Rich

looking through those Rich

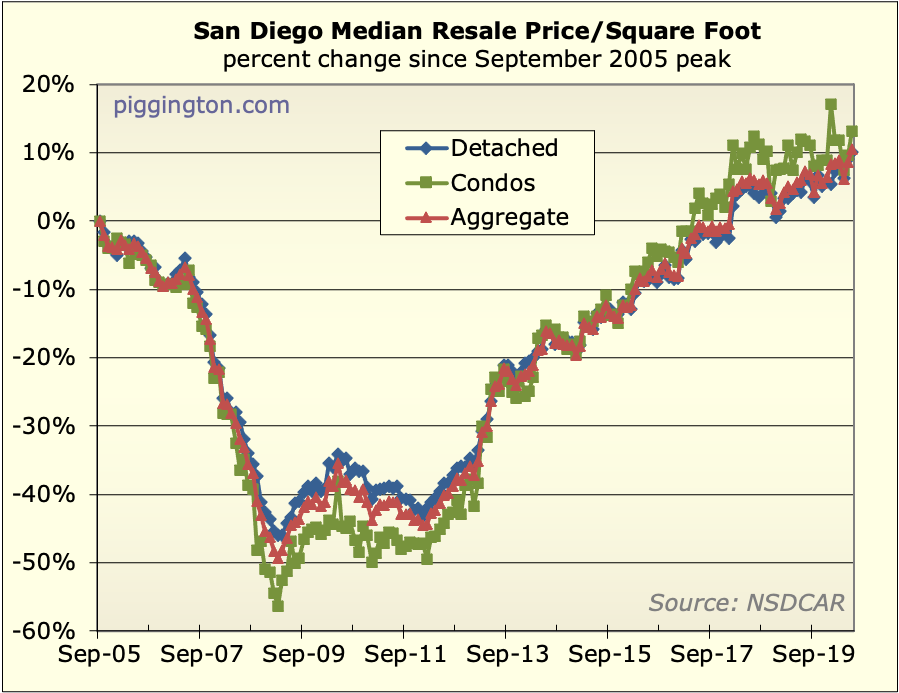

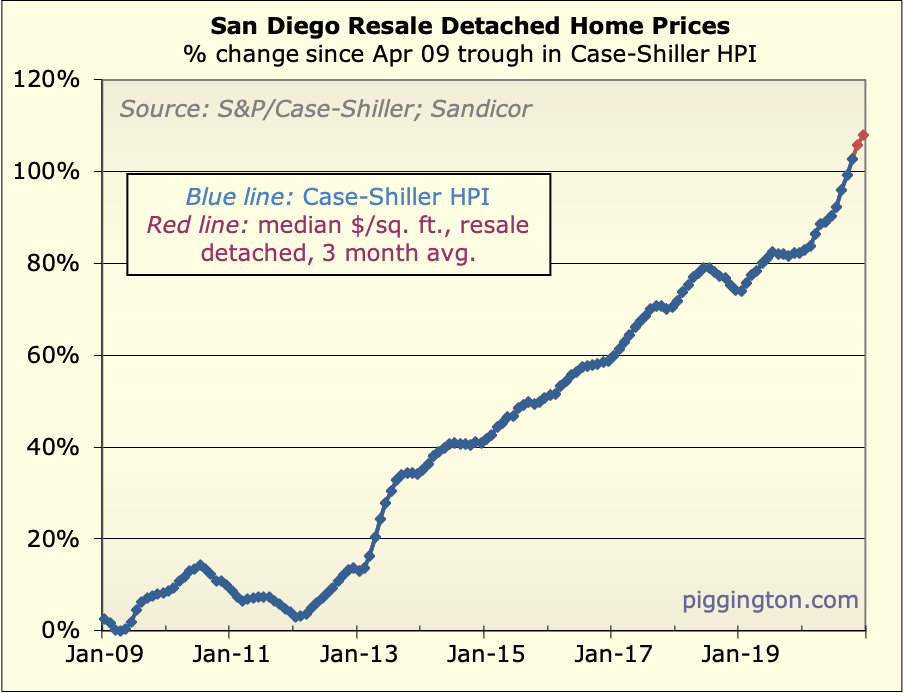

looking through those graphs is just stunning and even moreso as we all lived through it. I’m looking forward to watching how it goes the next decade though I think I know;)

Oh yeah, maybe its time to remove the Berkland Group footnote on the graphs LOL

Rich Toscano wrote:Haha… [quote=Rich Toscano]Haha… perhaps so. 🙂 It is no longer a going concern. (All the data was from MLS anyway in the end).[/quote]

Oh it’s going. There just is no conern

evolusd

5 years ago

Housing market is nuts; I’d Housing market is nuts; I’d consider buying but there’s just NOTHING TO BUY. Thankful our landlord just renewed with a 2% increase, more than fair as rents seemed to have skyrocketed as well in the last 12-mos.

gzz

5 years ago

While I have got some things While I have got some things wrong (my TSLA short is down 50k and counting, never gonna cover!), proud to say from 2013-2019 I consistently told all the random people here posting “should I buy” that I thought they should not only buy, but buy ASAP, not be too picky, and IMO buying is a no brainer. This from 2018 was typical:

“ Imagine someone in SF in 2013 worried about cash flow on a Victorian. They would have missed out on gigantic returns, 500% range on their down payment.”

Lots of assets seem expensive these days. But when safe yields are 1% in dollars and negative in euros/yen, there’s no reason a growth stock should not be P/E of 70 or a house in a good area shouldn’t have a cap rate of 2.5%.

I’m not gonna be the last one to turn out the lights and give up on value investing. I purchased 25k of FIZZ today, my first reddit meme stock, and it went up 5k in a day. I have long owned irbt, and it became a reddit meme stock because it was heavily shorted, and suddenly rose 50%.

gzz

5 years ago

Everything else is bubbling, Everything else is bubbling, so why not 25% increase for 2021?

He’s why it might:

Rates still ultra low.

Bullish investors and holders have been nothing but rewarded for 10 years. The pain of the bust is a distant memory.

Inventory even lower than our last two lift-offs in 2004-2006 and 1/2012 to 9/2014.

Those last two rockets lasted 2.5-3 years. We are not even at 10 months right now.

The only restraints are semi-tight lending standards and high nominal down-payments. Lending was even tighter in 2012-2014 though, and down payments can be 3.5 and 5% and covered with stock and other frothy market gains.

gzz

5 years ago

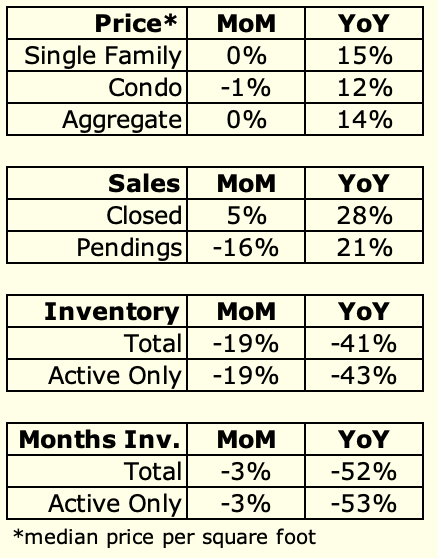

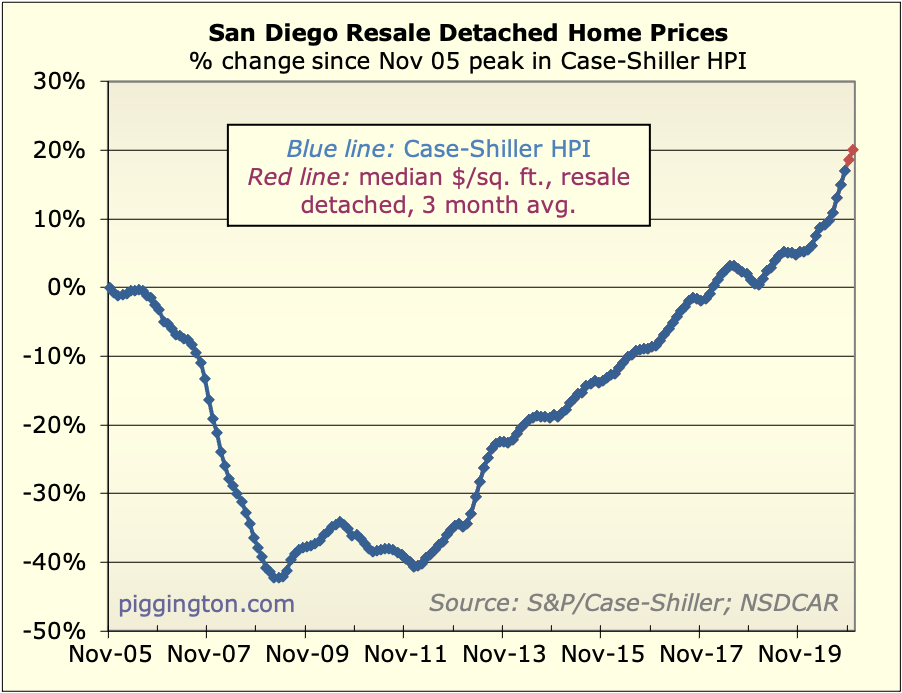

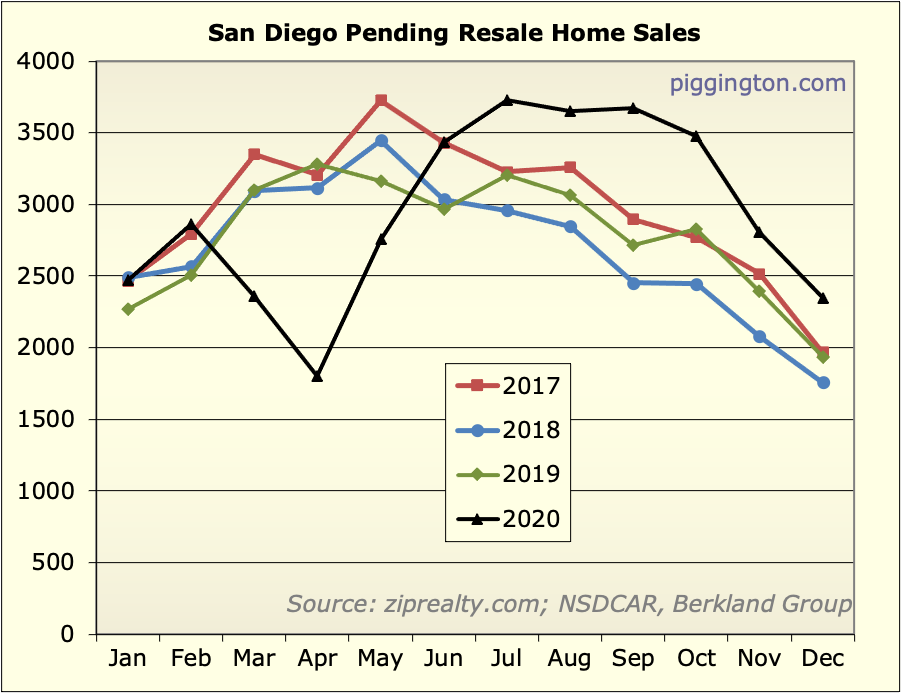

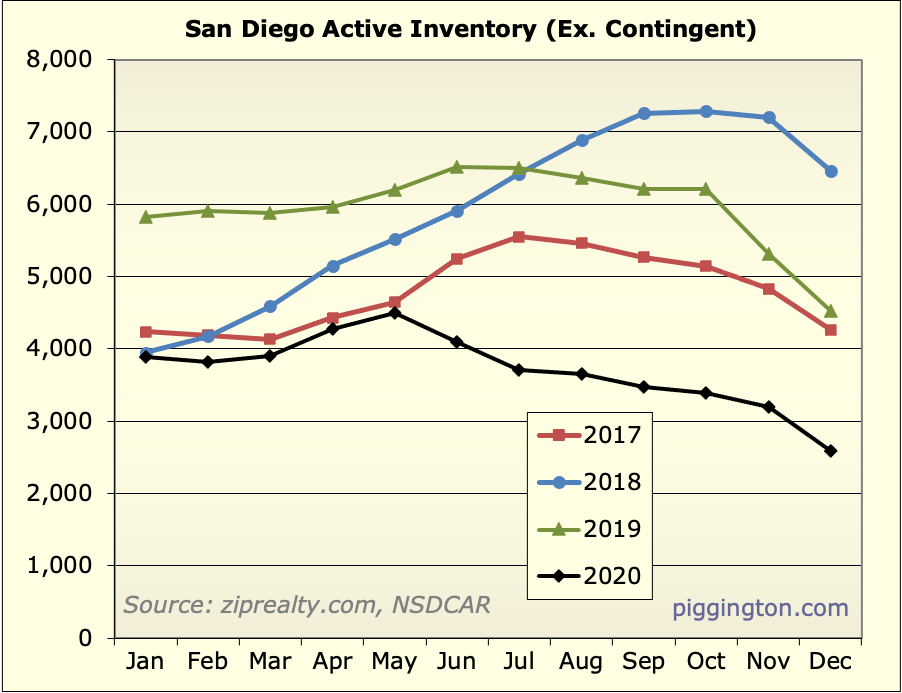

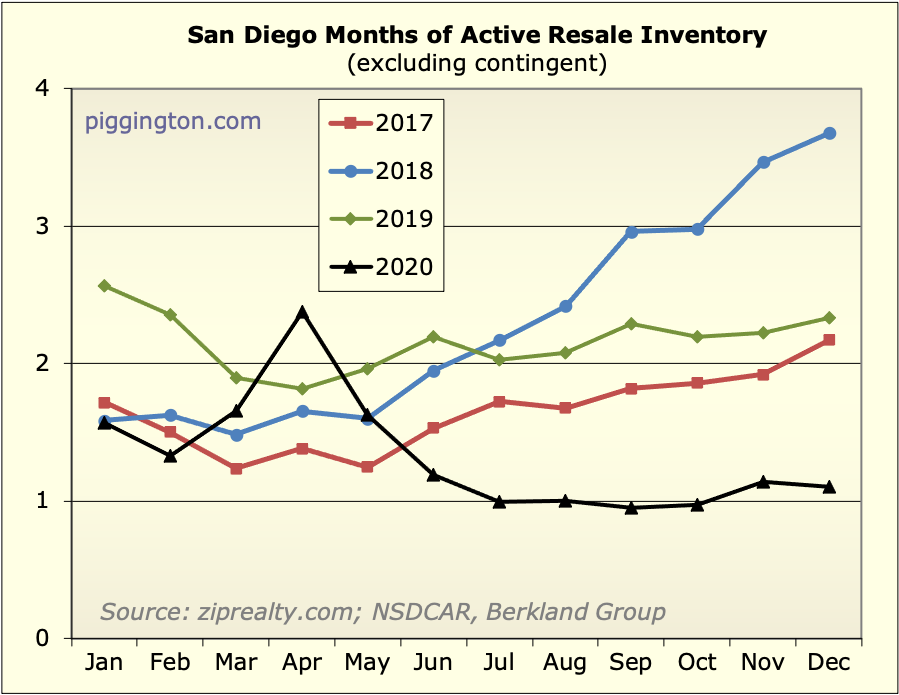

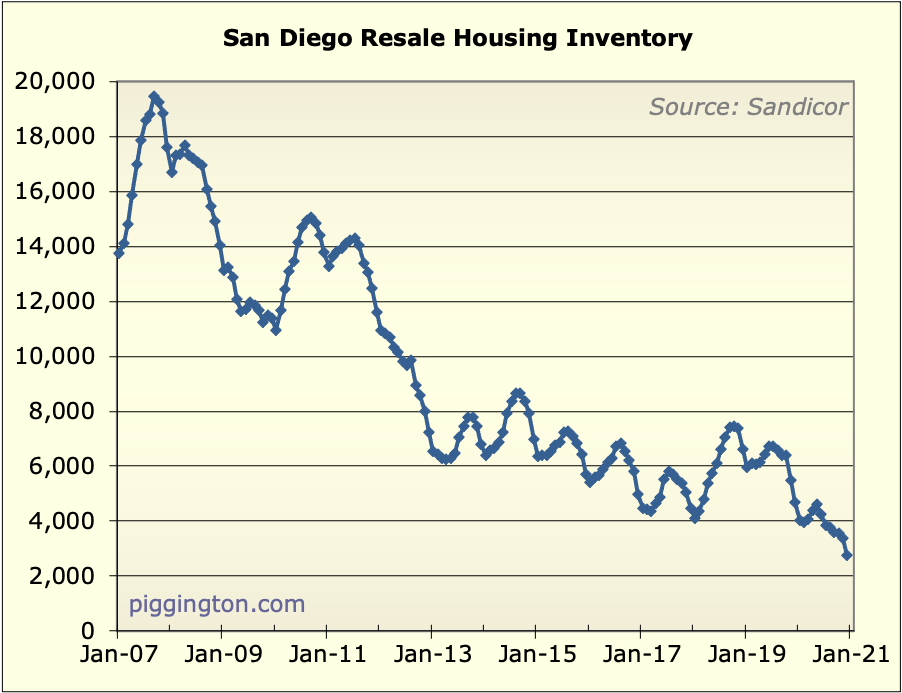

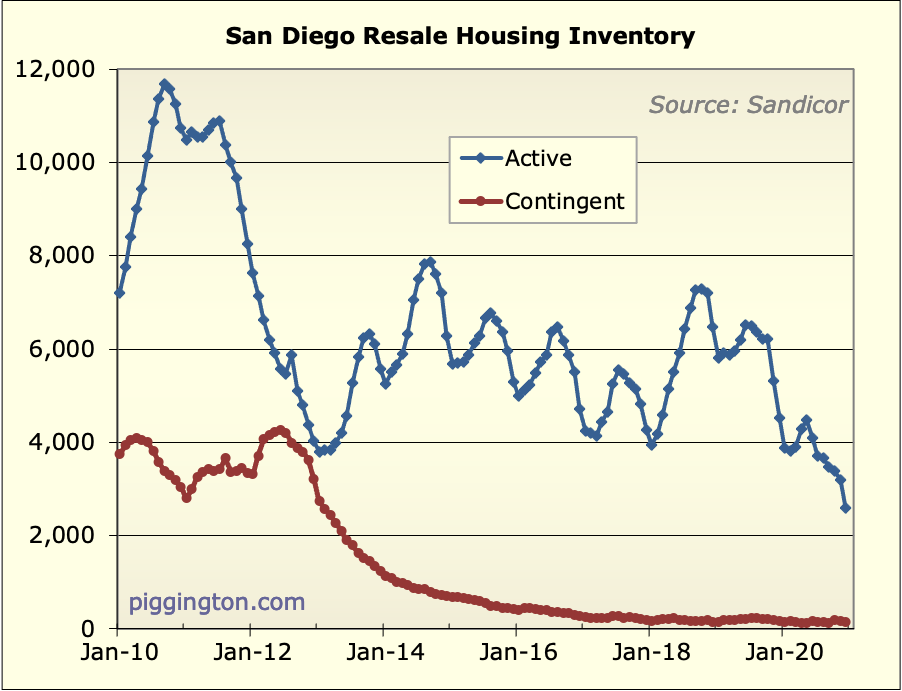

The raw inventory chart is The raw inventory chart is remarkable. The prior vertical leap in 1/2012 started at inventory of 14k and ended (or transitioned to slower gains) at 8k.

This time we started at 6k and now at 2.5k less than a year later.

The 2012-2014 spike saw prices rise about 70% in less than three years. This time we have

higher incomes

lower rates

larger population

looser lending.

Evol: zillow shows 53 detached homes in SD City (excluding San Ysidro) with 3+/2+ beds and baths and under $850k.

Best to get into a rising market and renovate/trade up later IMO.

gzz

I think it was the right gzz

I think it was the right call and credit where credit is due. But its not entirely for the reasons you mentioned nor were the conditions that have caused this recent big run up present or predictable. This big recent gains are due to extreme imbalance of supply and demand. Listings are way down due to the pandemic and demand is way up not only locally but we are seeing an influx from denser higher priced areas.

As for there being nothing to buy, yes its tight but the better agents are the ones that are getting their clients in the better properties at fair prices lately. Experience matters. I see that over and over in my business and among peers

bewildering

5 years ago

How much has discretionary How much has discretionary income increased since 2006?

How much of this depends on low rates?

I wish we had graphs for those questions.

If Case Shiller is inflation-adjusted then is this now a 2006-sized bubble?

bewildering wrote:How much [quote=bewildering]How much has discretionary income increased since 2006?

How much of this depends on low rates?

I wish we had graphs for those questions.

If Case Shiller is inflation-adjusted then is this now a 2006-sized bubble?[/quote]

We do have these graphs! I just need to update them. It’s getting high on the list.

gzz

5 years ago

Worrying about valuations is Worrying about valuations is how I lost big shorting stocks!

Seriously though, as long as housing is subject to more favorable tax treatment and likely rent growth, its yield should generally be lower than federal bonds, but we’re way above this.

Even if we go up 50%, we’ll still be way below that.

Let’s take a typical 700k San Diego condo. Tax will be about 7.7k, HOA about 5k a year, $300 fire insurance, 13k total. If it rents for 2800/mo, that’s a net of about 20.6k.

The 30 year right now yields 1.8%. Applying that to the condo’s yield suggests a price of $1.14 million.

You can quibble with the assumptions here a little, but ultimately the condo’s yield can be protected from taxes fairly easily, and is likely to increase at or above inflation since housing in a nice city like San Diego is a luxury good whose demand increases faster than economic growth, while supply more slowly.

gzz wrote:Worrying about [quote=gzz]Worrying about valuations is how I lost big shorting stocks!

Seriously though, as long as housing is subject to more favorable tax treatment and likely rent growth, its yield should generally be lower than federal bonds, but we’re way above this.

Even if we go up 50%, we’ll still be way below that.

Let’s take a typical 700k San Diego condo. Tax will be about 7.7k, HOA about 5k a year, $300 fire insurance, 13k total. If it rents for 2800/mo, that’s a net of about 20.6k.

The 30 year right now yields 1.8%. Applying that to the condo’s yield suggests a price of $1.14 million.

You can quibble with the assumptions here a little, but ultimately the condo’s yield can be protected from taxes fairly easily, and is likely to increase at or above inflation since housing in a nice city like San Diego is a luxury good whose demand increases faster than economic growth, while supply more slowly.[/quote]

I can quibble with one of the assumptions a lot, which is that 30 year UST yields will stay at 1.8% indefinitely. (You didn’t state that assumption outright, but it’s implicit in your comparing condo rental yields with the 30 year UST yield).

If yields go back to their normal relationship with inflation, the argument collapses. Will that happen? I don’t know (I don’t think anyone knows) but I think it’s a pretty big gamble to depend on rates staying abnormally low forever.

PS I appreciate your comment

PS I appreciate your comment on worrying about valuations, and I feel your pain… but bubbles past showed that people who worried about valuations were eventually glad they did. It just took a while (and felt like forever 🙂

Rich, I just don’t see any Rich, I just don’t see any reason to either assume or predict rates will revert higher.

We don’t think life expectancy will revert to historic levels do we?

Nor per capita real GDP?

Nor the relative share of national income spent on clothing versus health care?

Why are nominal and real interest rates in the category “subject to mean reversion to 20th century levels”?

For me, the rates in peer nations with similar but more advanced population aging are a better guide about the future of US rates, and they point to lower US rates.

gzz wrote:Rich, I just don’t [quote=gzz]Rich, I just don’t see any reason to either assume or predict rates will revert higher.

We don’t think life expectancy will revert to historic levels do we?

Nor per capita real GDP?

Nor the relative share of national income spent on clothing versus health care?

Why are nominal and real interest rates in the category “subject to mean reversion to 20th century levels”?

For me, the rates in peer nations with similar but more advanced population aging are a better guide about the future of US rates, and they point to lower US rates.[/quote]

I’m not “assuming or predicting” that rates will revert higher. I’m simply allowing for the possibility that they will.

I’m not “assuming or predicting” that rates will revert higher. I’m simply allowing for the possibility that they will.[/quote]

No, I will amend this.

I actually kind of think they could go up. They went down because of the pandemic. Why wouldn’t they go back up when the pandemic is over? That seems like the more likely outcome, if I’m forced to guess. But I’ll admit it could be wrong.

But that wasn’t really my main point. My main point was: nobody knows what rates will do, they could do anything and one of those things could be to go up, but your thesis assumes they will never go up.

On balance, 2 of 3 large On balance, 2 of 3 large areas Japan and Europe have negative rates and there is very little expectation they will go positive anytime soon.

The Biden admin probably can’t print/borrow as much as they like with a 50/50 Senate.

Think normally market rate interest should be higher if US seen in isolation.

But with the complex interconnected economies, sideways is also an option for next year years.

Escoguy wrote:On balance, 2 [quote=Escoguy]On balance, 2 of 3 large areas Japan and Europe have negative rates and there is very little expectation they will go positive anytime soon.[/quote]

Our demographic aging and fertility decline is about 10 years behind Europe and Japan. Due to demographic momentum, even the unlikely chance of a sudden baby boom takes a very long time to have any substantial effect.

There’s a very good chance in my opinion of US 10 year rates falling below 0% too in 5-10 years.

“[Rates] went down because of the pandemic. Why wouldn’t they go back up when the pandemic is over?”

Most of the rate decrease was before the pandemic. 30 year mortgage rates had their local peak in Oct 2018 at 4.8%. In Jan 2020, they were 3.5%, now are 2.7%.

A return to a pre-pandemic trendline would mean rates of about 3.1%. I don’t see that denting this market.

“But that wasn’t really my main point. My main point was: nobody knows what rates will do”

No we don’t, but our neutral assumption is the huge and liquid market for US residential mortgages reflects all current information and expectations, and is equally likely to go up as down.

“but your thesis assumes they will never go up.”

Again, I think the neutral assumption is mortgage rates of 1.7% are as likely as a return to 3.7%.

That said, the effect on the market isn’t equal of an increase versus decrease in rates. Everyone is locking in at sub-3% fixed these days, which will tend to decrease supply since the cost of owning goes down and the profit from renting goes up. A mild rate increase wouldn’t be bullish, but it would restrict supply since a 2.7% mortgage is quite valuable when rates are at 4%.

This offset to the negative effect of rising rates is not mirrored by a similar negative offset to the positive of falling rates.

Instead, a further decrease in rates is bullish in a huge number of ways: it decreases mortgage costs, allows another wave of refis, and decreases the return of alternative investments to RE. It further reduces supply by making it easier to avoid foreclosure for distressed owners.

To a large extent, I think these bullish factors are not yet fully priced in yet. Prices are sticky upward because of both psychological factors and also the need for mortgage appraisals to meet comps.

I experienced this myself when I did a refi back in 2013, when the appraisal came in way below actual value and only 5% higher than 2011 purchase price, despite impressive renovations and market that had gone up well over 20% since my purchase.

People in the industry might have other other examples, but outside of the ultra-loose lending of the 2004-2006 bubble period, I think banks are reluctant to extend mortgages that are based on valuations 20% or more higher than 12 months prior, even when the market goes up that much. If true, this theory would predict extremely low inventory, which is exactly what we see. Sellers don’t want to sell below economic value, but won’t list at the market clearing price because they know they may have to deal with the costs and frustration of a strong good faith buyer not getting financing.

I also have a feeling we are mid-way into another bubble-fueling virtuous cycle where rising prices reduce loan losses in every segment of the mortgage market, which leads to looser standards and lower spreads over treasuries, which leads to higher prices.

I’m not totally against buying right now. We’re actually in escrow for a Del Mar condo right now with a price of 197 rental months, so there are still deals to be had. But I see the SFR’s in DMCV as totally over-valued. I saw arguments above of:

higher incomes

larger population

lower rates

looser lending

Higher incomes and larger population should affect rental price equally. In fact, there’s an extra perk for renting in DMCV this year since Del Mar Union is one of the only districts in the county that has full-time in-person elementary school – a perk that should temporarily boost rental value (but not as too much on buying).

Lower rates and looser lending are transient conditions that can’t be maintained forever — if the economy rebounds rates will go up; if there’s post-pandemic recession looser lending might disappear too. I feel like it’s only a matter of time before prices come down to earth (tethered to rental prices). Plus, don’t they say markets tend to crash when everyone buys into the euphoria?

There’s definitely a lot of pent-up demand, but lately I feel like there’s suddenly a flurry of listing activities too (ETA: in the time it took me to write this entire post, two homes came on the market in CV). I don’t know if I’m imagining it or if supply is truly rising as higher valuation as well as the improving covid situation are finally enticing owners to sell. The other thing I remember about the last bubble was that the cheaper homes were rising much faster than more expensive homes, as the buying frenzy drove up the purchasing of any home that people could possibly stretch to buy (instead of a home people actually needed or wanted), as panic/fear-of-losing-out drove purchase decisions. I feel like that’s what’s happening now. I live in LJ Shores where one neighbor just delisted a house that they failed to sell after 6 months; Del Mar looks very expensive but it always has been; cheaper surrounding areas like University City, CV, Sorrento Valley, Solana Beach, Encinitas have risen far more in price – costing almost as much as Del Mar.

I’d love to see a monitor of the number of units listed/pending/sold in DMCV going forward.

I would also love to see what Rich’s valuation index looks like right now. Have we entered bubble territory yet?

P.S. So I went and did my poor man’s version of the valuation index (only based on price-to-rent) by looking at the change in SD rent b/t 1997 and now (according to Zillow, so going from 2.6K to 2.84K), and the change in SFR price (going from 570K to 674K) in the same time frame. And I came up with the result that if the valuation index in 2017 was at 120 according to Rich’s chart ), then it is now at 130, which is a lot higher than it ever was previously except during the run-up to the big bubble, but still is a ways under the peak of 175.

So I guess it could still go up a long ways before falling. If it’s going to be like the last bubble, it could be another 2.5 years before it rounds the peak, and 5 years before prices are “good” for buyers again. But it also be a smaller bubble because lending standards are much higher now; or it could be an even bigger bubble because interest rates have never been so low and the Fed seems determined to keep them low.

feraina: what does the feraina: what does the price/rent look like at CV 1-bedroom condos? I don’t think $1.8 million six-beds are especially relevant to determine market rent ratios.

The one you say was on the market for a long time specifies “6-9” month lease. That implies to me it isn’t long term, but the demand for a high end 3-bedroom for exactly that period might well be zero.

:I live in LJ Shores where one neighbor just delisted a

:house that they failed to sell after 6 months

LJS is older and very high end, with very different lots and views mixed close together. This makes it easier to overprice a house, and harder to tell since the market is inherently fragmented and illiquid compared to CV.

I follow my own zip of 92107 very closely, and my observation is its similar high-end/hard-to-value places in the $2m+ range now sell much faster than any other time. Even high end buyers have FOMO.

I’m not sure where you’re I’m not sure where you’re going with this. But anyway there are no 1beds in CV. I mean there are apartments but not condos. I guess one could look at prices and rent for 2beds. I am guessing the latter is under $2200 (just because Del Mar across the highway is), but they’re selling for over $750K I’d guess. So even worse then the 3beds in rent-months.

feraina wrote:I’m not sure [quote=feraina]I’m not sure where you’re going with this. But anyway there are no 1beds in CV. I mean there are apartments but not condos. I guess one could look at prices and rent for 2beds. I am guessing the latter is under $2200 (just because Del Mar across the highway is), but they’re selling for over $750K I’d guess. So even worse then the 3beds in rent-months.[/quote]

I would caution using CV as a measuring stick for SFR rental market. It is a very odd one and not like most others. The type of people that want to live in an SFR there seem to prefer buying and can afford to do so. The ones that just want to be there for the schools will rent the smallest thing they can get away with like a condo. Much of that is cultural norms.

I worked on renting out a nice 5BR/3BA in CV about a year ago and it was brutally tough. Itw as like banging my head on a wall. Most applicants were groups of students or professional singles not families with 2 to 3 kids as one would expect. Put that house in Encinitas/South Carlsbad and there is a line of applicants for the same or higher rent. Different folks with different values up here. CV SFR rental market is an abnormality in the market.

Oh I just got an alert in my Oh I just got an alert in my Redfin feed that a 1 bedroom in CV listed at $538K is pending. Zillow says rental value is $2250. So a multiplication factor of 240. Sdrealtor, I can see your argument about really large homes but what about a 1 bedroom? Who buys 1 bedrooms? Maybe a professional or an investor. I can’t imagine why an investor would pay that high. $2250 doesn’t even include the $405 HOA fees.

feraina wrote:Oh I just got [quote=feraina]Oh I just got an alert in my Redfin feed that a 1 bedroom in CV listed at $538K is pending. Zillow says rental value is $2250. So a multiplication factor of 240. Sdrealtor, I can see your argument about really large homes but what about a 1 bedroom? Who buys 1 bedrooms? Maybe a professional or an investor. I can’t imagine why an investor would pay that high. $2250 doesn’t even include the $405 HOA fees.[/quote]

Single adults, older folks that want to live alone, second/vacation homes, people that need to come here for work but have family living else where. Those are a few off the top of my head. There aren’t many 1 units comparatively. They rent for only a little less than 2 bedroom units also.

In CV they start around 400k and rent around 2200 so your multiplier is a bit off

feraina, Redfin price and feraina, Redfin price and rent estimates are garbage.

My OB condo it underestimates the property price by more than 65%. As in, it says a 2/2 condo with parking and ocean view 2 blocks from the beach is worth 440k. Really.

The rental range is really wide, but the midpoint of it is substantially lower than it is rented for, and I set the rent 4+ years ago at a friendly level and have never raised it. It’s off by at least 20% on rent.

Rich

looking through those

Rich

looking through those graphs is just stunning and even moreso as we all lived through it. I’m looking forward to watching how it goes the next decade though I think I know;)

Oh yeah, maybe its time to remove the Berkland Group footnote on the graphs LOL

Haha… perhaps so. 🙂 It is

Haha… perhaps so. 🙂 It is no longer a going concern. (All the data was from MLS anyway in the end).

Rich Toscano wrote:Haha…

[quote=Rich Toscano]Haha… perhaps so. 🙂 It is no longer a going concern. (All the data was from MLS anyway in the end).[/quote]

Oh it’s going. There just is no conern

Housing market is nuts; I’d

Housing market is nuts; I’d consider buying but there’s just NOTHING TO BUY. Thankful our landlord just renewed with a 2% increase, more than fair as rents seemed to have skyrocketed as well in the last 12-mos.

While I have got some things

While I have got some things wrong (my TSLA short is down 50k and counting, never gonna cover!), proud to say from 2013-2019 I consistently told all the random people here posting “should I buy” that I thought they should not only buy, but buy ASAP, not be too picky, and IMO buying is a no brainer. This from 2018 was typical:

“ Imagine someone in SF in 2013 worried about cash flow on a Victorian. They would have missed out on gigantic returns, 500% range on their down payment.”

Lots of assets seem expensive these days. But when safe yields are 1% in dollars and negative in euros/yen, there’s no reason a growth stock should not be P/E of 70 or a house in a good area shouldn’t have a cap rate of 2.5%.

I’m not gonna be the last one to turn out the lights and give up on value investing. I purchased 25k of FIZZ today, my first reddit meme stock, and it went up 5k in a day. I have long owned irbt, and it became a reddit meme stock because it was heavily shorted, and suddenly rose 50%.

Everything else is bubbling,

Everything else is bubbling, so why not 25% increase for 2021?

He’s why it might:

Rates still ultra low.

Bullish investors and holders have been nothing but rewarded for 10 years. The pain of the bust is a distant memory.

Inventory even lower than our last two lift-offs in 2004-2006 and 1/2012 to 9/2014.

Those last two rockets lasted 2.5-3 years. We are not even at 10 months right now.

The only restraints are semi-tight lending standards and high nominal down-payments. Lending was even tighter in 2012-2014 though, and down payments can be 3.5 and 5% and covered with stock and other frothy market gains.

The raw inventory chart is

The raw inventory chart is remarkable. The prior vertical leap in 1/2012 started at inventory of 14k and ended (or transitioned to slower gains) at 8k.

This time we started at 6k and now at 2.5k less than a year later.

The 2012-2014 spike saw prices rise about 70% in less than three years. This time we have

higher incomes

lower rates

larger population

looser lending.

Evol: zillow shows 53 detached homes in SD City (excluding San Ysidro) with 3+/2+ beds and baths and under $850k.

Best to get into a rising market and renovate/trade up later IMO.

gzz wrote:

The 2012-2014

[quote=gzz]

The 2012-2014 spike saw prices rise about 70% in less than three years. This time we have

higher incomes

lower rates

larger population

looser lending.

[/quote]

You forgot: much, much higher valuations. (Far in excess of the increase in incomes).

gzz

I think it was the right

gzz

I think it was the right call and credit where credit is due. But its not entirely for the reasons you mentioned nor were the conditions that have caused this recent big run up present or predictable. This big recent gains are due to extreme imbalance of supply and demand. Listings are way down due to the pandemic and demand is way up not only locally but we are seeing an influx from denser higher priced areas.

As for there being nothing to buy, yes its tight but the better agents are the ones that are getting their clients in the better properties at fair prices lately. Experience matters. I see that over and over in my business and among peers

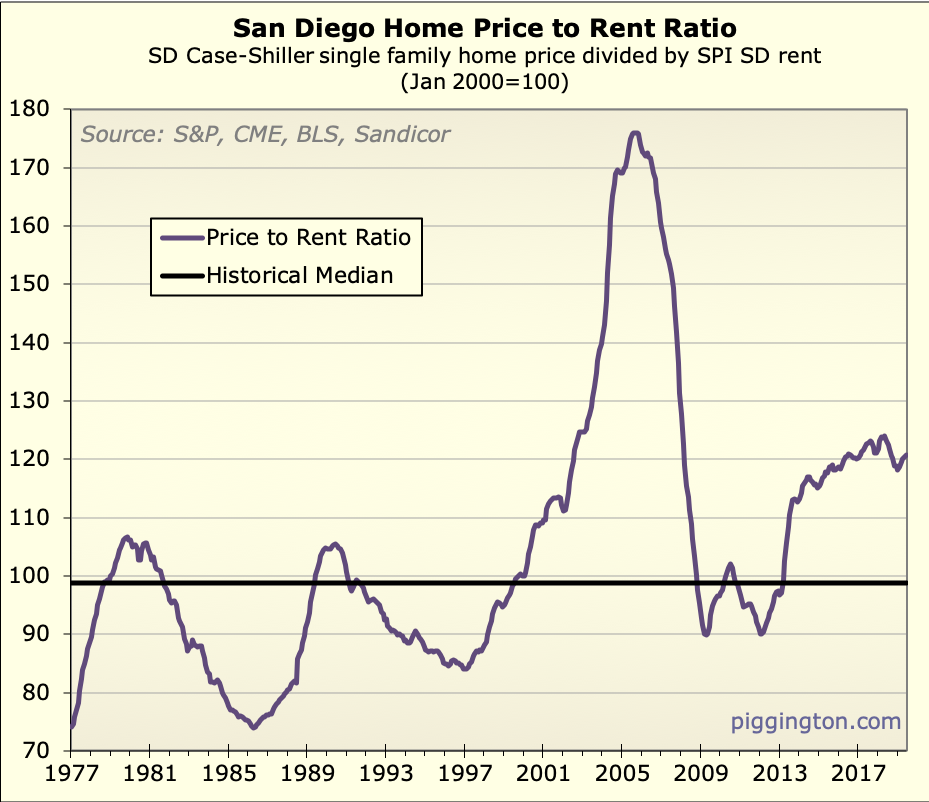

How much has discretionary

How much has discretionary income increased since 2006?

How much of this depends on low rates?

I wish we had graphs for those questions.

If Case Shiller is inflation-adjusted then is this now a 2006-sized bubble?

bewildering wrote:How much

[quote=bewildering]How much has discretionary income increased since 2006?

How much of this depends on low rates?

I wish we had graphs for those questions.

If Case Shiller is inflation-adjusted then is this now a 2006-sized bubble?[/quote]

We do have these graphs! I just need to update them. It’s getting high on the list.

Worrying about valuations is

Worrying about valuations is how I lost big shorting stocks!

Seriously though, as long as housing is subject to more favorable tax treatment and likely rent growth, its yield should generally be lower than federal bonds, but we’re way above this.

Even if we go up 50%, we’ll still be way below that.

Let’s take a typical 700k San Diego condo. Tax will be about 7.7k, HOA about 5k a year, $300 fire insurance, 13k total. If it rents for 2800/mo, that’s a net of about 20.6k.

The 30 year right now yields 1.8%. Applying that to the condo’s yield suggests a price of $1.14 million.

You can quibble with the assumptions here a little, but ultimately the condo’s yield can be protected from taxes fairly easily, and is likely to increase at or above inflation since housing in a nice city like San Diego is a luxury good whose demand increases faster than economic growth, while supply more slowly.

gzz wrote:Worrying about

[quote=gzz]Worrying about valuations is how I lost big shorting stocks!

Seriously though, as long as housing is subject to more favorable tax treatment and likely rent growth, its yield should generally be lower than federal bonds, but we’re way above this.

Even if we go up 50%, we’ll still be way below that.

Let’s take a typical 700k San Diego condo. Tax will be about 7.7k, HOA about 5k a year, $300 fire insurance, 13k total. If it rents for 2800/mo, that’s a net of about 20.6k.

The 30 year right now yields 1.8%. Applying that to the condo’s yield suggests a price of $1.14 million.

You can quibble with the assumptions here a little, but ultimately the condo’s yield can be protected from taxes fairly easily, and is likely to increase at or above inflation since housing in a nice city like San Diego is a luxury good whose demand increases faster than economic growth, while supply more slowly.[/quote]

I can quibble with one of the assumptions a lot, which is that 30 year UST yields will stay at 1.8% indefinitely. (You didn’t state that assumption outright, but it’s implicit in your comparing condo rental yields with the 30 year UST yield).

If yields go back to their normal relationship with inflation, the argument collapses. Will that happen? I don’t know (I don’t think anyone knows) but I think it’s a pretty big gamble to depend on rates staying abnormally low forever.

PS I appreciate your comment

PS I appreciate your comment on worrying about valuations, and I feel your pain… but bubbles past showed that people who worried about valuations were eventually glad they did. It just took a while (and felt like forever 🙂

Rich, I just don’t see any

Rich, I just don’t see any reason to either assume or predict rates will revert higher.

We don’t think life expectancy will revert to historic levels do we?

Nor per capita real GDP?

Nor the relative share of national income spent on clothing versus health care?

Why are nominal and real interest rates in the category “subject to mean reversion to 20th century levels”?

For me, the rates in peer nations with similar but more advanced population aging are a better guide about the future of US rates, and they point to lower US rates.

gzz wrote:Rich, I just don’t

[quote=gzz]Rich, I just don’t see any reason to either assume or predict rates will revert higher.

We don’t think life expectancy will revert to historic levels do we?

Nor per capita real GDP?

Nor the relative share of national income spent on clothing versus health care?

Why are nominal and real interest rates in the category “subject to mean reversion to 20th century levels”?

For me, the rates in peer nations with similar but more advanced population aging are a better guide about the future of US rates, and they point to lower US rates.[/quote]

I’m not “assuming or predicting” that rates will revert higher. I’m simply allowing for the possibility that they will.

Rich Toscano wrote:

I’m not

[quote=Rich Toscano]

I’m not “assuming or predicting” that rates will revert higher. I’m simply allowing for the possibility that they will.[/quote]

No, I will amend this.

I actually kind of think they could go up. They went down because of the pandemic. Why wouldn’t they go back up when the pandemic is over? That seems like the more likely outcome, if I’m forced to guess. But I’ll admit it could be wrong.

But that wasn’t really my main point. My main point was: nobody knows what rates will do, they could do anything and one of those things could be to go up, but your thesis assumes they will never go up.

On balance, 2 of 3 large

On balance, 2 of 3 large areas Japan and Europe have negative rates and there is very little expectation they will go positive anytime soon.

The Biden admin probably can’t print/borrow as much as they like with a 50/50 Senate.

Think normally market rate interest should be higher if US seen in isolation.

But with the complex interconnected economies, sideways is also an option for next year years.

Escoguy wrote:On balance, 2

[quote=Escoguy]On balance, 2 of 3 large areas Japan and Europe have negative rates and there is very little expectation they will go positive anytime soon.[/quote]

Our demographic aging and fertility decline is about 10 years behind Europe and Japan. Due to demographic momentum, even the unlikely chance of a sudden baby boom takes a very long time to have any substantial effect.

There’s a very good chance in my opinion of US 10 year rates falling below 0% too in 5-10 years.

Rich, you wrote

“[Rates] went

Rich, you wrote

“[Rates] went down because of the pandemic. Why wouldn’t they go back up when the pandemic is over?”

Most of the rate decrease was before the pandemic. 30 year mortgage rates had their local peak in Oct 2018 at 4.8%. In Jan 2020, they were 3.5%, now are 2.7%.

A return to a pre-pandemic trendline would mean rates of about 3.1%. I don’t see that denting this market.

“But that wasn’t really my main point. My main point was: nobody knows what rates will do”

No we don’t, but our neutral assumption is the huge and liquid market for US residential mortgages reflects all current information and expectations, and is equally likely to go up as down.

“but your thesis assumes they will never go up.”

Again, I think the neutral assumption is mortgage rates of 1.7% are as likely as a return to 3.7%.

That said, the effect on the market isn’t equal of an increase versus decrease in rates. Everyone is locking in at sub-3% fixed these days, which will tend to decrease supply since the cost of owning goes down and the profit from renting goes up. A mild rate increase wouldn’t be bullish, but it would restrict supply since a 2.7% mortgage is quite valuable when rates are at 4%.

This offset to the negative effect of rising rates is not mirrored by a similar negative offset to the positive of falling rates.

Instead, a further decrease in rates is bullish in a huge number of ways: it decreases mortgage costs, allows another wave of refis, and decreases the return of alternative investments to RE. It further reduces supply by making it easier to avoid foreclosure for distressed owners.

To a large extent, I think these bullish factors are not yet fully priced in yet. Prices are sticky upward because of both psychological factors and also the need for mortgage appraisals to meet comps.

I experienced this myself when I did a refi back in 2013, when the appraisal came in way below actual value and only 5% higher than 2011 purchase price, despite impressive renovations and market that had gone up well over 20% since my purchase.

People in the industry might have other other examples, but outside of the ultra-loose lending of the 2004-2006 bubble period, I think banks are reluctant to extend mortgages that are based on valuations 20% or more higher than 12 months prior, even when the market goes up that much. If true, this theory would predict extremely low inventory, which is exactly what we see. Sellers don’t want to sell below economic value, but won’t list at the market clearing price because they know they may have to deal with the costs and frustration of a strong good faith buyer not getting financing.

I also have a feeling we are mid-way into another bubble-fueling virtuous cycle where rising prices reduce loan losses in every segment of the mortgage market, which leads to looser standards and lower spreads over treasuries, which leads to higher prices.

Just to add to the

Just to add to the conversation on valuation. This 3/2.5 home in Carmel Valley has been trying to rent out at $3700 for over 5 months with no luck.

https://www.zillow.com/homedetails/11317-Carmel-Creek-Rd-San-Diego-CA-92130/16777926_zpid/

Nearby similar homes have been selling recently for well over $1M. That’s over 300 rental months! Or this house that is asking almost 400 rental months: https://www.redfin.com/CA/San-Diego/3917-Via-Cangrejo-92130/home/4518999.

What was the price-to-rent ratio at the peak of the last bubble just before it burst?

I’m not totally against buying right now. We’re actually in escrow for a Del Mar condo right now with a price of 197 rental months, so there are still deals to be had. But I see the SFR’s in DMCV as totally over-valued. I saw arguments above of:

higher incomes

larger population

lower rates

looser lending

Higher incomes and larger population should affect rental price equally. In fact, there’s an extra perk for renting in DMCV this year since Del Mar Union is one of the only districts in the county that has full-time in-person elementary school – a perk that should temporarily boost rental value (but not as too much on buying).

Lower rates and looser lending are transient conditions that can’t be maintained forever — if the economy rebounds rates will go up; if there’s post-pandemic recession looser lending might disappear too. I feel like it’s only a matter of time before prices come down to earth (tethered to rental prices). Plus, don’t they say markets tend to crash when everyone buys into the euphoria?

There’s definitely a lot of pent-up demand, but lately I feel like there’s suddenly a flurry of listing activities too (ETA: in the time it took me to write this entire post, two homes came on the market in CV). I don’t know if I’m imagining it or if supply is truly rising as higher valuation as well as the improving covid situation are finally enticing owners to sell. The other thing I remember about the last bubble was that the cheaper homes were rising much faster than more expensive homes, as the buying frenzy drove up the purchasing of any home that people could possibly stretch to buy (instead of a home people actually needed or wanted), as panic/fear-of-losing-out drove purchase decisions. I feel like that’s what’s happening now. I live in LJ Shores where one neighbor just delisted a house that they failed to sell after 6 months; Del Mar looks very expensive but it always has been; cheaper surrounding areas like University City, CV, Sorrento Valley, Solana Beach, Encinitas have risen far more in price – costing almost as much as Del Mar.

I’d love to see a monitor of the number of units listed/pending/sold in DMCV going forward.

I would also love to see what Rich’s valuation index looks like right now. Have we entered bubble territory yet?

P.S. So I went and did my poor man’s version of the valuation index (only based on price-to-rent) by looking at the change in SD rent b/t 1997 and now (according to Zillow, so going from 2.6K to 2.84K), and the change in SFR price (going from 570K to 674K) in the same time frame. And I came up with the result that if the valuation index in 2017 was at 120 according to Rich’s chart ), then it is now at 130, which is a lot higher than it ever was previously except during the run-up to the big bubble, but still is a ways under the peak of 175.

), then it is now at 130, which is a lot higher than it ever was previously except during the run-up to the big bubble, but still is a ways under the peak of 175.

So I guess it could still go up a long ways before falling. If it’s going to be like the last bubble, it could be another 2.5 years before it rounds the peak, and 5 years before prices are “good” for buyers again. But it also be a smaller bubble because lending standards are much higher now; or it could be an even bigger bubble because interest rates have never been so low and the Fed seems determined to keep them low.

feraina: what does the

feraina: what does the price/rent look like at CV 1-bedroom condos? I don’t think $1.8 million six-beds are especially relevant to determine market rent ratios.

The one you say was on the market for a long time specifies “6-9” month lease. That implies to me it isn’t long term, but the demand for a high end 3-bedroom for exactly that period might well be zero.

:I live in LJ Shores where one neighbor just delisted a

:house that they failed to sell after 6 months

LJS is older and very high end, with very different lots and views mixed close together. This makes it easier to overprice a house, and harder to tell since the market is inherently fragmented and illiquid compared to CV.

I follow my own zip of 92107 very closely, and my observation is its similar high-end/hard-to-value places in the $2m+ range now sell much faster than any other time. Even high end buyers have FOMO.

I’m not sure where you’re

I’m not sure where you’re going with this. But anyway there are no 1beds in CV. I mean there are apartments but not condos. I guess one could look at prices and rent for 2beds. I am guessing the latter is under $2200 (just because Del Mar across the highway is), but they’re selling for over $750K I’d guess. So even worse then the 3beds in rent-months.

feraina wrote:I’m not sure

[quote=feraina]I’m not sure where you’re going with this. But anyway there are no 1beds in CV. I mean there are apartments but not condos. I guess one could look at prices and rent for 2beds. I am guessing the latter is under $2200 (just because Del Mar across the highway is), but they’re selling for over $750K I’d guess. So even worse then the 3beds in rent-months.[/quote]

I would caution using CV as a measuring stick for SFR rental market. It is a very odd one and not like most others. The type of people that want to live in an SFR there seem to prefer buying and can afford to do so. The ones that just want to be there for the schools will rent the smallest thing they can get away with like a condo. Much of that is cultural norms.

I worked on renting out a nice 5BR/3BA in CV about a year ago and it was brutally tough. Itw as like banging my head on a wall. Most applicants were groups of students or professional singles not families with 2 to 3 kids as one would expect. Put that house in Encinitas/South Carlsbad and there is a line of applicants for the same or higher rent. Different folks with different values up here. CV SFR rental market is an abnormality in the market.

And there are a bunch of 1BR condos in CV

Oh I just got an alert in my

Oh I just got an alert in my Redfin feed that a 1 bedroom in CV listed at $538K is pending. Zillow says rental value is $2250. So a multiplication factor of 240. Sdrealtor, I can see your argument about really large homes but what about a 1 bedroom? Who buys 1 bedrooms? Maybe a professional or an investor. I can’t imagine why an investor would pay that high. $2250 doesn’t even include the $405 HOA fees.

feraina wrote:Oh I just got

[quote=feraina]Oh I just got an alert in my Redfin feed that a 1 bedroom in CV listed at $538K is pending. Zillow says rental value is $2250. So a multiplication factor of 240. Sdrealtor, I can see your argument about really large homes but what about a 1 bedroom? Who buys 1 bedrooms? Maybe a professional or an investor. I can’t imagine why an investor would pay that high. $2250 doesn’t even include the $405 HOA fees.[/quote]

Single adults, older folks that want to live alone, second/vacation homes, people that need to come here for work but have family living else where. Those are a few off the top of my head. There aren’t many 1 units comparatively. They rent for only a little less than 2 bedroom units also.

In CV they start around 400k and rent around 2200 so your multiplier is a bit off

feraina, Redfin price and

feraina, Redfin price and rent estimates are garbage.

My OB condo it underestimates the property price by more than 65%. As in, it says a 2/2 condo with parking and ocean view 2 blocks from the beach is worth 440k. Really.

The rental range is really wide, but the midpoint of it is substantially lower than it is rented for, and I set the rent 4+ years ago at a friendly level and have never raised it. It’s off by at least 20% on rent.

Valuation

Valuation update!!

https://www.piggington.com/hastening_away_affordability_san_diego_housing_valuations_jan_2

Rich Toscano wrote:Valuation

[quote=Rich Toscano]Valuation update!!

https://www.piggington.com/hastening_away_affordability_san_diego_housing_valuations_jan_2%5B/quote%5D

Thanks!

They are trying to lease for

They are trying to lease for 6/9 months.

Most long term renters want a year so not a good proxy for the market.

I’ve only done one short term in 20 years.