San Diego homeowners with adjustable rate mortgages can breathe a sigh of relief. After 17 consecutive — albeit modest — rate increases, the Federal Reserve has decided to stand pat and keep its federal funds target rate at 5.25 percent.

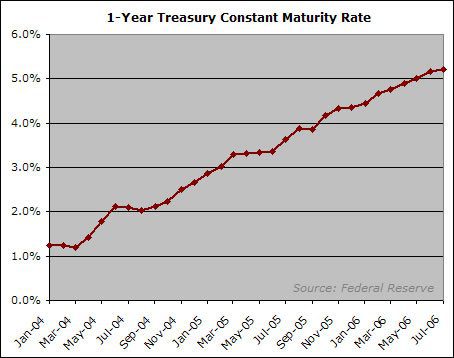

The accompanying chart shows the seemingly unstoppable rise in the 1-Year Constant Maturity Treasury, an index often used to adjust monthly mortgage payments, during the Fed’s tightening campaign.

Another great graph from

Another great graph from Rich.

Borrowers who took out an adjustable loan (option-ARM, ARM, I/O) in the summer of 2004, at 2%, are going to see their payments more than double this summer.

I don’t know about you, but I know I wouldn’t be able to handle a doubling of my mortgage payment. Neither will the folks who bought in the summer of ’04. Thus, in 3 months we should see a fresh batch of NODs.

The Fed’s interest rate increases are still in the pipeline. Most of the exotic loans have not yet come up for renewal, so the effect of rising interest rates is still looming. Even if the Fed leaves rates as they are, or drops them at the next meeting as they realize a recession is imminent, that will not save ARM holders, who truly need a reversal to 2002 rates.

Higher interest rates drive many to bankruptcy, because they won’t qualify for refinancing at today’s higher rates and with lower home equity. People were buying homes at more than the traditional 3 – 3.5 x annual gross income, using loans with temporary low interest rates, which were bound to go up! An adjustable rate loan is not a good idea when interest rates at the lowest in history. An adjustable rate loan could make sense when rates are high, and you are betting on rates going down. So the first problem is that a borrower who qualified for a mortgage at 2%, won’t qualify for that same mortgage at 6%. The other issue is their LTV will be too high to qualify for a refinance; the bank won’t lend more than the house is worth. If they have not paid off any principal, and the housing prices are falling, some borrowers will be underwater now. Not a good time to refinance. The only way out: get a 2nd job to pay for that ever-rising mortgage, sell, or give the home back to the bank.

Why should the bank care? Mostly the borrower is holding the interest rate risk, and investors who are not savvy enough to understand the risk they were taking on, bought these loans up by the trillions of dollars. MBS (mortgage backed securities) and CMO (collateralized mortgage obligations) were earning a better rate of return than CDs for many years. Global money flowed into these products, from central banks, pension funds, perhaps even retirement accounts and money market funds.

I am betting that most adjustable rate borrowers will delay on selling, and will be stuck with short sales and bankruptcy/foreclosure.

A high level of foreclosures is in the pipeline, unless the Federal Reserve lowers interest rates back to 2%, AND international investors keep buying mortgage backed securities.

Yet the most worrisome aspect of this is not the individuals who foolishly chose these risky loans, but the financial impact on corporations, governments, money markets, Fannie Mae and the other GSEs, pension funds, and foreign central banks, who bought all this paper. After all, the real risk of these loans is held by the lender, and the lender is NOT your local bank. It is all the people I just listed, and it probably is you too (via your pension fund, etc.).

For this reason, I think cash is safest. Do we know for sure that our money market fund or our GSEs do not hold, or is affiliated with, any of MBS or CMO money?

Schahrzad Berkland

It may be used to adjust

It may be used to adjust short term rates, but if you compare it to the 30 year mortgage rate for the last 3 years, there seems to be no correlation. The fed has raise rates and the 30 year mortgage has not increased in the same manner. Rates should be closer to 7 1/2 if there was a direct correlation between the fed funds rate and the 30 year.

Here is a link to a different view of the whole mess.

link