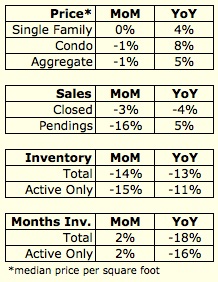

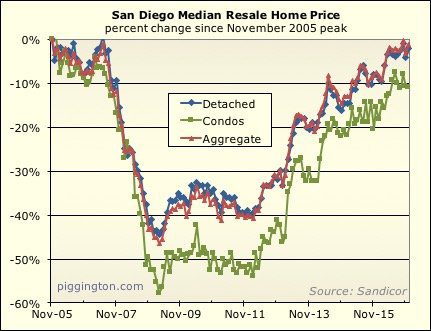

Here’s the final score for the year 2016:

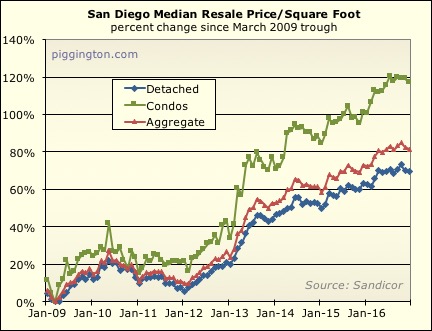

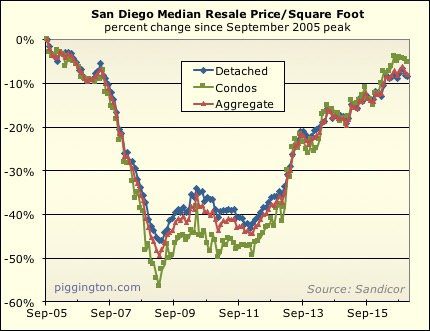

Looking at the single family number, which gives the best read, prices

increased a couple % more than inflation, and roughly the same as wage

and rent growth. As one would expect in a given year, all things

being equal.

This time they’re not equal in that valuations began the year at an elevated

level. However, as discussed in the afore-linked article,

perhaps valuations can remain higher than usual while interest rates

remain lower than usual.

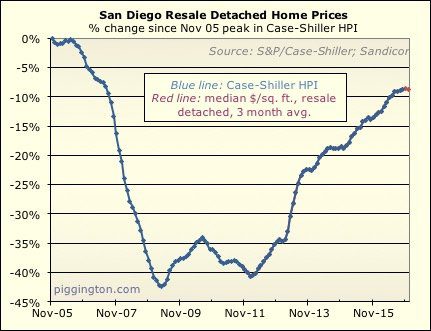

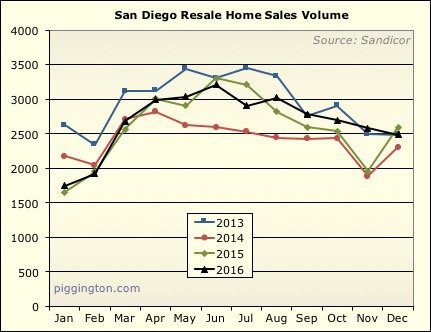

Back to the monthly data, prices did pull back, but that’s reasonable

at this time of year:

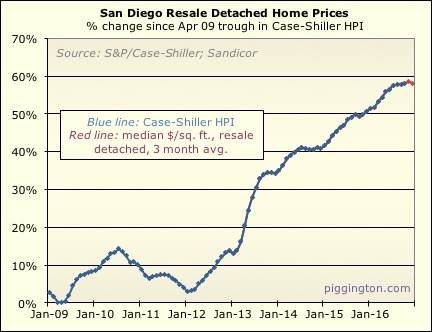

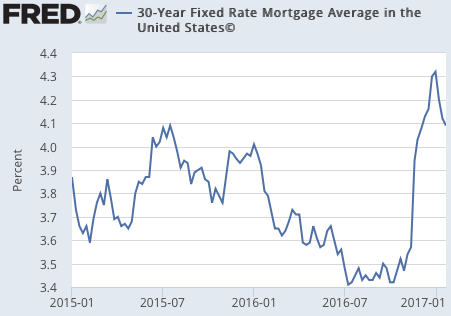

No evidence yet that the recent rate rise is taking a big bite, but

keep in mind that as abrupt

as the increase was, it didn’t take rates all that far above where they

began 2016:

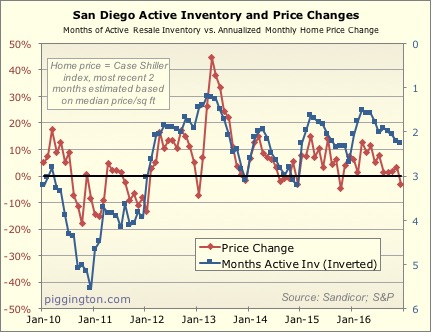

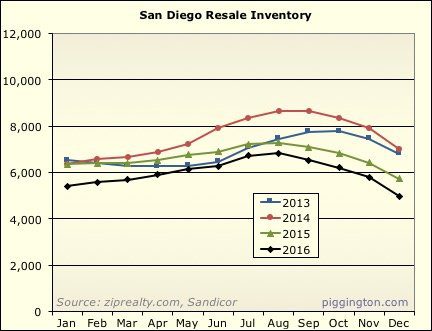

The inventory-vs-price chart shows that months of inventory remains

pretty tight, and at a level that would usually put upward pressure on

prices. The dip down in prices appears typical for year-end… I

would expect some convergence in these two lines as time goes on

(either prices starting back up again, or months of inventory

increasing as demand wanes compared to supply).

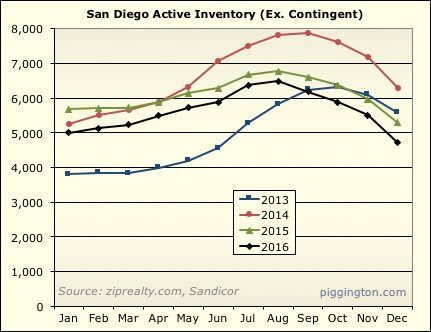

Here’s a closer look at months of inventory. The typical December

bounce was a no-show; let’s see what happens as the year begins.

Some more graphs are below, for those who want to get into the weeds…

Figure 4 vs the last figure

Figure 4 vs the last figure both shows inventory vs price change. In figure 4, 3 month inventory and 0% price change is aligned while in the last figure 0% and 6 month inventory is aligned. I keep hearing realtors quoting 6 months being a healthy inventory. Seems like figure 4 has been alignment of price and inventory. I wonder if in the new world of low inventory, 3 month supply means a balanced market with no higher appreciation than inflation?

Also, Rich do you think the housing price on the middle and upper middle range would drop 6% if/when standard deduction is raised to ~30K? It will negate any mortgage interest deduction for the typical buyers of median house in SD? 400K mortgage @ 4%, implies a 16K interest. So all owners up to ~800K in loan would not be able to take advantage of mortgage interest deduction?

Thank you for the update.

Thank you for the update.

The very tight inventory/price correlation has certainly broken down the last three years.

I would say that it is because of tight lending. You really need a down payment this cycle, so the rental pool needs to save up $60,000 to get a starter home. Once they do, the payments together with MI deduction will probably be lower than their rent, but that does not matter if they don’t have the $60,000.

The stock market increase should help those saving for a down payment.

January and early February in

January and early February in my area looks strong for prices. High end places are moving at a good rate and inventory remains extremely low