some thoughts and points to ponder over:

- REOs are “must sell” properties. Once they become prevalent in a market, they will influence market prices.

- Homebuilders’ spec homes are “must sell” properties. They will be competing against other “must sell” sellers for the buyers.

- REOs have no sellers who are intending on trading into another housing unit, be it new or existing.

- Homebuilders’ spec homes have no sellers who are intending on trading into another housing unit, be it new or existing.

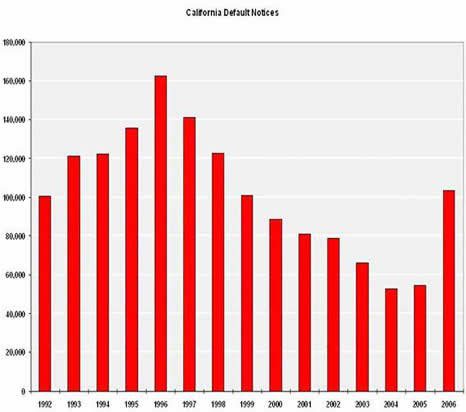

- NOD – REO (notice of default to completion of foreclosure) is averaging 150 days in San Diego. It then averages two months or more before the REO is listed for sale. In other words, a default notice posted today is a housing unit for sale six months from now. Defaults started increasing during the second half of 2006 and are showing no signs of slowing. Most of these defaults are inventory that are still months away from hitting the market.

- A homebuilder who begins construction on an unsold spec home will have a completed unit for sale two to six months from now. Homebuilders are sitting on record levels of unsold specs, both finished and under construction. Aside from what has already started, it is unclear whether the builder will keep building regardless of market conditions.

- The percentage of defaults which eventually become REOs changes with market condition. As conditions deteriorate, the percentage becomes higher and higher, as does loss severity.

- The consensus opinion appears to be that defaults are limited to the subprime loans and their impact to the overall market will be limited. Limited to what?

- Homeownership rate reached an all time high of 69% last year, made possible by the credit bubble. If a more sustainable level is in the low to mid 60’s, as it had been prior to the bubble, 10% or more of current homeowners would have to be “demoted” back to renting while removing a huge chunk of the demand in the process.

- 2007 is the peak year for recast. There is no historical comparison for this level of recast, at this low level of equity, with such high debt ratios and such huge potential adjustment in payments. Compounding that with little or no property appreciation, we are venturing into new territories. We will soon find out if the economy is strong enough to absorb this blow. There is, however, no doubt that the recasts would make affordability an issue, even for those who have already purchased a home.

- Financing is not only about interest rates. What has been overlooked are the terms that made home purchasing feasible for many who might not have otherwise qualified. These are called non-traditional mortgages. With the rising default rates, Wall Street is losing its appetite for these toxic products. What percentage of new and existing homes was sold to buyers using non-traditional financing?

- The easy credit was made possible by Wall Street with not only MBS, but all the derivative products. However, no exotic derivative is going to change the basics of a mortgage: the borrower’s ability to repay. Now borrowers are not paying in volume. What will replace the MBS market if the current MBS buyers vanish?

- Where is the demand going to come from? Taking out the demand created by the credit bubble, the core demand never left. They are the ones who are supporting the current 1.04 million new home sales pace, about the same as the 1.09 million sales for 2003, higher than the 976k for 2002. They are the ones who are supporting the current 6.2 million existing home sales, higher than 2003, or as David Lereah of NAR kept repeating, the 3rd highest year in history. As for that artificial demand of the bubble years, I do not think that is going to return without a new bubble.

- The up cycle: lower interest rate creates demand, prices go up, more homes get built, easy financing creates more demand, prices go up more, investors/flippers create more demand, prices go up more, more homes get built, easy financing allows previously unqualified buyers to own homes creating more demand, prices go up more, more homes get built. This cycle ended in 2005, and was confirmed in 2006.

- The down cycle: the “must sell” properties will lower prices to sell their units, lower prices will depress overall prices making it more difficult for those facing recast to refinance or otherwise work out their financial woes, creating more foreclosures, more foreclosures add to the inventory, creating more price competition and further tightening of underwriting standards. How vicious this cycle will be is anyone’s guess now.

- The debate in the real estate cycle appears to be whether the worst is already behind us or is it three to six months away. Is it not possible that this down cycle may be at the beginning?

Conclusion

Time has always been kind to owners of real estate as long as they can hold indefinitely. Homeowners who live in the same house and service the same fixed rate mortgage using income from the same jobs can hold indefinitely. To them, the house is a home, a shelter. The utility of the home does not change with the value. The credit bubble has created circumstances for some homeowners that even if they remain employed and live in the same house, their debt service may rise beyond their ability to pay. Furthermore, the size of this credit bubble could trigger systemic failure, far beyond the S&L fiasco of the late 1980s.

2007 will be the year that we find out how strong the US consumers really are. We know with certainty that the builders have too much inventory in both land and specs. We know defaults are escalating and REOs from foreclosures completed a few months ago are just starting to show up as inventory. Without the fuel from the credit bubble, absorbing the estimated 1 million to 1.5 million units of excess inventory is going to be challenging.

I opine that the biggest danger lies in the complacency exhibited by economists, market participants and regulators. It is not whether they are optimistic or pessimistic; it is quite obvious that many have not given the widely available data much thought before jumping to their respective conclusions.

Does anyone have a plan in the event of a hard landing?

—

The following are my notes and thoughts in support of the aforementioned scenarios. They are in no particular order. Furthermore, I studied in detail two batches of REOs in SD to understand the current timeline, the reasons for default, the disposition and the estimated losses for each property. These are ongoing studies to be completed when the majority of the sample properties are disposed of .

What is different this time?

During a CSFB builders’ symposium last fall, all the old homebuilders were asked this question: What is different this cycle? One after another, the old timers repeated that they did not anticipate how fast this cycle burst, especially when economic conditions were, and still are, considered good, unemployment rate low, job creation relatively strong and interest rate low. You can say the same about the mortgage bubble.

So why is it different this time? All cycles, up or down, are created by demand/supply imbalances. Previous down cycles typically began with economic factors that changed the demand/supply equilibrium, usually on the demand side. For example, during the early 1980’s when Volcker raised rates, it was virtually impossible for buyers to qualify for 13% fixed rate mortgages. When rates came back down, the pent up demand was then responsible for the up cycle until demand/supply reached equilibrium again. Unemployment would be another common reason for down cycles. The unemployed creates a pent up demand which will materialize when employment conditions improve.

This up cycle started when the real estate market was already on an up cycle, with very healthy sales volume and price appreciation. The demand created to drive this up cycle higher was purely artificial, via the credit bubble. The excess supply created to drive this artificial demand is therefore also artificial.

Many believe that because the economy is strong and unemployment rate low, the correction is just a normalizing process. It is entirely possible the reverse is true. It is difficult to envision how the unemployment rate can be lower than the current mid 4% range. If homeowners are losing their homes while they are fully employed, what happens if they start losing their jobs? If we go down from here, as in a hard landing, the remedies are going to be very limited. Mortgage interest rate will not be something that the Federal Reserve has any control over. It will be up to the MBS market.

Non-traditional Mortgages

In the old days, Freddie Mac and Fannie Mae were the two agencies that controlled the secondary markets. The majority of real estate loans are “agency conforming”. Basically, the agencies prescribed a set of underwriting guidelines that all mortgage originators adhered to.

Today, non-traditional mortgages drive the market. The perils are:

- Qualifying borrowers

- Collateral-dependent loans

- Reduced documentation or stated income

- Piggyback 100% LTVs

- Teaser rates

- Subprime borrowers

- Non-owner loans based on ability to service debt

- And the worst of all: Risk layering – all of the above.

Federal and State agencies have issued guidelines. Whether these guidelines have teeth is no long an issue. The market has clearly lost its appetite for these products.

CLTV vs LTV (combined LTV)

It was not until recent months that the average analyst had paid attention to CLTV. Lenders and the mortgage arms of homebuilders had been reporting only the LTV, without disclosing what the actual encumbrances were by not including any junior liens in their reports. My foreclosure study shows that the “C” part of these piggyback CLTV loans is resulting in 100% loss severity for the holders of these liens.

My foreclosure study further demonstrates that 100% of the foreclosures today are in one of more of the aforementioned categories, with piggybacks being the most prevalent reason.

How many piggybacks are out there?

Percentage of Mortgages with Piggyback Loans, Third Quarter 2006

Of the 40% of mortgages with piggyback loans in the United States, 69% have an 80% or higher combined LTV, while 44% have a 95% CLTV or greater.

Quantifying the market’s exposure to subprime loans

Unfortunately, there is no commonly accepted definition of a subprime loan. One researcher may call subprime the loans made to borrowers with a low FICO score while others may include all non-traditional products. With risk layering, it is very easy to double or triple count since they are not mutually exclusive; e.g. could a 80/20 piggyback loan to a low FICO borrower using stated income be counted as three non-traditional mortgages?

I tried to isolate just one component to see if I could get a rough estimate of what a quantifiable consequence may be. In this simple analysis, I took two major subprime lenders – New Century and Novastar, representing the top end and the bottom end originators respectively.

|

|

Loan Production (billons) |

||

|

|

2006 |

2005 |

2004 |

|

New Century |

$59.8 |

$56.1 |

$42.2 |

|

Novastar |

$10.2 |

$9.2 |

$8.4 |

Source: company press releases

This is a distribution of the subprime loans originated. Though the chart is for 2005, 2006 should not be much different. As you can see, New Century and Novastar alone originated almost $100 billion in these so called 2/28 ARMs in the last two years. There are easily over $500 billion of these 2/28s originated during the last 24 months, ticking away like time bombs.

Distribution of Subprime MBS Purchase Loans by Loan Type, 2005

Subprime originators are scrambling to alter underwriting standards to reduce defaults. As a result, many subprime borrowers looking to roll their old 2/28s into new ones find the loan program that they previously qualified under had been eliminated. Without price appreciation, these borrowers are left with few options.

At this writing, the default rate of these 2/28s is spiraling out of control. This is a brand new product that has never been stress tested in previous cycles. We do know that these products had been sold to investors at such narrow spreads which may not accurately and adequately compensate for the risk involved.

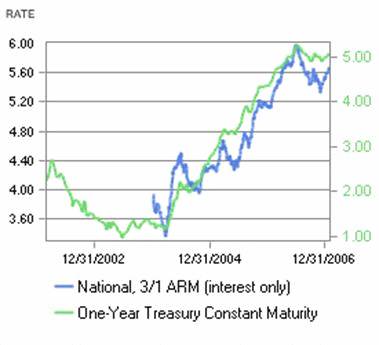

Hybrid recast

Hybrid recast is likely a much bigger problem than subprimes that no one is paying attention to, though hybrid and subprime are not mutually exclusive. While the hybrid recast may not cause a wave of defaults, they will increase household mortgage debt.

Most of the hybrids have a 2.5% interest cap at recast. Since the current fully indexed rate is likely to be at least 2.5% over the rate at origination, I am going to use 2.5% to illustrate the impact. The 3/1 ARMs that originated in 2004 are all facing recast this year.

Original Loan amount – $300,000

Original Interest rate – 4.25% (just an approximate for the period)

Original payment amortized – $1,476

Original payment I/O – $1,063

Recast interest rate – 6.75% (4.25% + 2.5%)

Principal remaining for originally amortized hybrid – $284,160

Recast payment amortized for remaining 27 yrs – $1,908

$432 or 29% payment increase

Principal remaining for original I/O hybrid – $300,000

Recast payment amortized for remaining 27 yrs – $2,014

$951 or 89% payment increase

Source: Bankrate.com

Source: Bankrate.com

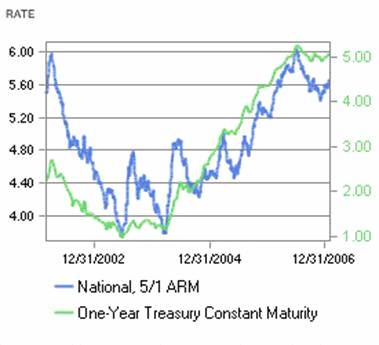

After the 3/1 ARMs, the wave of the 5/1 ARMs is coming.

Source: Bankrate.com

Whether foreclosures will result is not going to change the financial burden of those facing recast. Using the current rates, here are the alternatives in the order of the lowest impact to monthly payments:

Refinance into a new ARM.

Refinance into a FRM.

Pay the reset payment amount.

As an example, Thornburg Mortgage (TMA) is salivating over the up coming recast. I suppose they are counting on their borrowers having no option but to pay.

Mr. Goldstone concluded, "Adding to our positive outlook is the anticipated earnings benefit we should realize as the interest rates on approximately $7.2 billion of our hybrid ARMs will reset over the next 24 months from an average interest rate of 4.63% to a current market rate."

This is why refinancing volume is an extremely important indicator; an indicator that is not receiving the deserved attention. With interest rates relatively stable, and higher than a couple of years ago, there should be very little refinancing today. The MBAA refinance application index today should be similar to that of the low points during early 1990s, 1995 and 2000. Yet, as of last week, refinance applications per MBAA are responsible for 47.8% of all applications. Obviously, these were for the purpose of rolling over subprime 2/28 loans, hybrid recasts or just cashing out equity for living expenses. A high refinance volume, especially from ARMs to FRMs, would be a strong indicator that the recast problem is being resolved in an orderly manner. The confirmation would be a stabilization of defaults, if not an outright decline. If the refinance volume does not stay up, that implies borrowers facing recast are forced to pay a much higher rate. Defaults should follow.

MBA Refinance Application Index, January 1990 through Present

This is what happened in 2006 per FreddieMac.

|

1-Year ARMs |

3-Year ARMs |

Longer Initial-Period ARMs |

||||||

|

1/1 |

1/1 |

1/1 |

3/1 |

3/3 |

5/1 |

7/1 |

10/1 |

|

|

Loan Terms |

— — — P e r c e n t a g e P o i n t s — — — |

|||||||

|

Underlying Index Rate |

4.96 |

4.96 |

4.96 |

4.96 |

4.61 |

4.96 |

4.96 |

4.96 |

|

Margin |

2.77 |

2.75 |

2.71 |

2.76 |

2.78 |

2.76 |

2.76 |

2.79 |

|

Fully-Indexed Rate |

7.73 |

7.71 |

7.67 |

7.72 |

7.39 |

7.72 |

7.72 |

7.75 |

|

Initial Year’s Discount |

2.29 |

2.07 |

2.05 |

1.84 |

1.56 |

1.76 |

1.66 |

1.60 |

|

Initial Interest Rate |

5.44 |

5.64 |

5.62 |

5.88 |

5.83 |

5.96 |

6.06 |

6.15 |

|

Fees and Points |

0.6 |

0.5 |

0.4 |

0.4 |

0.4 |

0.5 |

0.4 |

0.4 |

|

Fixed-Adjustable Rate Spread |

0.69 |

0.49 |

0.51 |

0.25 |

0.30 |

0.17 |

0.07 |

-0.02 |

|

Product Concentration (%) |

52 |

28 |

15 |

69 |

4 |

84 |

47 |

28 |

Source: FreddieMac

(For those who have access to analysts’ reports, the best and most recent data can be found in Bank of America’s December 15, 2006 – Specialty and Mortgage Finance Weekly by Robert Lacoursiere. It is the only report that I know of which factored out the percentage of homeowners with NO MORTGAGE in the overall analysis.)

Wall Street’s Moral Hazard

Non-traditional mortgages were Wall Street’s money making dream. A year ago, the game plan was still to vertically consolidate so the big firms would own every branch of this money tree. They already controlled the beginning via warehouse lines of credit and the end via the MBS markets. They were in the process of taking over the middle by buying up all the originators and servicers before the loans started to sour.

Wall Street did not realize the moral hazard they created in the process. As long as OPM was used to buy their junk loans, the originators would gladly make those loans, reaping huge profits in the process. Underwriting standards were based on what Wall Street would buy rather than the qualifications of the borrowers. When these loans turned sour, the originators simply closed their doors temporarily , especially when repurchase obligations became too high. If you dig into the background of the executives of Argent, New Century, Option One, Novastar, I am certain you will find previous employment at companies such as Associated First, Conti, South Pacific Fundings, and many other subprime lenders who folded in the 1990s.

This website, though simplifying some things, serves as an excellent illustration of current conditions in the subprime market.

Will it blow up? No one knows. Derivatives are traded in unknown quantities in unclear products. Paper thin margins made enormous profits possible only via huge leveraging. We may see a sequel to LTCM.

Short Sale

Though short sales are commonly attempted, my foreclosure study revealed a major hurdle that would likely prevent them from happening in volume – the piggyback loans. In order for a short sale to happen, the lender has to agree to a lesser amount than the encumbrance. In the event of a piggyback loan, the junior lien holder has no incentive in accommodating the borrower since they are going to suffer a total wipeout anyway. Short sales are overall positive for the market because they would not drive the price as low as a foreclosed REO would. Without a short sale, defaulting borrowers have no choice but to let it go to full foreclosure.

Foreclosure Data

Unfortunately, I know of no good source for timely nationwide foreclosure data. MBAA provides some good data but their report is not only quarterly but about two months after the end of the quarter. By default, Realtytrac may be the best available.

PMI provides a good heads up for the major MSAs via their monthly report.

Regionally, DQN has the best and timeliest.

Source: DQN and Calculated Risk

Locally, I have weekly updates that are 100% accurate but only for San Diego. Though a major MSA, it is not big enough a sample for the nation.

REO study #1 – updated Jan 23, 2007

- Period – all REOs recorded from 8/17/06 to 8/29/06

- 26 – Sample size (31 total, 5 has no data available)

- 9 – Sold (closed escrow)

- 3 – In escrow

- 7 – Active

- 7 – Not on market yet

- (2 – Current foreclosure by junior lien holder, likely to be foreclosed soon by 1 st)

- Average days from NOD to REO – 149 days

22 of the 26 REOs have 2nd liens that are totally wiped out – 100% losses . In terms of dollars, the loss amounts to $2,046,500 or $93,000 per property . This loss was already realized the moment the 1st completed foreclosing on their liens.

With only 9 closings, the average loss severity is not very meaningful. It is estimated at 49.4% based on preliminary analysis. This is obviously an on going study that will be updated till the majority of the sample is disposed of.

REO study #2 – updated Jan 23, 2007

- Period – all REOs recorded from 10/4/06 to 10/9/06

- 28 – Sample size (30 total, 2 has no data available)

- 1 – Sold (closed escrow)

- 2 – In escrow

- 15 – Active

- 10 – Not on market yet

22 of the 28 REOs have 2nd liens that are totally wiped out – 100% losses .

With only 1 sale, there not enough data to analyze the loss severity now.

I think the word that should

I think the word that should jump out at everyone is “unprecedented”. I keep referring back to the bust of the ’90s and how badly burned some of the GFs from 1988-1989 were, but that upswing was only 1/3 above the long term trendline from where we peaked this time.

The losses of the ’90s were commonly in the low-mid five figures, and those loss rates drove a lot of lenders and their borrowers under. We’re already seeing foreclosure losses starting in the 6 figures this time, and I don’t think we’re anywhere near being done yet.

Seriously, how many people who work for a living can recover from a $100k loss without bankruptcy? What would it be like if a $600k house at peak pricing eventually settled at $400k?

Yeah, the media is only just

Yeah, the media is only just now catching on to the scope of this story. Unfortunately, J6Pck is still blissfully unaware of the magnitude of this credit bubble.

It is truly akin to standing on the shore and turning one’s back to the approaching tsunami.

“Seriously, how many people

“Seriously, how many people who work for a living can recover from a $100k loss without bankruptcy?”

__________________________

Ironically, I believe a homeowner can simply walk away from his original purchase loan (including a piggyback loan). They would lose whatever downpayment $$ they put into the deal (which these days seems to be, oh, about $0) but I don’t think the lenders have any recourse to collect any shortage after the foreclosure sale.

The folks who stand to get creamed are those who have refi’d and also taken out 2nds or HELOCs and are upside down. I believe the lenders can obtain judgments against them for any deficiency after a foreclosure sale, which very well could end up in the six figures. Seems to me, though, that the typical problematic scenario being referred to on this site is the recent 100% finance purchaser who is facing a reset and is or is on the way to being upside down. I think these people just walk, if necessary, and take the credit hit and the pride hit but no real monetary loss.

I’d be very interested to get Ramsey’s take on the servicing/lending industries reaction to the potential wave of foreclosures. As quoted by Rich, refi volume is high and presently indicates an orderly response to looming resets. If this continues, could it be disaster averted? And if not, what will be the industries’ reaction in terms of forebearance, renegotiation of terms and other classic and well established loss mitigation responses to homeowner distress.

Rich, you have a thoughtful

Rich, you have a thoughtful friend who is generous with his time, to have put together such an informative post. Thanks for sharing.

This article was well

This article was well thought and very informative. Kudos to Rich and Ramsey. It will be interesting to see if the lenders try to push thru some kind of “emergency” legislation or regulation that will allow them to obtain judgements against owners who walk away from their properties.

Either that, or we could see another massive bailout like the S&L crisis of the 80’s. I wonder how the voters in the Red states would feel about having to pay back the mortgages of people in CA.

Asterix

Not only a 100k loss, but

Not only a 100k loss, but even though the lender can’t seek compensation if the mortgage was a purchase and not a re-fi. The lender can/will issue a 1099 for the 100k to the defaulted borrower who will then owe Uncle Sam a boat load on income taxes!!!! If I am correct, bankruptcy doesn’t wipe out income taxes owed.

In the case of the homeowner

In the case of the homeowner who is indebted only by original purchase money loans (including the 80/20 deals that probably make up the majority of the problematic situations), I believe they not only escape liability to the bank for any shortage on a foreclosure sale but also avoid being taxed on the shortage by the IRS. I think this is the outcome of non-recourse loans in California. I’m not a tax specialist by any means but I do believe the outcome will be that these folks can simply walk (and of course have the 7 year foreclosure hit to their credit).

Thanks to your friend Ramsey

Thanks to your friend Ramsey Rich.

The thing that catches my eye is his opening bullet:

REOs are “must sell” properties. Once they become prevalent in a market, they will influence market prices.

Refi’s are high, but foreclosures are higher. From Bubble Markets Tracking Inventory Blog we see San Diego had 1475 foreclosures in January. From the Sandicor MLS on resale homes, we see San Diego had 1768 sales of existing homes.

Looking back to foreclosures, we see Feb is rocking, 1719 foreclosures as of Tuesday the 13th. How high will it go?

So do the banks feel the critical pinch of volume? If January foreclosures hit the market in March and Feb in April, when will the banks reach critical mass? They had 1251 and 1304 foreclosures in December and November. Those apparently came online January and this month.

With current foreclosures on par with the resale sales rate, how long before the banks blink in the game of Chicken pricing to move the volume they see in their pipeline?

From the 4S Ranch Update based on OCRenters pricing info, the other must sell that Ramsey pointed out being builder Specs, appears to already be blinking.

If current volume all home (new & resale) is in the 3400 units range and the banks end up with a foreclosure pipeline for 2007 with 50-100% of that volume every month in “must sell” properties. How hard is the landing?

Can the banks sits comfortably with 24,000 REOs in SD alone on the books with a book value of $12 Billion?

this is one of the best post

this is one of the best post i have read, thanks for the hard work. Passing this to all i know

Very well written post. I

Very well written post. I have been talking about this as well. In fact I have spoken to many MBS traders and they were not even aware of the CLTV… they simply priced on the LTV and priced accordingly.

The aggressive lending is the problem we are facing. As you indicated in the recast of 2/28, I have created a 2/28 mortgage calculator this automatically calculates the adjustments and many will be surprised by the jump in payments… often increases of over 50% for the I/O products.

The 2/28 is a much bigger problem than the pay-option arm that everyone loves to vilify which only has the 110%-125% recast option that no-one really understands but still semi protects borrowers since payments don’t really jump unless they hit the recast.

Many of these 2/28 have 3 year pre-pays further prohibiting borrowers from qualifying due to lack of equity when you combine low or negative appreciation, prepayment fee’s and new loan fee’s… and the fact that they will no longer qualify for a “real” mortgage where they have to state their real income.

The word on the street from the wholesale lenders I know is that the “stated” income loans for “salaried” borrowers are going to be gone by late March, early April.

I have been around since 1987 and remember 89-91 in So. Cal when 51% of homes sold in OC where short sales… as stated in the article… that can’t happen this time around because of the 2nds.

Also, what is significant to me is the change in people’s attitude towards real estate. Clients used to buy a house because they wanted a “home” now they buy because they want an “investment”. Borrowers will be more likely to walk away from their “investment” if it’s not making money then walk away from their “home”.

Also, there is no longer this association of the Scarlett Letter F for foreclosure on your chest as being a loser for losing your house to foreclosure… just the letter A as being an A+ smart real estate investor who walked away from a bad investment.

mortgage info:

I really

mortgage info:

I really think the effort for the 2/28 calculator was noble but I regret that the output from the calculator paints to rosy of a picture. My experience with these products tells me you need to add a 3% initial rate adjustment with 1% adjustment every 6 months. That is the way most, if not all 2/28’s and 3/27’s are written these days. You will see that in today’s flat to inverted yield curve tug of war, even at flat, payment increases are going to be even greater than projected in your calculator.

In reference to option ARMS being less risky, you need to re-think the 110% recast statement for sure and possibly even the 125%. The way these loans are currently being sold is going to kill borrowers. It is truly not the recast feature in itself, but irresponsible pricing strategies and lending practices.

Once upon a time Option Arm loans were better performing and less foreclosed on than Fixed rate loans. Unfortunately thanks to Wall Street joining the party and uneducated greedy originators, the true pioneers of the option arm market abandoned their sensible pricing practices. They did this to compete with Wall Street for business originated by a bunch of bloodthirsty greedy thug originators whose vacation home, or new Mercedes was more important than the safety of their client. Their greed ultimately sold many unsuspecting borrowers down the river.

The lenders and investors day of reckoning is coming, and a 110% recast will blow up 3-8 months sooner and with a lot louder bang than the 2/28’s! If you look at the large spread from fully indexed option arms with a low 1 – 2% start rate you will see that 110% can be reached well before month 24. The recasted payment vs. the minimum payment is over a 100% payment increase. Can you say payment shock? There is no way that the 25th month payment on the 2/28 ever reaches this magnitude in the effect on the borrowers budget. I have run the numbers and the Wall Street greed for yield on these loans may blow up in their faces and relatively soon! When they added such high margins and stuck borrowers with 3% pre-payment penalties so they could rebate 3% in premium to a thug originator who never even knew what a recast was, they ruined the product. This will cost them dearly especially since they weren’t finished there, they started lending at 95% to 100%LTV on some of these products. Prior to 3 years ago lenders never really ever approved many if any option arms loans above an 80% LTV and if they did there was PMI. Again unfortunately some greedy wizard said, c’mon guys lets self insure these and raise the margins another .8 to 1.4%(making the recast kick in even sooner). OOPS! I’m sorry, I do not see how a borrower with insufficient equity due to the neg am forcing them upside down in the property, a 3% going away present (pre-payment penalty) with new and improved payments (100% + payment increases) doesn’t walk, do you?

I am just not sure Wall Street ever expected 17 rate hikes and this long of a pause! It may really cause havoc, and option arms once a very effective lending tool may go bye bye forever as a result. The worst has not probably shown itself yet, and it hurts me because greed has ruled over sensibility. I feel we are at that place just before the tech bubble really imploded, you know when you couldn’t help jumping in at the last minute to try and make one more major play and got spanked! OUCH!

Hoping for better than most forecasts, but I am a realist, the storm clouds tell me take shelter!

P.S. Now I know some originator who sells option arms properly and discloses the positives and all the risks is going to write bcak telling me I am wrong. I know you are correct and you sold the lowest margin and you explained all the reasons not to make the minimum payment just like I would. You and I did not create this problem, so don’t bother writing me back defending your position, I understand it! Just think about the 70 or 80% of the idiots who never explained anything, led people to believe their payments were etched in stone for 5 years on a truly monthly adjustable rate loan, locked them in a pre-pay with the highest margin available in this solar system, they are the culprits. Yep, we did the equivalent of handing loaded guns to children! Take cover as there’s gonna be some shootin’!