Administrative note: The new "Finance and Investing" section to your upper right will feature articles from my financial advisory firm’s website. Wait a minute, is this marketing? Well, maybe just a little… but the articles cover topics that are oft discussed in the forums and that could be of interest to many an Econo-Almanac reader.

OK, back to your regularly scheduled programming…

Prices

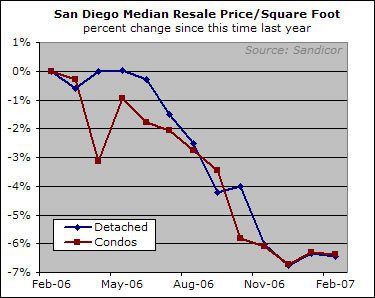

Nothing exciting happened in the pricing department. The size-adjusted median price was pretty much flat for the month, and was down 6.4% for both single family homes and condos since February 2006.

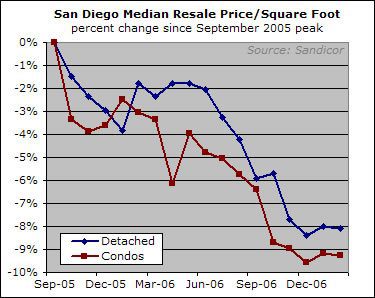

From the September 2005 peak of this data series, single family homes are down 8.1% and condos are down 9.3%.

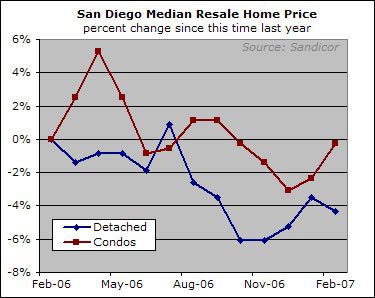

The "plain vanilla" median, which is less informative but more widely reported, presents a slightly more positive picture. While the median detached home price saw a small drop, the median condo price actually rose to the same level where it was a year ago:

Of course, the divergence between the plain vanilla median and the size-adjusted median shows that while the typical condo buyer spent the same amount this year as least year, he or she got a bigger condo for the money.

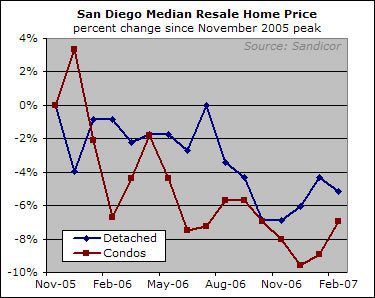

The median price is still down from the aggregate peak in November 2005, though not by as much as the size-adjusted median, which is in my opinion the more accurate measure.

January saw month-to-month increases in both the condo and detached home median prices. I assumed that the commentators would really play that up, but they didn’t end up doing so because the new home median price (to which I don’t have access) got absolutely shellacked and dragged down the overall median. It appears that they have finally given up trying to blame condo conversions for the huge declines in new home prices, a gambit which never made much sense except for the brief and long-ago period during which condo conversion sales were surging as a percent of all new home sales.

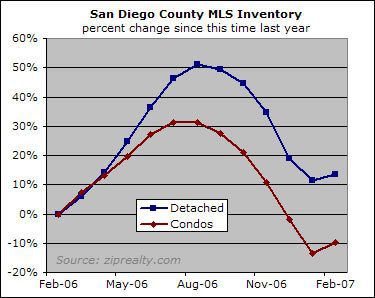

Supply and Demand

A year ago I started tracking inventory for condos and single family homes separately, so I can finally start graphing year-over-year changes as such:

For whatever reason, as you can see, growth in single family home inventory has grown a lot faster than condo inventory for the past year. Both series have started back up after the typical winter slump, but inventory isn’t increasing as fast as it was this time last year. I think that many of the listings last year were from people who wanted to cash out but who couldn’t get a satisfactory price. Some may be back this year, but it’s entirely possible that we won’t see an inventory surge as sudden as what took place in 2006. Unfortunately, a much higher percentage of the homes that are listed will likely be of the "must-sell" variety, as discussed further below.

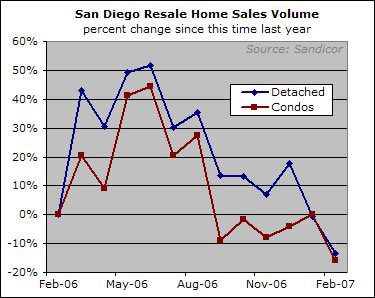

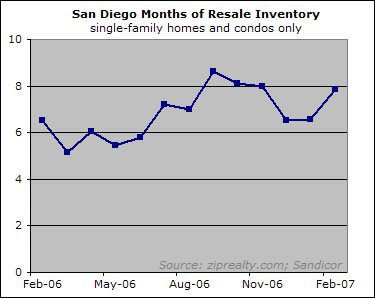

February volume was actually fairly weak after an upside surprise in January:

Sales were down about 14% from the already-anemic pace set a year ago, which allowed the months-of-inventory figure to climb back to just below 8:

Conclusion

As I said, there is nothing too exciting in these numbers. Prices didn’t really change and inventory increased a little but not much. The most significant change was the one-month drop in sales volume, which, being just one month and a holiday-distorted month at that, may or may not be meaningful.

The big story this past month was not in the sales data but in the lending industry. Lender tightening will likely be the prime mover for housing in the months ahead. As I wrote in a recent voiceofsandiego.org piece:

The potential significance of the ongoing meltdown in the mortgage industry can hardly be overstated. As I have described before, the virtuous cycle of higher home prices begetting laxer lending begetting even higher home prices, and so on, was absolutely crucial to allowing real estate prices to achieve their current absurd levels. Prices simply couldn’t have reached these heights without the lenders’ attempts to throw money at anyone who would have it.

Now, those same lenders are scrambling to compensate for their prior excesses, and the virtuous cycle has turned vicious. The increase in defaults has led to tighter lending policies. As borrowers with resetting teaser-rate loans find that they can’t refinance into loans anywhere as sweet as they originally had, more of them default, which leads to even further tightening by mortgage lenders. The process is every bit as self-reinforcing as the one it replaced, though not nearly as much fun. And it could have a big impact on home prices in the months ahead.

Mortgage industry woes didn’t really pick up the pace until late February, so the recent problems probably won’t show up in the closed sales data for at least a month.* We’ll see the impact eventually, though. San Diego’s housing market has become so dependent on exotic loans just to keep things afloat that I don’t see how it could happen any other way.

* – If a monthly update isn’t enough to take the edge off your data addiction, Jim the Realtor’s website has a lot of really good and (more to the point) frequently updated analysis.

the link that says “please

the link that says “please contact us” doesn’t seem to lead to a contact option.

As I said, there is nothing

As I said, there is nothing too exciting in these numbers. Prices didn’t really change and inventory increased a little but not much. The most significant change was the one-month drop in sales volume, which, being just one month and a holiday-distorted month at that, may or may not be meaningful.

Actually, I find this kind of interesting. Both an increase in prices and an increase in inventory. Is there any numbers on completed sales for the corresponding months? It looks like there is an anticipation of good sales volume this spring (reflected in the pricing) but it is not supported by actual sales volume (reflected in the increasing inventory). This seems to indicate to me that the increase in prices we are seeing here, is not supported by the market.. (no confirmation in price move with corresponding increase in volume)

Actually, I find this kind

Actually, I find this kind of interesting. Both an increase in prices and an increase in inventory.

How do you figure an increase in prices? Price per square foot was down for both types, and this is the most accurate measure.

Your thing about anticipation could be right, but if so it’s only slowing down the price decline, not causing price increases.

How do you figure an

How do you figure an increase in prices? Price per square foot was down for both types, and this is the most accurate measure.

Look at the last two tickmarks on the price/square foot… higher than the previous. The RE shills consider this as indicative of the end of the slowdown.. It is not confirmed by reduction in inventory though.

got it. thanks for

got it. thanks for clarifying.